Professional Documents

Culture Documents

Kaplan - Porter - 2011 9 - How To Solve The Cost Crisis in Health Care - HBR

Uploaded by

bayu prabuOriginal Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Kaplan - Porter - 2011 9 - How To Solve The Cost Crisis in Health Care - HBR

Uploaded by

bayu prabuCopyright:

Available Formats

HBR.

ORG

Robert S. Kaplan is a Baker Michael E. Porter is the

Foundation Professor at Bishop William Lawrence

Harvard Business School. University Professor at

Harvard. He is based at

Harvard Business School.

How to Solve

The Cost Crisis

In Health Care

The biggest problem with health care isn’t

with insurance or politics. It’s that we’re

measuring the wrong things the wrong way.

by Robert S. Kaplan and Michael E. Porter

PHOTOGRAPHY: MARK HOOPER

September 2011 Harvard Business Review 47

1271 Sep11 Kaplan layout.indd 47 7/27/11 6:08:04 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE

U.S. health care costs

currently exceed 17% of

GDP and continue to rise.

Other countries spend less of their GDP on health care they are unable to link cost to process improvements

but have the same increasing trend. Explanations are or outcomes, preventing them from making sys-

not hard to find. The aging of populations and the de- temic and sustainable cost reductions. Instead, pro-

velopment of new treatments are behind some of the viders (and payors) turn to simplistic actions such

increase. Perverse incentives also contribute: Third- as across-the-board cuts in expensive services, staff

party payors (insurance companies and governments) compensation, and head count. But imposing arbi-

reimburse for procedures performed rather than out- trary spending limits on discrete components of care,

comes achieved, and patients bear little responsibility or on specific line-item expense categories, achieves

for the cost of the health care services they demand. only marginal savings that often lead to higher total

But few acknowledge a more fundamental source systems costs and poorer outcomes. For example, as

of escalating costs: the system by which those costs payors introduce high copayments to limit the use of

are measured. To put it bluntly, there is an almost expensive drugs, costs may balloon elsewhere in the

complete lack of understanding of how much it costs system should patients’ overall health deteriorate

to deliver patient care, much less how those costs and they subsequently require more services.

compare with the outcomes achieved. Instead of Poor cost measurement has also led to huge

focusing on the costs of treating individual patients cross-subsidies across services. Providers are gener-

with specific medical conditions over their full cycle ously reimbursed for some services and incur losses

of care, providers aggregate and analyze costs at the on others. These cross-subsidies introduce major

specialty or service department level. distortions in the supply and efficiency of care. The

Making matters worse, participants in the health inability to properly measure cost and compare cost

care system do not even agree on what they mean by with outcomes is at the root of the incentive problem

costs. When politicians and policy makers talk about in health care and has severely retarded the shift to

cost reduction and “bending the cost curve,” they are more effective reimbursement approaches.

typically referring to how much the government or Finally, poor measurement of cost and outcomes

insurers pay to providers—not to the costs incurred also means that effective and efficient providers go

by providers to deliver health care services. Cutting unrewarded, while inefficient ones have little incen-

payor reimbursement does reduce the bill paid by tive to improve. Indeed, institutions may be penalized

insurers and lowers providers’ revenues, but it does when the improvements they make in treatments

nothing to reduce the actual costs of delivering care. and processes reduce the need for highly reimbursed

Providers share in this confusion. They often allocate services. Without proper measurement, the healthy

their costs to procedures, departments, and services dynamic of competition—in which the highest-value

based not on the actual resources used to deliver care providers expand and prosper—breaks down. In-

but on how much they are reimbursed. But reim- stead we have zero-sum competition in which health

bursement itself is based on arbitrary and inaccurate care providers destroy value by focusing on highly

assumptions about the intensity of care. reimbursed services, shifting costs to other entities,

Poor costing systems have disastrous conse- or pursuing piecemeal and ineffective line-item cost

quences. It is a well-known management axiom that reductions. Current health care reform initiatives will

what is not measured cannot be managed or im- exacerbate the situation by increasing access to an in-

proved. Since providers misunderstand their costs, efficient system without addressing the fundamental

48 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 48 7/27/11 6:08:11 PM

HBR.ORG

Idea in Brief

Much of the rapid escalation Pilot projects under way at As providers and payors

in health care costs can be hospital systems in the U.S. better understand costs,

attributed to the fact that and Europe demonstrate the they will be positioned to

providers have an almost transformative effect of a achieve a true “bending of

complete lack of understand- new approach that accu- the cost curve” from within

ing of how much it costs to rately measures costs—at the system, not based on

deliver patient care. Thus the level of the individual top-down mandates.

they lack the knowledge nec- patient with a given medical The sheer size of the op-

essary to improve resource condition over a full cycle of portunity to reduce health

utilization, reduce delays, care—and compares those care costs—with no sacrifice

and eliminate activities that costs to outcomes. in outcomes—is astounding.

don’t improve outcomes.

value problem: how to deliver improved outcomes at The remedy to that are best addressed in a coordinated way and

a lower total cost. the cost crisis should be broadly defined to include common com-

Fortunately, we can change this state of affairs. does not require plications and comorbidities. The cost of treating a

And the remedy does not require medical science medical science patient with diabetes, for example, must include not

breakthroughs or top-down governmental regula- breakthroughs or only the costs associated with endocrinological care

tion. It simply requires a new way to accurately mea- but also the costs of managing and treating associ-

new governmental

sure costs and compare them with outcomes. Our ated conditions such as vascular disease, retinal dis-

regulation. It simply

approach makes patients and their conditions—not ease, and renal disease. For primary and preventive

departmental units, procedures, or services—the

requires a new care, the unit of value measurement is a particular

fundamental unit of analysis for measuring costs and way to accurately patient population—that is, a group with similar pri-

outcomes. The experiences of several major institu- measure costs and mary care needs, such as healthy children or the frail

tions currently implementing the new approach—the compare them with and elderly with multiple chronic conditions.

Head and Neck Center at MD Anderson Cancer Cen- outcomes. Let’s explore the first component of the health

ter in Houston, the Cleft Lip and Palate Program at care value equation: health outcomes. Outcomes for

Children’s Hospital in Boston, and units performing any medical condition or patient population should

knee replacements at Schön Klinik in Germany and be measured along multiple dimensions, including

Brigham & Women’s Hospital in Boston—confirm our survival, ability to function, duration of care, dis-

belief that bringing accurate cost and value measure- comfort and complications, and the sustainability

ment practices into health care delivery can have a of recovery. Better measurement of outcomes will,

transformative impact. by itself, lead to significant improvements in the

value of health care delivered, as providers’ incen-

Understanding the tives shift away from performing highly reimbursed

Value of Health Care services and toward improving the health status of

The proper goal for any health care delivery system patients. Approaches for measuring health care out-

is to improve the value delivered to patients. Value comes have been described previously, notably in

in health care is measured in terms of the patient Michael Porter’s 2010 New England Journal of Medi-

outcomes achieved per dollar expended. It is not cine article, “What Is Value in Health Care?”

the number of different services provided or the vol- While measuring medical outcomes has received

ume of services delivered that matters but the value. growing attention, measuring the costs required to

More care and more expensive care is not necessarily deliver those outcomes, the second component of the

better care. value equation, has received far less attention. In the

To properly manage value, both outcomes and value framework, the relevant cost is the total cost of

cost must be measured at the patient level. Measured all resources—clinical and administrative personnel,

outcomes and cost must encompass the entire cycle drugs and other supplies, devices, space, and equip-

of care for the patient’s particular medical condition, ment—used during a patient’s full cycle of care for a

which often involves a team with multiple specialties specific medical condition, including the treatment

performing multiple interventions from diagnosis to of associated complications and common comorbidi-

treatment to ongoing management. A medical con- ties. We increase the value of health care delivered

dition is an interrelated set of patient circumstances to patients by improving outcomes at similar costs or

