You might also like

- ReSA AP Quiz 5B43Document42 pagesReSA AP Quiz 5B43Rafael Bautista75% (4)

- HSE Event Reporting and Management StandardDocument37 pagesHSE Event Reporting and Management StandardRenatoNo ratings yet

- Module 7 - Merchandising Business Special TransactionsDocument40 pagesModule 7 - Merchandising Business Special TransactionsMaria Nicole OroNo ratings yet

- Module 12 Just in Time and Backflush CostingDocument14 pagesModule 12 Just in Time and Backflush CostingMarjorie NepomucenoNo ratings yet

- Chapter 10 Entrepreneurial Ventures: Management, 14e (Robbins/Coulter)Document74 pagesChapter 10 Entrepreneurial Ventures: Management, 14e (Robbins/Coulter)Mohannad Elabbassi100% (1)

- Just in Time and Backflush CostingDocument12 pagesJust in Time and Backflush CostingBea ChristineNo ratings yet

- PAS 2 - InventoriesDocument26 pagesPAS 2 - InventoriesAnn Margarette LopezNo ratings yet

- Chapter 6-Accounting For Merchandising TransactionsDocument30 pagesChapter 6-Accounting For Merchandising Transactions05 Phạm Hồng Diệp12.11No ratings yet

- Review - IV: Nature of Inventory and Cost of Goods SoldDocument10 pagesReview - IV: Nature of Inventory and Cost of Goods SoldAmrutaNo ratings yet

- Inventories NotesDocument7 pagesInventories NotesJessel Ann MontecilloNo ratings yet

- UnPlanned Delivery Cost 1701802185Document9 pagesUnPlanned Delivery Cost 1701802185vamsiNo ratings yet

- Accounting For Corporations: ACT B861FDocument54 pagesAccounting For Corporations: ACT B861FCalvin MaNo ratings yet

- Inventories: PERIODIC SYSTEM-physical Counting of Goods OnDocument4 pagesInventories: PERIODIC SYSTEM-physical Counting of Goods OnGirl Lang AkoNo ratings yet

- Cost of Sales & InventoriesDocument17 pagesCost of Sales & InventoriesShashank100% (1)

- Lect 11TVDocument25 pagesLect 11TVsalman siddiqui100% (1)

- Cheat SheetDocument15 pagesCheat SheetJason wonwonNo ratings yet

- Chapter 18 Revenue RecognitionDocument4 pagesChapter 18 Revenue Recognitionridho_wijoyo100% (1)

- Working Capital and Operating CycleDocument24 pagesWorking Capital and Operating Cyclesaurabh chaturvediNo ratings yet

- Accounting For Managers: Professor ZHOU NingDocument38 pagesAccounting For Managers: Professor ZHOU Ningdev4c-1No ratings yet

- Working Capital ManagementDocument80 pagesWorking Capital ManagementDharmendarNo ratings yet

- Class No 14 & 15Document31 pagesClass No 14 & 15WILD๛SHOTッ tanvirNo ratings yet

- Cost Accounting Chapters 1&2Document7 pagesCost Accounting Chapters 1&2ralfgerwin inesaNo ratings yet

- Chapter 6 - Accounting For MerchandiseDocument30 pagesChapter 6 - Accounting For MerchandiseTrần Anh TuấnNo ratings yet

- Ma Am+saira s+Tutorial+Slides-Chap+6+-+Inventories PDFDocument17 pagesMa Am+saira s+Tutorial+Slides-Chap+6+-+Inventories PDFAli Zain ParharNo ratings yet

- Marathon Session (Part 08) - Class NotesDocument68 pagesMarathon Session (Part 08) - Class NotesSiya GoyalNo ratings yet

- Inventories 2024Document27 pagesInventories 2024Charish Ann SimbajonNo ratings yet

- HO 10 Inventories IAS 2Document7 pagesHO 10 Inventories IAS 2rhailNo ratings yet

- Chapter-3 - Working Capital MGTDocument57 pagesChapter-3 - Working Capital MGTRaunak YadavNo ratings yet

- Chapter 6-CLCDocument19 pagesChapter 6-CLCVăn ThànhNo ratings yet

- Ap-500Q: Quizzer On Purchasing/Disbursement Production and Revenue/Receipt Cycles: Audit of Inventories, Receivables and Cash and Cash EquivalentsDocument27 pagesAp-500Q: Quizzer On Purchasing/Disbursement Production and Revenue/Receipt Cycles: Audit of Inventories, Receivables and Cash and Cash Equivalentsruel c armillaNo ratings yet

