You might also like

- Foreign Exchange MarketDocument24 pagesForeign Exchange MarketGaurav DhallNo ratings yet

- Global Grants Community Assessment FormDocument3 pagesGlobal Grants Community Assessment Formlalitya xavieraNo ratings yet

- Foreign Exchange MarketDocument40 pagesForeign Exchange MarketSayaliRewaleNo ratings yet

- How To Guide To Oauth and API SecurityDocument12 pagesHow To Guide To Oauth and API Securitysilviuleahu100% (1)

- Wi-Fi Planning and Design Questionnaire 2.0Document12 pagesWi-Fi Planning and Design Questionnaire 2.0Free Space67% (3)

- A Study of Foreign Exchange and Risk ManagementDocument7 pagesA Study of Foreign Exchange and Risk ManagementMallikarjun Rao100% (2)

- Management of Forex TransactionsDocument64 pagesManagement of Forex TransactionsasifanisNo ratings yet

- Point of View Task CardsDocument7 pagesPoint of View Task Cardsapi-660227300No ratings yet

- Project Report On Currency MarketDocument54 pagesProject Report On Currency MarketSurbhi Aery63% (8)

- Apply 3S: Information Sheet Level 1Document137 pagesApply 3S: Information Sheet Level 1Atsede MitikuNo ratings yet

- FOREIGN EXCHANGE MARKET - Final ReportDocument33 pagesFOREIGN EXCHANGE MARKET - Final ReportDisha MathurNo ratings yet

- A PROJECT REPORT On Study On Foreign Exchange Final1Document35 pagesA PROJECT REPORT On Study On Foreign Exchange Final1Genesian Nikhilesh PillayNo ratings yet

- 1.1 Cruz v. DENR PDFDocument7 pages1.1 Cruz v. DENR PDFBenBulacNo ratings yet

- Blockchain Unit Wise Question BankDocument3 pagesBlockchain Unit Wise Question BankMeghana50% (4)

- Importance of Team Work in An OrganizationDocument10 pagesImportance of Team Work in An OrganizationMohammad Sana Ur RabNo ratings yet

- Chapter One and TwoDocument50 pagesChapter One and Twomikialeabrha23No ratings yet

- Currency Markets and Exchange RatesDocument18 pagesCurrency Markets and Exchange RateslosangelesNo ratings yet

- International Financial ManagementDocument88 pagesInternational Financial Managementnagesh komatiNo ratings yet

- Module 3 Lesson 3Document15 pagesModule 3 Lesson 3Marivic TolinNo ratings yet

- Leela Mam Ques & AnsDocument30 pagesLeela Mam Ques & AnsBhuvana HariNo ratings yet

- Foreign Exchange MarketsDocument17 pagesForeign Exchange MarketsDiana BercuNo ratings yet

- InvestmentDocument30 pagesInvestmentJimitMehtaNo ratings yet

- A Report On Foreign Exchange Risk Management: by Kavita P. ChokshiDocument34 pagesA Report On Foreign Exchange Risk Management: by Kavita P. Chokshikpc87No ratings yet

- Trichy Full PaperDocument13 pagesTrichy Full PaperSwetha Sree RajagopalNo ratings yet

- Foreign Exchange Is Essential To Coordinate Global BusinessDocument7 pagesForeign Exchange Is Essential To Coordinate Global BusinesssaranistudyNo ratings yet

- The Foreign Exchange Market: Unit 5 SectionDocument6 pagesThe Foreign Exchange Market: Unit 5 SectionBabamu Kalmoni JaatoNo ratings yet

- Javed Project AnuDocument5 pagesJaved Project Anu25javedshaikhNo ratings yet

- Foreign Exchange MarketDocument10 pagesForeign Exchange MarketMzee Mayse CodiersNo ratings yet

- Chapter II. The Foreign Exchange MarketDocument19 pagesChapter II. The Foreign Exchange MarketThùy ThùyNo ratings yet

- International Financial Management PPT Chap 1Document28 pagesInternational Financial Management PPT Chap 1serge folegweNo ratings yet

- Foreign Exchange On EconomyDocument7 pagesForeign Exchange On Economyeslam hamdyNo ratings yet

- The Foreign Exchange MarketDocument3 pagesThe Foreign Exchange MarketDavina AzaliaNo ratings yet

- Introduction To Foreign ExchangeDocument36 pagesIntroduction To Foreign Exchangedhruv_jagtap100% (1)

- ln1 PDFDocument20 pagesln1 PDFM.n KNo ratings yet

- Key Currencies:: Share of National Currencies in Total Identified Official Holdings of Foreign Exchange, 1998Document12 pagesKey Currencies:: Share of National Currencies in Total Identified Official Holdings of Foreign Exchange, 1998KaranPatilNo ratings yet

- Unit 6 Foreign Exchange Markets For StudentsDocument9 pagesUnit 6 Foreign Exchange Markets For StudentsĐào Phan Le AnhNo ratings yet

- Introduction To Foreign ExchangeDocument27 pagesIntroduction To Foreign Exchangemandy_t06No ratings yet