September 2011 Harvard Business Review 49

1271 Sep11 Kaplan layout.indd 49 7/27/11 6:08:11 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE

by reducing the total costs involved in patients’ care tools in place, health care providers can utilize medi-

while maintaining the quality of outcomes. cal staff, equipment, facilities, and administrative re-

A powerful driver of value in health care is that sources far more efficiently, streamline the path of

better outcomes often go hand in hand with lower to- patients through the system, and select treatment

tal care cycle costs. Spending more on early detection approaches that improve outcomes while eliminat-

and better diagnosis of disease, for example, spares ing services that do not.

patients suffering and often leads to less complex

and less expensive care later. Reducing diagnostic The Challenges of Health Care Costing

and treatment delays limits deterioration of health Accurate cost measurement in health care is chal-

and also lowers costs by reducing the resources re- lenging, first because of the complexity of health care

quired for care. Indeed, the potential to improve out- delivery itself. A patient’s treatment involves many

comes while driving down costs is greater in health different types of resources—personnel, equipment,

care than in any other field we have encountered. space, and supplies—each with different capabilities

The key to unlocking this potential is combining an and costs. These resources are used in processes that

accurate cost measurement system with the system- start with a patient’s first contact with the organiza-

atic measurement of outcomes. With these powerful tion and continue through a set of clinical consulta-

Myth #1

Charges are a good surrogate for provider costs.

The widespread confusion between deeply flawed assumption that every estimates are not systematically mea-

what a provider charges, what it is billable event in a department has the sured or confirmed in practice settings.

actually reimbursed, and its costs is a same profit margin. Reimbursement- Reimbursing physicians on the basis of

major barrier to reducing the cost of based costing also buries the costs of highly aggregate and likely inaccurate

health care. Providers have aggravated valuable but nonbillable events, such estimates of their costs introduces

this problem by structuring impor- as patient consultations, in large over- major incentive problems into the

tant aspects of their costing systems head pools that are allocated arbitrarily health care system. But the problems

around the way they are reimbursed. and inaccurately to billable events. are compounded when the reimburse-

In the U.S., this is partly a histori- Although costing systems for physi- ment rates are also used to allocate

cal artifact of the Medicare cost-plus cian services differ from those used by physician costs to patients, a purpose

reimbursement system, which requires hospitals, they suffer from the same for which they were never intended.

hospital departments to prepare an problems. As is the case for hospitals, We need to abandon the idea that

annual Medicare Cost Report (MCR), U.S. physicians are reimbursed not on charges billed or reimbursements paid

detailing costs and charges by depart- the basis of an individual patient’s re- in any way reflect costs. In reality, the

ment. Rather than developing and source use but on average estimates of cost of using a resource—a physician,

maintaining accurate costing systems relative demands—relative value units, nurse, case manager, piece of equip-

that are based on actual resource or RVUs—on physician labor, practice ment, or square meter of space—is the

usage, separate from the regulatory expenses, and malpractice expenses same whether the resource is perform-

standard required for reimbursement, in performing billable activities. These ing a poorly or a highly reimbursed

hospitals defaulted to reimbursement- resource estimates are derived from service. Cost depends on how much of

driven systems. specialty panels and national surveys a resource’s available capacity (time)

Unfortunately, that approach was of physicians, who stand to gain from is used in the care for a particular pa-

flawed from the start because it was overestimating the time and complex- tient, not on the charge or reimburse-

based on the use of highly aggregate ity of their work. Despite the required ment for the service, or whether it is

data for estimating costs and the sign-off by government payors, the RVU reimbursed at all.

1271 Sep11 Kaplan layout.indd 50 7/27/11 6:08:12 PM

HBR.ORG

FURTHER READING

FROM THE AUTHORS

MEASURING VALUE

AND OUTCOMES

tions, treatments, and administrative processes until spends with each resource. (See Robert S. Kaplan

the patient’s care is completed. The path that the pa- and Steven R. Anderson’s “Time-Driven Activity- “What Is Value in

tient takes through the system depends on his or her Based Costing,” HBR 2004.) Health Care?”

by M.E. Porter

medical condition. In its initial implementation, such a costing sys- New England Journal of

The already complex path of care is further com- tem may appear complex. But the complexity arises Medicine, 2010

plicated by the highly fragmented way in which not from the methodology but from today’s idiosyn-

Redefining Health Care:

health care is delivered today. Numerous distinct and cratic delivery system, with its poorly documented Creating Value-Based

largely independent organizational units are involved processes for treating patients with particular condi- Competition on Results

in treating a patient’s condition. Care is also idiosyn- tions and its inability to map asset and expense cat- by M.E. Porter and

E.O. Teisberg

cratic; patients with the same condition often take egories to patient processes. As health care providers Harvard Business Review

different paths through the system. The lack of stan- begin to reorganize into units focused on conditions, Press, 2006

dardization stems to some extent from the artisanal standardize their protocols and treatment processes,

“A Strategy for Health

nature of medical practice—physicians in the same and improve their information systems, using the Care Reform: Towards a

organizational unit performing the same medical TDABC system will become much simpler. Value-Based System”

process (for instance, total knee replacement) often To see how TDABC works in the health care con- by M.E. Porter

New England Journal of

use different procedures, drugs, devices, tests, and text, we first explore a simplified example. Medicine, 2009

equipment. In operational terms, you might describe

health care today as a highly customized job shop. Costing the Patient: A Simple Example

TIME-DRIVEN

Existing costing systems, which measure the Consider Patient Jones, who makes an outpatient ACTIVITY-BASED

costs of individual departments, services, or sup- visit to a clinic. To estimate the total cost of Jones’s COSTING

port activities, often encourage the shifting of costs care, we first identify the processes he undergoes

Time-Driven Activity-

from one type of service or provider to another, or and the resources used in each process. Let’s assume Based Costing:

to the payor or consumer. The micromanagement of that Jones uses an administrative process for check- A Simpler and More

costs at the individual organizational unit level does in, registration, and obtaining documentation for Powerful Path to

Higher Profits

little to reduce total cost or improve value—and may third-party reimbursement; and a clinical process by R.S. Kaplan and

in fact destroy value by reducing the effectiveness of for treatment. Just three clinical resources are re- S.R. Anderson

care and driving up administrative costs. (For more quired: an administrator (Allen), a nurse (White), Harvard Business Review

Press, 2007

on the problems with current costing systems, see and a physician (Green).

the three Myth sidebars.) We begin by estimating the first of the two param- Cost and Effect: Using

Any accurate costing system must, at a fundamen- eters: the quantity of time (capacity) the patient uses Integrated Cost Systems

To Drive Profitability and

tal level, account for the total costs of all the resources of each resource at each process. From information Performance

used by a patient as she or he traverses the system. supplied by the three staffers, we learn that Jones by R.S. Kaplan and

That means tracking the sequence and duration of spent 18 minutes (0.3 hours) with Administrator R. Cooper

Harvard Business Review

clinical and administrative processes used by individ- Allen, 24 minutes (0.4 hours) with Nurse White for Press, 1998

ual patients—something that most hospital informa- a preliminary examination, and nine minutes (0.15

tion systems today are unable to do. This deficiency hours) with Physician Green for the direct examina-

can be addressed; technology advances will soon tion and consultation.

greatly improve providers’ ability to track the type Next, we calculate the capacity cost rate for each

and amount of resources used by individual patients. resource—that is, how much it costs, per hour or

In the meantime, it is possible to determine the pre- per minute, for a resource to be available for patient-

dominant paths followed by patients with a particular related work—using the following equation:

medical condition, as our pilot sites have done.