- UNIT VI JIT SystemDocument7 pagesUNIT VI JIT SystemBerch TreeNo ratings yet

- FAR3 - InventoryDocument17 pagesFAR3 - InventoryBeing TuluvaNo ratings yet

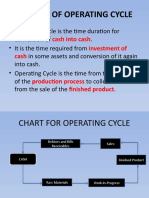

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocument6 pagesConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaNo ratings yet

- Chapter 8 InventoryDocument11 pagesChapter 8 Inventorymarwan2004acctNo ratings yet

- Toaz - Info Afar Backflush Costing With Answers 1 PRDocument5 pagesToaz - Info Afar Backflush Costing With Answers 1 PRNicole Andrea TuazonNo ratings yet

- Need of Working Capital & Concept of Operating Cyycle: Presented By:-G.Venket Ramana Ujjayani PatraDocument11 pagesNeed of Working Capital & Concept of Operating Cyycle: Presented By:-G.Venket Ramana Ujjayani PatraVenket RamanaNo ratings yet

- Chapter 6-Accounting For Merchandising TransactionsDocument30 pagesChapter 6-Accounting For Merchandising Transactions05 Phạm Hồng Diệp12.11No ratings yet

- Chapter 5Document3 pagesChapter 5Phạm MiuNo ratings yet

- Module 8 - Inventories Part IIDocument14 pagesModule 8 - Inventories Part IIMark Christian BrlNo ratings yet

- AfM 9 - Merchants & InventoryDocument27 pagesAfM 9 - Merchants & InventoryjaymursalieNo ratings yet

- Chapter 2 Inventories For UseDocument18 pagesChapter 2 Inventories For UseawlachewNo ratings yet

- Acct LL MotiDocument64 pagesAcct LL Motinewaybeyene5No ratings yet

- Reviewer For Integrated Accounting Finals Term 1Document12 pagesReviewer For Integrated Accounting Finals Term 1yellowNo ratings yet

- Periodic and Perpetual Inventory SystemsDocument17 pagesPeriodic and Perpetual Inventory SystemsMichael Brian TorresNo ratings yet

- Chapter 5 InventoriesDocument48 pagesChapter 5 InventoriesJude Joaquin SanchezNo ratings yet

- Chapter 1, InventoriesDocument18 pagesChapter 1, InventoriesAmsaluNo ratings yet

- InventoriesDocument30 pagesInventoriesMac FerdsNo ratings yet

- Integartion OBYC SAP FI MMCCDocument57 pagesIntegartion OBYC SAP FI MMCCAriba TestingNo ratings yet

- Chapter5 JustinTimeandBackflushAccountingDocument21 pagesChapter5 JustinTimeandBackflushAccountingFaye Nepomuceno-Valencia0% (1)

- Chapter 2 InventoriesDocument56 pagesChapter 2 InventoriesFerdelyn FuentesNo ratings yet

- TOPIC 1 Accounting For InventoryDocument9 pagesTOPIC 1 Accounting For Inventorykirah raraNo ratings yet

- Acc Reviewer P2Document5 pagesAcc Reviewer P2Shane QuintoNo ratings yet

- Module 7 13 No 11Document6 pagesModule 7 13 No 11LEIGHANNE ZYRIL SANTOSNo ratings yet

- Discussion - InventoriesDocument3 pagesDiscussion - InventoriesVel JuneNo ratings yet

- Acctg. Ed 1 - Module 10 Accounting Cycle of A Merchandising BusinessDocument35 pagesAcctg. Ed 1 - Module 10 Accounting Cycle of A Merchandising BusinessChen Hao100% (1)

- Accounts ReceivableDocument54 pagesAccounts ReceivableFrancine Thea M. LantayaNo ratings yet

- Chapter 6 - Inventories Lecture NotesDocument41 pagesChapter 6 - Inventories Lecture Notesminhndn21405No ratings yet

- Chapter 5 Inventories Exercises Answer Guide Summer AY2122 PDFDocument10 pagesChapter 5 Inventories Exercises Answer Guide Summer AY2122 PDFwavyastroNo ratings yet

- Who Are We?: Inventory Inclusion and ExclusionDocument12 pagesWho Are We?: Inventory Inclusion and ExclusionShey INFTNo ratings yet

