You might also like

- Subsidies & Countervailing 02212014Document32 pagesSubsidies & Countervailing 02212014MargieAnnPabloNo ratings yet

- Countervailing DutyDocument30 pagesCountervailing DutySamuelNo ratings yet

- Subsidies and Counter MeasuresDocument23 pagesSubsidies and Counter MeasuresSeashell LoafingNo ratings yet

- Primer RA8752 (AD)Document11 pagesPrimer RA8752 (AD)Mildred AlegadoNo ratings yet

- Primer AntiDumpingDocument11 pagesPrimer AntiDumpingmitchitan19No ratings yet

- Tariff Commission FAQsDocument7 pagesTariff Commission FAQsFrancisJosefTomotorgoGoingoNo ratings yet

- 3 Anti Dumping DutyDocument20 pages3 Anti Dumping DutyPam PincaNo ratings yet

- Procedure Section713 Rev2 28july 2020Document3 pagesProcedure Section713 Rev2 28july 2020aim zehcnasNo ratings yet

- Special DutiesDocument9 pagesSpecial DutiesMARKNo ratings yet

- Subsidies and Countervailing MeasureDocument29 pagesSubsidies and Countervailing MeasureErika LaguitanNo ratings yet

- Tax 2 Annotations (RAs)Document8 pagesTax 2 Annotations (RAs)Kevin HernandezNo ratings yet

- Subsidy and Countervailing DutyDocument16 pagesSubsidy and Countervailing DutyShaina DalidaNo ratings yet

- Primer RA8800 (SG)Document11 pagesPrimer RA8800 (SG)SamuelNo ratings yet

- Module Tariff6Document13 pagesModule Tariff6J- ArtizNo ratings yet

- Anti DumpingDocument52 pagesAnti DumpingSamuelNo ratings yet

- Imposition of A Countervailing Duty Under Republic Act 8751 - Countervailing Duty Act of 1999Document38 pagesImposition of A Countervailing Duty Under Republic Act 8751 - Countervailing Duty Act of 1999Mariel BoncatoNo ratings yet

- Definition of TermsDocument3 pagesDefinition of TermsMARKNo ratings yet

- N1idn3 IndonesiaDocument52 pagesN1idn3 IndonesiaHarsh GargNo ratings yet

- Anti Dumping DutyDocument5 pagesAnti Dumping DutyyeshanewNo ratings yet

- Customs Reviewer 2017 (Final)Document24 pagesCustoms Reviewer 2017 (Final)Chi Odanra83% (12)

- CountervailingDocument9 pagesCountervailingMA. LORENA CUETONo ratings yet

- Customs Reviewer 2018 (Final)Document25 pagesCustoms Reviewer 2018 (Final)Mamerto Egargo Jr.No ratings yet

- Anti-Dumping Countervailing Measures Safeguard Measures: Trade RemediesDocument17 pagesAnti-Dumping Countervailing Measures Safeguard Measures: Trade RemediesliyaNo ratings yet

- Qdoc - Tips - Customs Reviewer 2017 FinalDocument24 pagesQdoc - Tips - Customs Reviewer 2017 Finalriza mae PandianNo ratings yet

- Basics of CustomDocument17 pagesBasics of CustomKhushboo ParikhNo ratings yet

- ITLP - Notes2Document9 pagesITLP - Notes2Louis MalaybalayNo ratings yet

- C !""##$ C % &C' C (&% C &C C C& C&C (&%) C (+C)Document12 pagesC !""##$ C % &C' C (&% C &C C C& C&C (&%) C (+C)michael ritaNo ratings yet

- Customs Modernization & Tariff Act PDFDocument76 pagesCustoms Modernization & Tariff Act PDFCheryl BaguilatNo ratings yet

- Regras DC DSBDocument35 pagesRegras DC DSBgugamachalaNo ratings yet

- Tariff-Code-2018 BarDocument39 pagesTariff-Code-2018 Barred_inajNo ratings yet

- Trade Remedy Measures IdentificationDocument2 pagesTrade Remedy Measures IdentificationaguilaremmanuelNo ratings yet

- Safeguard MeasuresDocument11 pagesSafeguard MeasuresMargieAnnPabloNo ratings yet