With good estimates of the typical path an indi- Capacity Cost Expenses Attributable to Resourcei

Rate for Resourcei = Available Capacity of Resource

vidual patient takes for a medical condition, provid- i

ers can use the time-driven activity-based costing The numerator aggregates all the costs associated

(TDABC) system to assign costs accurately and rela- with supplying a health care resource, such as Allen,

tively easily to each process step along the path. This White, or Green. It starts with the full compensation

improved version of activity-based costing requires of each person, including salary, payroll taxes, and

that providers estimate only two parameters at each fringe benefits such as health insurance and pen-

process step: the cost of each of the resources used sions. To that we add the costs of all other associated

in the process and the quantity of time the patient resources that enable Allen, White, and Green to be

September 2011 Harvard Business Review 51

1271 Sep11 Kaplan layout.indd 51 7/27/11 6:08:27 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE HBR.ORG

available for patient care. These typically include a Let’s assume that similar calculations yield

pro rata share of costs related to employee supervi- capacity cost rates for Administrator Allen and

sion, space (the offices each staffer uses), and the Physician Green of $45 per hour and $300 per hour,

equipment, information technology, and telecom- respectively.

munications each uses in the normal course of work. We calculate the total cost of Jones’s visit to the fa-

In this way, the cost of many of the organization’s cility by simply multiplying the capacity cost rate of

shared or support resources can be assigned to the each resource by the time (in hours) Jones spent using

resources that directly interact with the patient. the resource, and then adding up the components:

Supervision cost, for example, can be calculated As this example

on the basis of how many people a manager super- demonstrates, ac- (0.3 hours × $45)

(0.4 hours × $65)

vises. Space costs are a function of occupancy area curately calculating + (0.15 hours × $300)

and rental rates; IT costs are based on an individual’s the cost of delivering Total cost of visit: $84.50

use of computers and communications products and health care is quite

services. Assume that we find Nurse White’s total straightforward under the TDABC system. Although

cost to be as follows: the example is admittedly simplified, it captures al-

most all the fundamental concepts any health care

Annual compensation provider needs to apply to estimate the cost of treat-

(including fringe benefits) $65,000 ing patients over their full cycles of care.

Supervision cost By capturing all the costs over the complete cycle

(10% of nursing supervisor’s full cost) $9,000 of care for an individual patient’s medical condition,

Occupancy (9 sq. meters of space we allow providers and payors to address virtually

@ $1,200/sq. meter/year) $10,800 any costing question. Providers can aggregate and

Technology and support $2,560 analyze patients’ cost of care by age, gender, and

Annual total cost of Nurse White $87,360 comorbidity, or by treatment facility, physician, em-

Monthly total cost of Nurse White $7,280 ployer, and payor. They can calculate total and aver-

age costs for any category or subcategory of patients

We next calculate Nurse White’s availability for while still capturing the detailed data on individual

patient care—the denominator of our capacity cost patients needed to understand the sources of cost

rate equation. This calculation starts with 365 days variation within each category.

per year and subtracts all the time that the employee

is not available for work. The calculation for Nurse The Cost Measurement Process

White is as follows: Moving beyond the simplified example, let’s now

look at the seven steps our pilot sites are using to

Start with 365 days per year estimate the total costs of treating their patient

less weekend days 104 populations.

less vacation days 20 1. Select the medical condition. We begin by

less holidays 12 specifying the medical condition (or patient popula-

less sick days 5 tion) to be costed, including the associated compli-

224 available days per year cations and comorbidities that affect processes and

18.7 days per month resources used during the patient’s care. For each

condition, we define the beginning and end of the

Start with 7.5 hours per available day patient care cycle. For chronic conditions, we choose

less scheduled breaks (hours) 0.5 a care cycle for a period of time, such as a year.

less meetings, training, education 1.0 2. Define the care delivery value chain. Next,

Available clinical hours 6 hours per day we specify the care delivery value chain (CDVC),

which charts the principal activities involved in a

Nurse White is therefore available for patient patient’s care for a medical condition along with

work 112 hours per month (6 hours a day for 18.7 their locations. The CDVC focuses providers on

days). Dividing the monthly cost of the resource the full care cycle rather than on individual pro-

($7,280) by monthly capacity (112 hours) gives us cesses, the typical unit of analysis for most process

Nurse White’s capacity cost rate: $65 per hour. improvements and lean initiatives in health care.

52 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 52 7/27/11 6:08:28 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE HBR.ORG

CREATING A COST

MEASUREMENT

SYSTEM

1Select the medical

condition and/or (The exhibit “The Care Delivery Value Chain” shows who needs a laryngoscopy as part of her clinical visit

patient population the CDVC developed with the Brigham & Women’s requires an additional process step. The time esti-

to be examined pilot site for patients with severe knee osteo- mate and associated incremental resources required

arthritis.) This overall view of the patient care cycle can be easily added to the overall time equation for

2Define the care

helps to identify the relevant dimensions along

which to measure outcomes and is also the start-

ing point for mapping the processes that make up

that patient. (See again the process map exhibit.)

To estimate standard times and time equations,

our pilot sites have found it useful to bring together

delivery value chain each activity. all the people involved in a set of processes for fo-

3. Develop process maps of each activity in cused discussion. In the future, we expect providers

3Develop process

patient care delivery. Next we prepare detailed

process maps for each activity in the care delivery

will use electronic handheld, bar-code, and RFID

devices to capture actual times, especially if TDABC

value chain. Process maps encompass the paths becomes the generally accepted standard for mea-

maps of each activ-

patients may follow as they move through their suring the cost of patient care.

ity in patient care

care cycle. They include all the capacity-supplying 5. Estimate the cost of supplying patient

delivery; identify the

resources (personnel, facilities, and equipment) in- care resources. In this step, we estimate the direct

resources involved

volved at each process along the path, both those costs of each resource involved in caring for patients.

and any supplies

directly used by the patient and those required to The direct costs include compensation for employ-

used for the patient

make the primary resources available. (The exhibit ees, depreciation or leasing of equipment, supplies,

at each process

“New-Patient Process Map” shows a process map for or other operating expenses. These data, gathered

one segment of the patient care cycle at the MD An- from the general ledger, the budgeting system, and

4Obtain time

derson Head and Neck Center.) In addition to identi-

fying the capacity-supplying resources used in each

other IT systems, become the numerator for calcu-

lating each resource’s capacity cost rate.

estimates for each process, we identify the consumable supplies (such We must also account for the time that many

process step as medications, syringes, catheters, and bandages) physicians, particularly in academic medical centers,

used directly in the process. These do not have to be spend teaching and doing research in addition to their

5Estimate the cost

shown on the process maps.

Our pilot sites used several approaches for creat-

ing process maps. Some project teams interviewed

clinical responsibilities. We recommend estimating

the percentage of time that a physician spends on

clinical activities and then multiplying the physi-

of supplying each clinicians individually to learn about patient flow, cian’s compensation by this percentage to obtain the

patient care while others organized “power meetings” in which amount of pay accounted for by the physician’s clini-

resource people from multiple disciplines and levels of man- cal work. The remaining compensation should be

agement discussed the process together. Even at this assigned to teaching and research activities.

6Estimate the practi-

early stage in the project, the sessions occasionally

identified immediate opportunities for process and

Next, we identify the support resources neces-

sary to supply the primary resources providing pa-

cost improvement. tient care. For personnel resources, as illustrated in

cal capacity of each

4. Obtain time estimates for each process. the Patient Jones example, these include supervising

resource provider,

We also estimate how much time each provider or employees, space and furnishings (office and patient

and calculate the

other resource spends with a patient at each step in treatment areas), and corporate functions that sup-

capacity cost rate

the process. When a process requires multiple re- port patient-facing employees. When calculating the

sources, we estimate the time required by each one. cost of supplies, we include the cost of the resources

7Compute the total

For short-duration, inexpensive processes that

vary little across patients, we recommend using stan-

used to acquire them and make them available for

patient use during the treatment process (for in-

costs over each pa- dard times (rather than investing resources to record stance, purchasing, receiving, storage, sterilization,

tient’s cycle of care actual ones). Actual duration should be calculated and delivery).

for time-consuming, less predictable processes, es- Finally, we need to allocate the costs of depart-

pecially those that involve multiple physicians and ments and activities that support the patient-facing

nurses performing complex care activities such as work. We map those processes as we did in step 3

major surgery or examination of patients with com- and then calculate and assign costs to patient-facing

plicated medical circumstances. resources on the basis of their demands for the ser-

TDABC is also well suited to capture the effect vices of these departments, using the process that

of process variation on cost. For example, a patient will be described in step 6.