- Ass1 InternationalDocument21 pagesAss1 InternationalAbdulhafiz HajkedirNo ratings yet

- Sikkim Manipal University Sikkim Manipal University 4 Semester Spring 2011Document11 pagesSikkim Manipal University Sikkim Manipal University 4 Semester Spring 2011Alaji Bah CireNo ratings yet

- Susmel Foreign Exchange MarketsDocument18 pagesSusmel Foreign Exchange MarketsRAPID M&ENo ratings yet

- Inter - CH - 1 (1) (Read-Only)Document23 pagesInter - CH - 1 (1) (Read-Only)sharifhass36No ratings yet

- Foreign Exchange MarketDocument3 pagesForeign Exchange MarketJayesh BhandarkarNo ratings yet

- The Foreign Exchange Market: QuestionsDocument3 pagesThe Foreign Exchange Market: QuestionsCarl AzizNo ratings yet

- Chap05 Ques MBF14eDocument6 pagesChap05 Ques MBF14eÂn TrầnNo ratings yet

- MODULE 8 ReportingDocument7 pagesMODULE 8 Reportingjerome magundinNo ratings yet

- Week 2 Tutorial QuestionsDocument4 pagesWeek 2 Tutorial QuestionsWOP INVESTNo ratings yet

- International FinanceDocument56 pagesInternational FinanceSucheta Das100% (1)

- Functions of Foreign Exchange MarketsDocument6 pagesFunctions of Foreign Exchange Marketstechybyte100% (1)

- Foreign Exchange MarketDocument9 pagesForeign Exchange MarketHemanth.N S HemanthNo ratings yet

- Lesson 05Document12 pagesLesson 05mavericksailorNo ratings yet

- Central Bank Foreign Exchange Markets Exchange RateDocument3 pagesCentral Bank Foreign Exchange Markets Exchange Rategayathri murugesanNo ratings yet

- College of Business and Economics: Econ. 2082: International Economics II, AssignmentDocument11 pagesCollege of Business and Economics: Econ. 2082: International Economics II, AssignmentAbdulhafiz HajkedirNo ratings yet

- Foreign Exchange MarketsDocument19 pagesForeign Exchange MarketsniggerNo ratings yet

- Chapter 2-tcqtDocument39 pagesChapter 2-tcqtanhphuongphamleNo ratings yet

- Meaning of Foreign Exchange MarketDocument3 pagesMeaning of Foreign Exchange Marketleggy1587No ratings yet

- 1 Meaning and Function of Foreign Exchange Market 2 Types of Foreign Exchange MarketsDocument14 pages1 Meaning and Function of Foreign Exchange Market 2 Types of Foreign Exchange MarketsAnonymous GueU02hBdNo ratings yet

- REFLECTION-PAPER-BA233N-forex MarketDocument6 pagesREFLECTION-PAPER-BA233N-forex MarketJoya Labao Macario-BalquinNo ratings yet

- Foreign Exchange Market: CurrenciesDocument2 pagesForeign Exchange Market: CurrenciesErica CalzadaNo ratings yet

- Print EcoDocument1 pagePrint EcoishanhbmehtaNo ratings yet

- Comprehensive Notes On International Financial MarketDocument16 pagesComprehensive Notes On International Financial Marketকাজী এস এম হানিফ0% (1)

- Marco Economics Sem - 2 FC - 1Document28 pagesMarco Economics Sem - 2 FC - 1Sharath KanzalNo ratings yet

- Ibt Module 4Document2 pagesIbt Module 4jntvtn7pc9No ratings yet

- Sources of International FinanceDocument15 pagesSources of International FinanceEmerose BaliaNo ratings yet

- Chap 2Document26 pagesChap 2jasneet kNo ratings yet

- Forign Currency TransactionDocument31 pagesForign Currency Transactionnik22ydNo ratings yet

- Foreign Exchange MarketDocument3 pagesForeign Exchange MarketVasim ShaikhNo ratings yet

- Supply & DemandDocument15 pagesSupply & Demandakhiljith100% (1)

- CH-3 PlanningDocument54 pagesCH-3 Planningyirgalemle ayeNo ratings yet

- CH-3 PlanningDocument54 pagesCH-3 Planningyirgalemle ayeNo ratings yet

- 5S Job CycleDocument1 page5S Job Cycleyirgalemle ayeNo ratings yet

- Doctoral Thesis: Human Resource Management and Organizational PerformanceDocument229 pagesDoctoral Thesis: Human Resource Management and Organizational Performanceyirgalemle ayeNo ratings yet

- CH-5 OrganizingDocument48 pagesCH-5 Organizingyirgalemle ayeNo ratings yet

- CH-1 Overview of MGMTDocument33 pagesCH-1 Overview of MGMTyirgalemle ayeNo ratings yet

- CH-8 Intro - To MGTDocument15 pagesCH-8 Intro - To MGTyirgalemle ayeNo ratings yet

- Chapter - 2 - Development of Management ThoughtDocument35 pagesChapter - 2 - Development of Management Thoughtyirgalemle ayeNo ratings yet