- FI Entries For MTO ScenarioDocument3 pagesFI Entries For MTO ScenarioAchanti Dp100% (1)

- Chapter 4Document32 pagesChapter 4Đặng TrangNo ratings yet

- Chapter 5Document41 pagesChapter 5Đặng TrangNo ratings yet

- Chapter 3Document60 pagesChapter 3Đặng TrangNo ratings yet

- Chapter 2Document65 pagesChapter 2Đặng TrangNo ratings yet

- Inventory ManagementDocument51 pagesInventory ManagementMay Jovi JalaNo ratings yet

- Cease Desist Order TrinityDocument10 pagesCease Desist Order TrinitydaneNo ratings yet

- 410-MC9-UM ADVANCED TOPICS v01 Class6Document30 pages410-MC9-UM ADVANCED TOPICS v01 Class6LlanraeyNo ratings yet

- Ap Prob 8Document2 pagesAp Prob 8jhobsNo ratings yet

- Audit and Assurance June 2009 Past Paper (Question)Document6 pagesAudit and Assurance June 2009 Past Paper (Question)Serena JainarainNo ratings yet

- Questions Exam Mathematics and Game Theory 2019-2020Document5 pagesQuestions Exam Mathematics and Game Theory 2019-2020silNo ratings yet

- Aaf020-1 Sem2 As02m Data SetDocument7 pagesAaf020-1 Sem2 As02m Data SetThảo NguyễnNo ratings yet

- Lecture 3Document14 pagesLecture 3Lol 123No ratings yet

- Factors of Production Final PresentationDocument54 pagesFactors of Production Final Presentationlucky zee86% (7)

- Reflection The CorporationDocument2 pagesReflection The CorporationRuhani Kimpa100% (1)

- ObjectivesDocument71 pagesObjectivesEbenezer AkaluNo ratings yet

- Gen Com 1772010Document56 pagesGen Com 1772010Rohit JainNo ratings yet

- MBA FrameworksDocument19 pagesMBA FrameworksPraneeth PatnaikNo ratings yet

- Financial Distress Thesis-1Document80 pagesFinancial Distress Thesis-1Asaminew DesalegnNo ratings yet

- HR Metrics Implementation atDocument2 pagesHR Metrics Implementation atElena KolokythaNo ratings yet

- De Beers Natural Monopoly: 1. A Lack of SubstitutesDocument3 pagesDe Beers Natural Monopoly: 1. A Lack of SubstitutesRaljon SilverioNo ratings yet

- Module 8 - Inventories Part IIDocument14 pagesModule 8 - Inventories Part IIMark Christian BrlNo ratings yet

- Commoditygoldmprojoject13 15ramanjineyulu13f21e0062 150621155556 Lva1 App6892 PDFDocument60 pagesCommoditygoldmprojoject13 15ramanjineyulu13f21e0062 150621155556 Lva1 App6892 PDFMohsen RaeesNo ratings yet

- SDM Unit Test I Que PaperDocument6 pagesSDM Unit Test I Que PaperRaghuNo ratings yet

- 1.6 Store Internal Audit Check List: Auditor Name - Dipak Shelke Auditee Name - Omkar Sali, Pratik ChaudhariDocument2 pages1.6 Store Internal Audit Check List: Auditor Name - Dipak Shelke Auditee Name - Omkar Sali, Pratik ChaudhariDipak ShelkeNo ratings yet

- Ahluwalia, M. S. (2019)Document17 pagesAhluwalia, M. S. (2019)rnjn mhta.No ratings yet

- IELTS MASTER - IELTS Reading Test 11Document14 pagesIELTS MASTER - IELTS Reading Test 11fredy paradaNo ratings yet

- BST PROJECT FileDocument5 pagesBST PROJECT FileAR MASTERRNo ratings yet

- Schedule I of Tamil Nadu Stamp ActDocument40 pagesSchedule I of Tamil Nadu Stamp ActYash GangwaniNo ratings yet

- Kyc DetailsDocument37 pagesKyc DetailsTejas Shirsat0% (1)

- Aubank 26042022164457 Ausfb Outcome BMDocument23 pagesAubank 26042022164457 Ausfb Outcome BMrkumar_81No ratings yet

- Background CheckDocument6 pagesBackground CheckErrol BalingbingNo ratings yet

- Total Quality ManagementDocument46 pagesTotal Quality ManagementML ValentinoNo ratings yet