54 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 54 7/27/11 6:08:28 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE

CASE STUDY: THE CARE DELIVERY VALUE CHAIN

Severe Knee Osteoarthritis Requiring Replacement

The care delivery value chain is both a descriptive and prescriptive tool. By systematically mapping the full set

of activities delivered over the cycle of care for a medical condition, spanning multiple providers and nonclinical

care settings, the CDVC enables analysis of how the set of activities together generates patient value and offers

providers a systematic approach to analyze, improve, and integrate the configuration of care delivery.

INFORMING • Importance of • Meaning of diagnosis • Setting expectations • Expectations for • Importance of rehab • Importance of

AND exercise, weight recovery adherence exercise, maintaining

ENGAGING • Prognosis (short- • Importance of

reduction, proper and long-term nutrition, weight loss, • Importance of rehab • Longitudinal care healthy weight

What do nutrition outcomes) vaccinations plan

patients • Post-surgery risk

need to be • Drawbacks and • Home preparation factors

educated benefits of surgery

about?

MEASURING • Joint-specific • Loss of cartilage • Baseline health • Blood loss • Infections • Joint-specific

What measures symptoms and • Change in status • Operative time • Joint-specific symptoms and

need to be function (e.g., subchondral bone • Fitness for surgery symptoms and function

collected? WOMAC scale) • Complications

• Joint-specific (e.g., ASA score) function • Weight gain or loss

• Overall health (e.g.,

SF-12 scale) symptoms and • Inpatient length • Missed work

function of stay • Overall health

• Overall health • Ability to return to

normal activities

ACCESSING • PCP office • Specialty office • Specialty office • Operating room • Nursing facility • Specialty office

Where do

patient care • Health club • Imaging facility • Pre-op evaluation • Recovery room • Rehab facility • Primary care office

activities take • Physical therapy clinic center • Orthopedic floor at • Physical therapy • Health club

place? hospital or specialty clinic

surgery center • Home

TYPICAL PATH OF PATIENT CARE

MONITORING/ DIAGNOSING PREPARING INTERVENING RECOVERING/ MONITORING/

PREVENTING REHABBING MANAGING

CARE MONITOR IMAGING Overall prep ANESTHESIA SURGICAL MONITOR

DELIVERY • Conduct PCP exam • Perform and evaluate • Conduct home • Administer • Immediate return to • Consult regularly

What activities • Refer to specialists, MRI and x-ray assessment anesthesia (general, OR for manipulation, with patient

are performed if necessary –Assess cartilage loss • Monitor weight loss epidural, or if necessary

at each stage? –Assess bone regional) MANAGE

alterations MEDICAL

PREVENT SURGICAL PREP • Prescribe

SURGICAL • Monitor coagulation prophylactic

• Prescribe anti- CLINICAL EVALUATION • Perform cardiology, PROCEDURE

inflammatory pulmonary LIVING antibiotics when

medicines • Review history and evaluations • Determine approach needed

imaging (e.g., minimally • Provide daily living

• Recommend exercise • Run blood labs invasive) support (showering, • Set long-term

regimen • Perform physical dressing) exercise plan

exam • Conduct pre-op • Insert device

• Set weight loss targets physical exam • Track risk indicators • Revise joint, if

• Recommend • Cement joint necessary

treatment plan (fever, swelling,

(surgery or other PAIN MANAGEMENT other)

options) • Prescribe preemp- PHYSICAL THERAPY

tive multimodal pain

ORTHOPEDIC meds • Daily or twice daily

SURGEON PT sessions

For more on the CDVC, see Redefining Health Care: Creating Value-Based Competition on Results, by M.E. Porter and E.O. Teisberg (Harvard Business Review Press, 2006).

This approach to allocating support costs repre- When costing support departments, a good

sents a major shift from current practice. To illustrate, guideline is the “rule of 1.” Support functions that

let’s compare the allocation of the resources required have only one employee can be treated as a fixed

in a centralized department to sterilize two kinds of cost; they can be either not allocated at all or allo-

surgical tool kits, those used for total knee replace- cated using a simplistic method, as is currently done.

ment and those used for cardiac bypass. Existing But departments that have more than one person or

cost systems tend to allocate higher sterilization more than one unit of any resource represent vari-

costs to cardiac bypass cases than to knee replace- able costs. The workload of these departments has

ment cases because the charges (or direct costs) are expanded because of increased demand for the ser-

higher for a cardiac bypass than for a knee replace- vices and outputs they provide. Their costs should

ment. Under TDABC, however, we have learned that and can be assigned on the basis of the patient pro-

more time and expense are required to sterilize the cesses that create demand for their services.

typically more complex knee surgery tools, so rela- Project teams tasked with estimating the cost to

tively higher sterilization costs should be assigned to supply resources—the numerator of the capacity

knee replacements. cost rate—should have expertise in finance, human

56 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 56 7/27/11 6:08:28 PM

Myth #2

resources, and information systems. They can do Hospital overhead costs

this work in parallel with the process mapping and

time estimation (steps 3 and 4) performed by clini-

are too complex to allocate

cians and team members with expertise in quality accurately.

management and process improvement.

6. Estimate the capacity of each resource, Most health care leaders will eventually accept the idea that

and calculate the capacity cost rate. Deter- the direct costs of patient care, such as nurses, physicians, and

mining the practical capacity for employees—the consumable supplies (drugs, bandages, and syringes), ought to

denominator in the capacity cost rate equation—re- be assigned more accurately to individual patients. But many

quires three time estimates, which are gathered from leaders believe that allocating the costs of indirect and support

HR records and other sources: units cannot be done except with crude, arbitrary methods,

a. The total number of days that each employee often dressed up to look sophisticated. Typically, they use a

actually works each year. “peanut butter” method, which spreads overhead and sup-

b. The total number of hours per day that the em- port costs across each department’s billable activities (see

ployee is available for work. Myth #1) using metrics such as the size of direct costs, head

c. The average number of hours per workday used count, length of stay, assigned physical space, number of

for nonpatient-related work, such as breaks, training, patients, number of procedures, RVUs supplied, or costs-

education, and administrative meetings. to-charge ratios (Myth #1 again).

The effect of such arbitrary support-department al-

Monthly Practical a × (b c)

= 12 ⁻

Capacity of Resource locations on the measured cost of services can be pro-

found. In the past, Schön Klinik, like other hospitals in

For physicians who divide their time among clinical, Germany, had reduced the capacity of its total knee

research, and education activities, we subtract time replacement rehabilitation units in part because the

spent on research and education activities to obtain existing cost system portrayed them as less profit-

the number of hours per month that they are avail- able than acute-care units. During Schön Klinik’s cost

able for clinical work. pilot, the project team discovered that the existing

For equipment resources, we measure capacity cost system allocated support-department costs

by estimating the number of days per month and the largely on the basis of length of patient stay, not on

number of hours per day that each piece of equip- the patient’s use of support resources. Since Schön

ment can be used. This represents the upper limit on total knee replacement patients spent 75% of their

the capacity of the equipment. The actual capacity stay in the rehab facility, rehab had been allocated

utilization of much health care equipment is some- about 75% of support department costs.

times lower because equipment capacity is sup- The TDABC analysis showed, however, that the de-

plied in large lumps. For instance, suppose a piece mand for many support-unit services, such as medi-

of equipment can do 10,000 blood tests a month. A cal billing, is far higher during the days a patient

hospital decides to buy the equipment knowing that spends in the acute-care facility than during rehab

it needs to process only 6,000 tests per month. In days. With support costs properly assigned, the rehab

this case, we make an adjustment: The costing sys- facility showed improved profitability. Schön Klinik be-

tem should use the time required to perform 6,000 gan to contemplate the expansion of its rehabilitation

tests as the capacity of the resource. Otherwise, the capacity—a complete reversal of its previous decision—

tests actually performed on the equipment will, at and shifted its focus more intensively on reducing sup-

best, cover only 60% of its cost. If the provider sub- port costs incurred during the acute-care stay.