- Introduction To Management PPT at Bec Doms Bagalkot MbaDocument34 pagesIntroduction To Management PPT at Bec Doms Bagalkot MbaBabasab Patil (Karrisatte)No ratings yet

- Chapter 4 DMDocument14 pagesChapter 4 DMyirgalemle ayeNo ratings yet

- UC Morality and Professional EthicsDocument4 pagesUC Morality and Professional EthicsKiya AbdiNo ratings yet

- II Course OutlineDocument3 pagesII Course Outlineyirgalemle ayeNo ratings yet

- Unit ThreeDocument38 pagesUnit Threeyirgalemle ayeNo ratings yet

- TM-Entrepreneurship and Employabilityskill - TwoDocument227 pagesTM-Entrepreneurship and Employabilityskill - TwoKiya Abdi100% (2)

- Level I IT Support ServiceDocument53 pagesLevel I IT Support Serviceyirgalemle ayeNo ratings yet

- TM Morality and Professional EthicsDocument126 pagesTM Morality and Professional EthicsKiya Abdi100% (2)

- Women Workers Prohaboted Activite DirectivesDocument12 pagesWomen Workers Prohaboted Activite Directivesyirgalemle ayeNo ratings yet

- Curriculum Morality and Professional EthicsDocument11 pagesCurriculum Morality and Professional EthicsKiya Abdi100% (2)

- D-II Chap-1Document45 pagesD-II Chap-1yirgalemle ayeNo ratings yet

- 568 - 2000 Right To Employment of Persons With DisabilityDocument7 pages568 - 2000 Right To Employment of Persons With Disabilitymelewon2No ratings yet

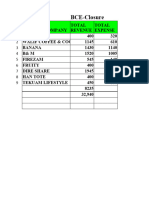

- Bce Closure SuDocument6 pagesBce Closure Suyirgalemle ayeNo ratings yet

- Human Communication Processes Session 5Document12 pagesHuman Communication Processes Session 5yirgalemle ayeNo ratings yet

- Philips Chassis Lc4.31e Aa Power Dps 181 PDFDocument9 pagesPhilips Chassis Lc4.31e Aa Power Dps 181 PDFAouadi AbdellazizNo ratings yet

- Spectrochem Chemindex 2016 17Document122 pagesSpectrochem Chemindex 2016 17Nivedita Dube0% (1)

- Lucero Flores Resume 2Document2 pagesLucero Flores Resume 2api-260292914No ratings yet

- Variable Length Subnet MasksDocument4 pagesVariable Length Subnet MaskszelalemNo ratings yet

- Lab ManualDocument15 pagesLab ManualsamyukthabaswaNo ratings yet

- Retail Marketing Course Work 11Document5 pagesRetail Marketing Course Work 11Ceacer Julio SsekatawaNo ratings yet

- Cat It62hDocument4 pagesCat It62hMarceloNo ratings yet

- Lae ReservingDocument5 pagesLae ReservingEsra Gunes YildizNo ratings yet

- HK Magazine 03082013Document56 pagesHK Magazine 03082013apparition9No ratings yet

- Valery 1178Document22 pagesValery 1178valerybikobo588No ratings yet

- Methods of ResearchDocument12 pagesMethods of ResearchArt Angel GingoNo ratings yet

- 9a Grundfos 50Hz Catalogue-1322Document48 pages9a Grundfos 50Hz Catalogue-1322ZainalNo ratings yet

- 3a. Systems Approach To PoliticsDocument12 pages3a. Systems Approach To PoliticsOnindya MitraNo ratings yet

- Sec 11Document3 pagesSec 11Vivek JhaNo ratings yet

- IM0973567 Orlaco EMOS Photonview Configuration EN A01 MailDocument14 pagesIM0973567 Orlaco EMOS Photonview Configuration EN A01 Maildumass27No ratings yet

- 2008 Reverse Logistics Strategies For End-Of-life ProductsDocument22 pages2008 Reverse Logistics Strategies For End-Of-life ProductsValen Ramirez HNo ratings yet

- Oxford Handbooks Online: From Old To New Developmentalism in Latin AmericaDocument27 pagesOxford Handbooks Online: From Old To New Developmentalism in Latin AmericadiegoNo ratings yet

- 036 ColumnComparisonGuideDocument16 pages036 ColumnComparisonGuidefarkad rawiNo ratings yet

- Introduction and Instructions: ForewordDocument20 pagesIntroduction and Instructions: ForewordDanang WidoyokoNo ratings yet

- Allergies To Cross-Reactive Plant Proteins: Takeshi YagamiDocument11 pagesAllergies To Cross-Reactive Plant Proteins: Takeshi YagamisoylahijadeunvampiroNo ratings yet

- Data Loss PreventionDocument20 pagesData Loss Preventiondeepak4315No ratings yet

- Job Description: Extensive ReadingDocument12 pagesJob Description: Extensive ReadingNatalia VivonaNo ratings yet

- Digirig Mobile 1 - 9 SchematicDocument1 pageDigirig Mobile 1 - 9 SchematicKiki SolihinNo ratings yet