sequently ends up using the equipment for a higher Once indirect costs have been accurately assigned,

number of tests, it can adjust the capacity rate managers and physicians can look for ways to reduce

accordingly. demand for support-department services and improve

This treatment of capacity follows the rule of 1 and the efficiency with which they are delivered. That, in turn,

should be applied when the organization has only will enable organizations to lower their spending on these

one unit of the equipment. Now suppose a provider resources.

has 12 facilities that each use equipment capable of

performing 10,000 blood tests per month—but each

facility performs only 6,000 tests per month. In that

1271 Sep11 Kaplan layout.indd 57 8/9/11 9:17:22 AM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE

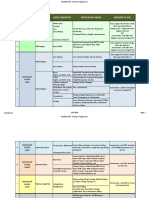

New-Patient

Process Map

This process map

describes a seg-

ment of the patient

case, the capacity of each resource unit should be set processes and restructure care delivery. Capitalizing care cycle at MD

at the full 10,000 tests per month, not its expected on these value-creating opportunities—previously

Anderson Head

number. We want the system to signal the cost of hidden by inadequate and siloed costing systems—

and Neck Center.

unused capacity when a provider chooses to supply is the key to solving the health care cost problem.

capacity at multiple locations or facilities rather than Let’s examine some of the most promising opportu-

Process maps

consolidating its use of expensive equipment. nities that proper costing reveals. show the resources

In addition to the lumpiness with which capac- Eliminate unnecessary process variations required for each

ity gets acquired, factors such as peak load demands, and processes that don’t add value. In our pilots, activity and often

surge capacity, and capacity acquired for future we have documented significant variation in the reveal immediate

growth should be accounted for. This applies to both processes, tools, equipment, and materials used by opportunities for

equipment and personnel. (Those factors can be in- physicians performing the same service within the process improve-

corporated, but the treatment is beyond the scope same unit in the same facility. For example, in total ment and cost

of this article.) knee replacement, surgeons use different implants, reduction.

In practice, we have found that underutilization surgical kits, surgeons’ hoods, and supplies, thereby

of expensive equipment capacity is often not a con- introducing substantial cost variation in treating pa-

scious decision but a failure of the costing system tients with the same condition at the same site. The

to provide visibility into resource utilization. That surgical unit now measures the costs and outcomes

problem is corrected by the TDABC approach. We that each surgeon produces. As a result, clinical

describe opportunities to improve resource capacity practice leaders are able to have more constructive

utilization later in the article. and better informed discussions about how best to

To calculate the resource capacity cost rate, we standardize care and treatment processes to reduce

simply divide the resource’s total cost (step 5) by its the costs of variability and limit the use of expensive

practical capacity (step 6) to obtain a rate, measured approaches and materials that do not demonstrably

in dollars or euros per unit of time, typically an hour lead to improved outcomes.

or a minute. In addition to reducing process variations, our

7. Calculate the total cost of patient care. pilot sites have eliminated steps or entire processes

Steps 3 through 6 establish the structure and data that did not improve outcomes. Schön Klinik, for

components of the TDABC system. In the final step, example, lowered costs by reducing the breadth of

the project team estimates the total cost of treating a tests included in its common laboratory panel after

patient by simply multiplying the capacity cost rates learning that many of the tests did not provide new

(including associated support costs) for each re- information that would lead to improvement in

source used in each patient process by the amounts outcomes.

of time the patient spent with the resource (step 4). Comparing practices across different countries

Sum up all the costs across all the processes used for the same condition also reveals major opportuni-

during the patient’s complete cycle of care to pro- ties for improvement. The reimbursement for a total

duce the total cost of care for the patient. joint replacement care cycle in Germany and Swe-

den is approximately $8,500, including all physician

Opportunities to Improve Value and technical services and excluding only outpatient

Our new approach actively engages physicians, clini- rehabilitation. The comparable figure in U.S. medi-

cal teams, administrative staff, and finance profes- cal centers is $30,000 or more. Since providers in all

sionals in creating the process maps and estimating three countries report, in aggregate, similar margins

the resource costs involved in treating patients over on joint replacement care, U.S. providers’ costs are

their care cycle. This bridges the historical divide be- likely two to three times as high as those of their

tween managers and clinical teams that has often led European counterparts. By comparing process maps

to tensions and stalemates over cost-cutting steps. and resource costs for the same medical condition

TDABC builds a common information platform that across multiple sites, we can determine how much of

will unleash innovation based on a shared under- the cost difference is attributable to variations in pro-

standing of the actual processes of care. Even at our cesses, protocols, and productivity and how much is

pilot site Schön Klinik, which already had an excel- attributable to differences in resource or supply costs

lent departmental cost-control system, introducing such as wages and implant prices. Our initial research

TDABC revealed powerful new ways to improve its suggests that although inputs are more expensive in

58 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 58 7/27/11 6:08:38 PM

HBR.ORG

Registration and Plan of Care Plan of Care

Verification Intake Clinician Visit Discussion Scheduling

Resources: Receptionist, patient access Nurse, receptionist MD, mid-level Registered nurse, medical doctor, Patient service

specialist, interpreter provider, medical patient service coordinator coordinator

assistant, patient

service coordina-

Patient arrives tor, RN

Check in patient; Verify patient Assess patient; Initiate patient Discuss plan Review plan of Schedule tests

communicate information; assemble paper- workup; review of care care; introduce and consults;

arrival complete con- work; place patient history; MD team; review communicate

RCPT, PAS patient in room conduct physi- schedule for schedule to

sent forms patient

2 PAS RN cal exam

MLP

return visit

RN PSC

MIN

40 20 45 30 15 5

MIN MIN MIN MIN MIN MIN

Clean room;

Patient

complete paper-

Laryngoscopy NO work; check

Receptionist needed? e-mail and voice- Scheduled

90%

mail for updates for same day?

Interpreter

or changes to

RN Registered Nurse plan of care

YES RN

MLP Mid-Level Provider 10%

10 YES

90%

MA Medical Assistant MIN

MD Medical Doctor Perform

laryngoscopy

PAS Patient Access Specialist

MD, MA, PSC

Enter next

process

PSC Patient Service Coordinator

10 Changes to

MIN plan of care? NO

90%

NO

10%

YES

10%

Patient

Notify patient departs

of changes

RN

30

MIN

the United States, the higher cost in U.S. facilities is nation and delays when a patient is handed off from

mainly due to lower resource productivity. one specialty or service to the next. Another cause of

Improve resource capacity utilization. The low resource utilization is having specialized equip-

TDABC approach identifies how much of each re- ment available just in case the need arises. Some

source’s capacity is actually used to perform pro- facilities that serve patients with unpredictable and

cesses and treat patients versus how much is unused rare medical needs make a deliberate decision to

and idle. Managers can clearly see the quantity and carry extra capacity. In such cases, an understanding

cost of unused resource capacity at the level of in- of the actual cost of excess capacity should trigger a

dividual physicians, nurses, technicians, pieces of discussion on how best to consolidate the treatment

equipment, administrators, or organizational units. of such patients. Much excess resource capacity,

Resource utilization data also reveal where increas- however, is due not to rare conditions or poor hand-

ing the supply of certain resources to ease bottle- offs but to the prevailing tendency of many hospi-

necked processes would enable more timely care tals and clinics to provide care for almost every type

and serve more patients with only modestly higher of medical problem. Such fragmentation of service

expenditures. lines introduces costly redundancy throughout the

When managers have greater visibility into areas health care system. It can also lead to inferior out-

where substantial and expensive unused capacity comes when providers handle a low volume of cases

exists, they can identify the root causes. For ex- of each type. Accurate costing gives managers a

ample, some underutilization of expensive space, valuable tool for consolidating patient care for low-

equipment, and personnel is caused by poor coordi- volume procedures in fewer institutions, which

September 2011 Harvard Business Review 59

1271 Sep11 Kaplan layout.indd 59 7/27/11 6:08:38 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE

would both reduce the high costs of unused capacity physicians and other skilled staff members require

and improve outcomes. their level of expertise and training. The process

Deliver the right processes at the right lo- maps developed for TDABC often reveal opportuni-

cations. Many services today are delivered in over- ties for appropriately skilled but lower-cost health

resourced facilities or facilities designed for the most care professionals to perform some of the processes

complex patient rather than the typical patient. By currently performed by physicians without adversely

accurately measuring the cost of delivering the affecting outcomes. Such substitutions would free

same services at different facilities, rather than us- up physicians and nurses to focus on their highest-

ing figures based on averaged direct costs and inac- value-added roles. (For an example from one of our

curate overhead allocations, providers are able to pilot sites, see the sidebar “A Cancer Center Puts the

see opportunities to perform particular services at New Approach to Work.”)

properly resourced and lower-cost locations. Such Speed up cycle time. Health care providers

realignment of care delivery, already under way at have multiple opportunities to reduce cycle times for

Children’s Hospital Boston, improves the value and treating patients, which in turn will reduce demand

convenience of more routine services for both pa- for resource capacity. For example, reducing the

tients and caregivers while allowing tertiary facilities time that patients have to wait will reduce demand

to concentrate their specialized resources on truly for patient supervision and space. Speeding up cycle

complex care. time also improves outcomes, both by minimizing

Match clinical skills to the process. Re- the duration of patient uncertainty and discomfort

source utilization can also be improved by examin- and by reducing the risk of complications and mini-

ing whether all the processes currently performed by mizing disease progression. As providers improve

Myth #3

Most health care costs are fixed.

Many health care system participants, If most costs were fixed, growth in ment inattention, not of the nature

including economists and accoun- demand for health care would increase of those costs.

tants, believe that most costs in only that small fraction of costs that Space costs are also not fixed.

health care are fixed because so much are variable, leading to lower average Space is perhaps an organization’s

care is delivered using shared staff, costs in the system, not the dramati- most fungible resource. If demand for

space, and equipment. The result of cally higher share of GDP now being space is reduced, units can be consoli-

this misguided thinking is that cost devoted to health care. dated into smaller space, and excess

reduction efforts tend to focus on only To understand why most health space can be repurposed, sold, or sub-

the small fraction of costs seen as care costs are not fixed, start with leased. Similarly, equipment costs can

variable, such as drugs and supplies, personnel costs, which are gener- be avoided if changes in processes,

which are sometimes referred to as ally at least 50% of the total costs treatment protocols, or patient mix

marginal or incremental costs. This of health care providers, according eliminate the demand for the re-

myth also motivates some health care to American Hospital Association sources. Equipment no longer needed

organizations to expand through merg- statistics. Hint: Personnel costs are can be retired or sold to other health

ers, acquisitions, and organic growth not fixed. Hospital executives can set care institutions that are expanding

in order to reap economies of scale the quantity, mix, and compensation their capacity.

by spreading their fixed costs over an of their personnel each year, or even All told, we estimate that upwards

increased volume of business. more frequently. Personnel costs are of 95% of what health care manag-

But if most health care costs were fixed only when executives allow them ers think of as fixed costs are actually

truly fixed, we would not have the to be. The claim that personnel costs under their control and therefore not

health care cost problem we do today. are fixed is a reflection of manage- really fixed.

60 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 60 7/27/11 6:08:39 PM

HBR.ORG

their process flows and reduce redundancy, their PILOT

patients will no longer have to be so “patient” as they

receive a complete cycle of care.

Optimize over the full cycle of care. Health

care providers today are typically organized around

A Cancer

Center Puts

specialties and services, which complicates coordi-

nation, interrupts the seamless, integrated flow of

patients from one process to the next, and leads to

the duplication of many processes. In the typical

care delivery process, for example, patients see mul-

tiple providers in multiple locations and undergo

a separate scheduling interaction, check-in, medi-

cal consultation, and diagnostic workup for each

one. This wastes resources and creates delays. The

The New

TDABC model makes visible the high costs of these

redundant administrative and clinical processes,

motivating professionals from different depart-

ments to work together to integrate care across de-

Approach

partments and specialties. Eliminating unnecessary

administrative and clinical processes represents one

of the biggest opportunities for lowering costs.

With a complete picture of the time and resources

involved, providers can optimize across the entire

To Work

care cycle, not just the parts. Physicians and staff by Heidi W. Albright, MHA, and Thomas W. Feeley, MD

may shift more of their time and resources to the

front end of the care cycle—to activities such as pa-

tient education and clinical team consultations—to

reduce the likelihood of patients experiencing far

more costly complications and readmissions later in

T

the cycle.

Additionally, this resource- and process-based ap- he University of Texas MD Anderson Cancer Center

proach gives providers visibility into valuable non- is a National Cancer Institute–designated Compre-

billed events in the cycle of care. These activities— hensive Cancer Center, located in Houston, Texas.

such as nurse counseling time, physician phone Seeing more than 30,000 new patients every year,

calls to patients, and multidisciplinary care team MD Anderson accounts for approximately 20% of

meetings—can often make major contributions to cancer care within the Houston region and 1% of

efficiency and favorable outcomes. Because existing cancer care nationally. MD Anderson is a medical

systems hide these costs in overhead (see Myth #1), condition–focused center that provides integrated,

such important elements of care are prone to be min- interdisciplinary care across the care cycle.

imized or left unmanaged. In collaboration with Michael Porter, we em-

barked on a major effort to expand clinical outcome measurement, begin-

Capturing the Payoffs ning with a study of 2,468 patients in the Head and Neck Center, in 2008.

“Calculating the return on investment of perfor- We created the Institute for Cancer Care Excellence in December 2008 to

mance improvement has been missing from most of support this effort. In 2010, with Robert Kaplan, we launched a pilot project,

the quality improvement discussions in health care,” also within the Head and Neck Center, to assess the feasibility of applying

Dr. Thomas Feeley at MD Anderson told us. “When modern cost accounting to health care delivery.

measurement does occur, the assumptions are usu- Traditionally, at MD Anderson, we used a charge-based cost accounting

ally gross, inaccurate, and sometimes overstated,” system. However, we realized that its cost allocations were problematic at

he added. “TDABC gave us a powerful tool to actu- several levels. For a start, the drivers of cost in health care had changed

ally model the effect an improvement will have on but the allocation methodology had not, with the result that our costing no

costs.” Accurate costing allows the impact of process CONTINUED ON NEXT PAGE

September 2011 Harvard Business Review 61

1271 Sep11 Kaplan layout.indd 61 7/27/11 6:08:52 PM

HBR.ORG

improvements to be readily calculated, validated, lead to reduced spending on resources that are no

and compared. longer needed. Managers also have the informa-

The big payoff occurs when providers use accu- tion they need to redeploy resources freed up as a

rate costing to translate the various value-creating result of process improvements. Leaders gain a tool

opportunities into actual spending reductions. A they never had before: a way to link decisions about

cruel fact of life is that total costs will not actually fall patient needs and treatment processes directly to

unless providers issue fewer and smaller paychecks, resource spending.

consume less (and less expensive) space, buy fewer

supplies, and retire or dispose of excess equipment. Reinventing Reimbursement

Facing revenue pressure due to lower reimburse- If we are to stop the escalation of total health care

ments—particularly from government programs costs, the level of reimbursement must be reduced.

such as Medicare and Medicaid—providers today But how this is done will have profound implications

use a hatchet approach to cost reduction by mandat- for the quality and supply of health care. Across-the-

ing arbitrary cuts across departments. That approach board cuts in reimbursement will jeopardize the

jeopardizes both the quality and the supply of care. quality of care and likely lead to severe rationing.

With accurate costing, providers can target their Reductions that enable the quality of care to be main-

cost reductions in areas where real improvements in tained or improved need to be informed by accurate

When providers understand the total costs of treating

patients over their complete cycle of care, they can

contemplate innovative reimbursement approaches without

fear of sacrificing their financial sustainability.

resource utilization and process efficiencies enable knowledge of the total costs required to achieve the

providers to spend less without having to ration care desired outcomes when treating individual patients

or compromise its quality. with a given medical condition.

Health care organizations today, like all other The current system of reimbursement is discon-

firms, conduct arduous and time-consuming budget- nected from actual costs and outcomes and discour-

ing and capacity planning processes, often accompa- ages providers and payors from introducing more

nied by heated arguments, power negotiations, and cost-effective processes for treating patients. With

frustration. Such difficulties are symptomatic of in- today’s inadequate costing systems, reimbursement

adequate costing systems and can be avoided. rates have often been based on historical charges.

A TDABC budgeting process starts by predict- That approach has introduced massive cross subsi-

ing the volume and types of patients the provider dies that reimburse some services generously and

expects. Using these forecasts combined with the pay far below costs for others, leading to excess

process maps for treating each patient condition, supply for well-reimbursed services and inadequate

providers can predict the quantity of resource hours delivery and innovation for poorly reimbursed ones.

required. This can then be divided by the practical Adjusting only the level of reimbursement, how-

capacity of each resource type to obtain accurate es- ever, will not be enough. Any true health care reform

timates of the quantity of each resource needed to will require abandoning the current complex fee-for-

meet the forecasted demand. Estimated monthly service payment schedule altogether. Instead, pay-

expense budgets for future periods can be easily ors should introduce value-based reimbursement,

obtained by multiplying the quantity of each re- such as bundled payments, that covers the full care

source category required by the monthly cost of each cycle and includes care for complications and com-

resource. mon comorbidities. Value-based reimbursement

In this way, managers can make virtually all rewards providers who deliver the best overall care

their costs “variable.” They can readily see how ef- at the lowest cost and who minimize complications

ficiency improvements and process innovations rather than create them. The lack of accurate cost

September 2011 Harvard Business Review 63

1271 Sep11 Kaplan layout.indd 63 7/27/11 6:09:12 PM

THE BIG IDEA HOW TO SOLVE THE COST CRISIS IN HEALTH CARE HBR.ORG

Accurate costing allows the impact of

process improvements to be readily

calculated, validated, and compared.

data covering the full cycle of care for a patient has numbers, they can make bold and politically difficult

been the major barrier to adopting alternative reim- decisions to lower costs while sustaining or improv-

bursement approaches, such as bundled reimburse- ing outcomes. Dr. Jens Deerberg-Wittram, a senior

ment, that are more aligned with value. executive at Schön Klinik, told us, “A good costing

We believe that our proposed improvements in system tells you which areas are worth addressing

cost measurement, coupled with better outcome and gives you confidence to have the difficult discus-

measurement, will give third-party payors the con- sions with medical professionals.” As providers and

fidence to introduce reimbursement methods that payors better understand costs, they will see numer-

better reward value, reduce perverse incentives, and ous opportunities to achieve a true “bending of the

encourage provider innovation. As providers start to cost curve” from within the system, not in response

understand the total costs of treating patients over to top-down mandates. Accurate costing also un-

their complete cycle of care, they will also be able to locks a whole cascade of opportunities, such as pro-

contemplate innovative reimbursement approaches cess improvement, better organization of care, and

without fear of sacrificing their financial sustainabil- new reimbursement approaches that will accelerate

ity. Those that deliver desired health outcomes faster the pace of innovation and value creation. We are

and more efficiently, without unnecessary services, struck by the sheer size of the opportunity to reduce

and with proven, simpler treatment models will not the cost of health care delivery with no sacrifice in

be penalized by lower revenues. outcomes. Accurate measurement of costs and out-

comes is the previously hidden secret for solving the

ACCURATELY MEASURING costs and outcomes is the health care cost crisis. HBR Reprint R1109B

single most powerful lever we have today for trans-

The authors would like to acknowledge the extensive and

forming the economics of health care. As health care invaluable assistance of Mary Witkowski, Dr. Caleb Stowell,

leaders obtain more accurate and appropriate costing and Craig Szela in the preparation of this article.

CARTOON: CHRIS WILDT

“Actually, I don’t know who these people are. They came with the frame.”

64 Harvard Business Review September 2011

1271 Sep11 Kaplan layout.indd 64 7/27/11 6:09:13 PM

You might also like

- Answers To Competency Assessment SectionDocument16 pagesAnswers To Competency Assessment Sectionapi-209542414100% (1)

- Healthcare White PaperDocument4 pagesHealthcare White Paperramakanta_sahu100% (1)

- Harvard Business Review on Fixing Healthcare from Inside & OutFrom EverandHarvard Business Review on Fixing Healthcare from Inside & OutNo ratings yet

- Taurian Curriculum Framework Grade 12 BIODocument8 pagesTaurian Curriculum Framework Grade 12 BIOpummyg100% (1)

- Classroom Readiness ChecklistDocument2 pagesClassroom Readiness ChecklistRoseman Tumaliuan100% (1)

- Nursing Care of A Family With An InfantDocument26 pagesNursing Care of A Family With An InfantJc GarciaNo ratings yet

- Porter y Kapplan (2011)Document18 pagesPorter y Kapplan (2011)ANA MARIA RIOSNo ratings yet

- HPN6Document50 pagesHPN6Joy MichaelNo ratings yet

- Cleveland HelpingDocument33 pagesCleveland HelpingHyma SandraNo ratings yet

- Will Increasing Primary Care Spending Alone Save Money?Document2 pagesWill Increasing Primary Care Spending Alone Save Money?anonNo ratings yet

- What Does The RAND Health Insurance ExperimentDocument3 pagesWhat Does The RAND Health Insurance ExperimentsunnyNo ratings yet

- 5 Quality Measures That Matter For Value-Based CareDocument8 pages5 Quality Measures That Matter For Value-Based CareTuan Nguyen DangNo ratings yet

- Value and Payment in Sleep Medicine JCSM 2018Document4 pagesValue and Payment in Sleep Medicine JCSM 2018cjbae22No ratings yet

- Comprehensive Health Care Reform and Biomedical InnovationDocument21 pagesComprehensive Health Care Reform and Biomedical InnovationcashelNo ratings yet

- Reducing Healthcare Costs: The Physician Perspective OnDocument7 pagesReducing Healthcare Costs: The Physician Perspective OnJeddy Zawadi GeeNo ratings yet

- Defining and Implementing Value-Based Health Care - A Strategic FrameworkDocument4 pagesDefining and Implementing Value-Based Health Care - A Strategic FrameworkQuang Danh PhạmNo ratings yet

- How Would Medicare For All Affect Health System Capacity? Evidence From Medicare For SomeDocument2 pagesHow Would Medicare For All Affect Health System Capacity? Evidence From Medicare For SomeCato InstituteNo ratings yet

- Defensiva - 3Document14 pagesDefensiva - 3Alexandra MateiNo ratings yet

- Better Ways To Pay For Health Care FOCUSDocument8 pagesBetter Ways To Pay For Health Care FOCUSCristhian LarrahondoNo ratings yet

- What Is Value-Based Healthcare - NEJM CatalystDocument3 pagesWhat Is Value-Based Healthcare - NEJM CatalystRémi DANHOUNDONo ratings yet

- An RX For Health Care Woes - CPAs and Firms Can Manage Health Care Costs NowDocument4 pagesAn RX For Health Care Woes - CPAs and Firms Can Manage Health Care Costs NowJill Edmonds, Communications DirectorNo ratings yet

- Reducing Administrative Costs and Improving The Health Care SystemDocument4 pagesReducing Administrative Costs and Improving The Health Care Systemrongse@gmail.comNo ratings yet

- Future Healthcare Value Based Healthcare Is It The Way Forward 002Document5 pagesFuture Healthcare Value Based Healthcare Is It The Way Forward 002amiraNo ratings yet

- 2013 Current Challenges To Academic Health CentersDocument2 pages2013 Current Challenges To Academic Health CentersIkramIzatNo ratings yet

- Ctu Medication ManagementnovoiceDocument12 pagesCtu Medication Managementnovoiceapi-240028260No ratings yet

- Who Is Driving The Interest in OualityDocument10 pagesWho Is Driving The Interest in Oualitymzahid7823No ratings yet

- 40 A National Strategy Pp982 990Document9 pages40 A National Strategy Pp982 990cma909No ratings yet

- Making Health Reform WorkDocument26 pagesMaking Health Reform WorkCenter for American ProgressNo ratings yet

- EpisodeBasedPayment PerspectivesforConsiderationDocument24 pagesEpisodeBasedPayment PerspectivesforConsiderationHazelnutNo ratings yet

- Approaches To Physician Payment The Deconstruction Primary CareDocument6 pagesApproaches To Physician Payment The Deconstruction Primary CarerianberlianproductiveNo ratings yet

- Driving GrowthDocument6 pagesDriving GrowthsolomonNo ratings yet

- Appropriate Use of Reference Pricing CanDocument5 pagesAppropriate Use of Reference Pricing CansunnyNo ratings yet

- Value-Based Insurance Design Landscape DigestDocument35 pagesValue-Based Insurance Design Landscape DigestNational Pharmaceutical CouncilNo ratings yet

- Health Delivery ch2Document20 pagesHealth Delivery ch2JeffersonNo ratings yet

- HealthcareTransformers ValueBasedHealthcareDocument30 pagesHealthcareTransformers ValueBasedHealthcareamiraNo ratings yet

- Controlling Health Care CostsDocument3 pagesControlling Health Care CostsAthanassios VozikisNo ratings yet

- Consumer Driven Health CareDocument9 pagesConsumer Driven Health CareKevin VarnerNo ratings yet

- The Effect of Pay-For-Performance in Hospitals: Lessons For Quality ImprovementDocument9 pagesThe Effect of Pay-For-Performance in Hospitals: Lessons For Quality ImprovementMasrun FatanahNo ratings yet

- Comprehensive Care PhysicianDocument9 pagesComprehensive Care PhysiciannurNo ratings yet

- How Much The Quality of Healthcare Costs? A Challenging Question!Document2 pagesHow Much The Quality of Healthcare Costs? A Challenging Question!Mehak KhannaNo ratings yet

- 305T Paper 4Document8 pages305T Paper 4Emery SteeleNo ratings yet

- BCG Next Generation Medical Management - v3Document14 pagesBCG Next Generation Medical Management - v3Sumit Kumar AwkashNo ratings yet

- "Indumbent" Healthcare Thinking: Prices Don't MatterDocument5 pages"Indumbent" Healthcare Thinking: Prices Don't MatterDavid W. JohnsonNo ratings yet

- Kelompok 3Document9 pagesKelompok 3Yunny FaustineNo ratings yet

- Actuarial Value: A Method For Comparing Health Plan BenefitsDocument12 pagesActuarial Value: A Method For Comparing Health Plan BenefitsParakh AhoojaNo ratings yet

- Cost Accounting in Healthcare PDFDocument8 pagesCost Accounting in Healthcare PDFfilosofal62100% (2)

- How To Make Market Competition Work in Healthcare: Kerianne H. Holman, MD, and Rodney A. Hayward, MDDocument5 pagesHow To Make Market Competition Work in Healthcare: Kerianne H. Holman, MD, and Rodney A. Hayward, MDMichael RandolphNo ratings yet

- Allen - Impacts of Pay For Performance On The Quality of Primary CareDocument9 pagesAllen - Impacts of Pay For Performance On The Quality of Primary Carekevinbgt99No ratings yet

- Home Care Position Paper 4 5 111 PDFDocument20 pagesHome Care Position Paper 4 5 111 PDFRichard HutasoitNo ratings yet

- Nihms 1032116Document12 pagesNihms 1032116TeresaSM19No ratings yet

- BCG Paying For Value in Health Care September 2019 - tcm9 227552Document32 pagesBCG Paying For Value in Health Care September 2019 - tcm9 227552Anand KumarNo ratings yet

- Decision-Making in Healthcare As A Complex Adaptive System: Craig KuziemskyDocument4 pagesDecision-Making in Healthcare As A Complex Adaptive System: Craig KuziemskyChofi SaezNo ratings yet

- Jama 2019 14603Document2 pagesJama 2019 14603Craig WangNo ratings yet

- Thinking Outside The Box Moving The Respiratory Care ProfessionDocument9 pagesThinking Outside The Box Moving The Respiratory Care Professionnicomat85No ratings yet

- KH AHA Benefits of Hospital Mergers Acquisitions 2021 10 08Document20 pagesKH AHA Benefits of Hospital Mergers Acquisitions 2021 10 08Amr AhmedNo ratings yet

- The Beginner's Guide To New Health Care Payment Models - BrookingsDocument7 pagesThe Beginner's Guide To New Health Care Payment Models - BrookingsMaca Vera RiveroNo ratings yet

- Delivery System WhitepaperDocument12 pagesDelivery System Whitepapernchc-scribdNo ratings yet

- Aligning Reimbursement With Value - Institute For Strategy and Competitiveness - Harvard Business SchoolDocument1 pageAligning Reimbursement With Value - Institute For Strategy and Competitiveness - Harvard Business SchoolTuan Nguyen DangNo ratings yet

- Does The Doctor Need A Boss?, Cato Briefing Paper No. 111Document12 pagesDoes The Doctor Need A Boss?, Cato Briefing Paper No. 111Cato InstituteNo ratings yet

- Identifying and Resolving Disputes in New Accountable Care SettingsDocument10 pagesIdentifying and Resolving Disputes in New Accountable Care SettingsRothHealthLawNo ratings yet

- Chapter 5 - Provider Reimbursement MethodsDocument18 pagesChapter 5 - Provider Reimbursement MethodsAdityaNo ratings yet

- Health Affairs Blog Appropriate Use of Reference Pricing Can Increase Value PrintDocument5 pagesHealth Affairs Blog Appropriate Use of Reference Pricing Can Increase Value PrintBrett BernsteinNo ratings yet

- Value Based Pricing 2Document6 pagesValue Based Pricing 2Kavita SubramaniamNo ratings yet

- Textbook of Urgent Care Management: Chapter 22, Health Plan ContractingFrom EverandTextbook of Urgent Care Management: Chapter 22, Health Plan ContractingNo ratings yet

- Daftar Pustaka DiserasiDocument297 pagesDaftar Pustaka Diserasibayu prabuNo ratings yet

- 1 PBDocument8 pages1 PBbayu prabuNo ratings yet

- Dampak Psikologis Tenaga Kesehatan Selama Pandemi COVID-19: Brian Pinggian, Hendri Opod, Lydia DavidDocument8 pagesDampak Psikologis Tenaga Kesehatan Selama Pandemi COVID-19: Brian Pinggian, Hendri Opod, Lydia DavidM. Arif ArrahmanNo ratings yet

- Call For Abstract TF6 T20Document3 pagesCall For Abstract TF6 T20bayu prabuNo ratings yet

- Penentuan Kelayakan Finansial Usaha Produksi Pupuk Abc Pada CV - Xyz Dusun Sebotu Kabupaten SanggauDocument8 pagesPenentuan Kelayakan Finansial Usaha Produksi Pupuk Abc Pada CV - Xyz Dusun Sebotu Kabupaten SanggauArif SetiajayaNo ratings yet