- Wto 1Document45 pagesWto 1Ssg BNo ratings yet

- Current Trends and Govt ActionsDocument3 pagesCurrent Trends and Govt ActionsRohit RoyNo ratings yet

- Ra 8752 Gr1 OutlineDocument5 pagesRa 8752 Gr1 OutlineIELTSNo ratings yet

- Advance Authorization SchemeDocument3 pagesAdvance Authorization SchemeganeshNo ratings yet

- Manual On Anti Dumping, Countervailing Duties and Safeguard MeasuresDocument95 pagesManual On Anti Dumping, Countervailing Duties and Safeguard MeasuresZEUS_Z77No ratings yet

- Tariff and Customs LawsDocument7 pagesTariff and Customs LawsRind Bergh DevelosNo ratings yet

- Executive Order No. 120 S. 1993 and The Implementing Rules and RegulationsDocument17 pagesExecutive Order No. 120 S. 1993 and The Implementing Rules and RegulationsKimberly TimtimNo ratings yet

- Subsidies & Counter..gDocument37 pagesSubsidies & Counter..gSaroj KumarNo ratings yet

- TA6 Safeguard Measures (F)Document39 pagesTA6 Safeguard Measures (F)Heather Brennan100% (1)

- Anti Dumping (Autosaved)Document60 pagesAnti Dumping (Autosaved)Alhysa Rosales CatapangNo ratings yet

- COUNTERVAILINGDocument6 pagesCOUNTERVAILINGMARIA CRISTINA LIMPAGNo ratings yet

- Lecture 4Document26 pagesLecture 4exotic trendsNo ratings yet

- Subsidies and Countervailing Measures - Agreement On Agriculture - 2019-24Document24 pagesSubsidies and Countervailing Measures - Agreement On Agriculture - 2019-24Aparna MukherjeeNo ratings yet

- E-Journal: Vol - Vi Issue No.42 JAN 2008Document16 pagesE-Journal: Vol - Vi Issue No.42 JAN 2008CIERNo ratings yet

- Bureau of Internal RevenueDocument11 pagesBureau of Internal RevenueRomer LesondatoNo ratings yet

- Presentation On SubsidyDocument42 pagesPresentation On SubsidyRajesh KumarNo ratings yet

- TariffDocument5 pagesTariffSunny RajNo ratings yet

- Export Management: Module 8/9Document84 pagesExport Management: Module 8/9Sheikh YajidulNo ratings yet

- Trade Remedies Safeguards: Reporters: John Mark Sunga Reo DagumanDocument14 pagesTrade Remedies Safeguards: Reporters: John Mark Sunga Reo DagumanjmsungaNo ratings yet

- Tariff and Customs CodeDocument26 pagesTariff and Customs CodeRussel SirotNo ratings yet

- Anti DumpingDocument53 pagesAnti DumpingYogesh Bandhu100% (1)

- Orld Rade Rganization: G/SG/N/1/PHL/2Document51 pagesOrld Rade Rganization: G/SG/N/1/PHL/2Tru ColorsNo ratings yet

- Macroeconomics Policies Is Concerned With The Operation of The Economy As A WholeDocument10 pagesMacroeconomics Policies Is Concerned With The Operation of The Economy As A WholeTavanesan MahindramanyNo ratings yet

- Export Promotion Schemes: Promotional Measures in Foreign Trade PolicyDocument4 pagesExport Promotion Schemes: Promotional Measures in Foreign Trade Policymu sicNo ratings yet

- Procedure - Section711 - Rev2 - 28july 2020Document3 pagesProcedure - Section711 - Rev2 - 28july 2020AceNo ratings yet

- Orld Rade Rganization: G/ADP/N/1/COL/3Document36 pagesOrld Rade Rganization: G/ADP/N/1/COL/3Mai NamNo ratings yet

- CTL 201P CLS1B 083019 0015 Rev. 00Document2 pagesCTL 201P CLS1B 083019 0015 Rev. 00LaMinn Paing0% (1)

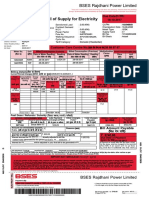

- Bill of Supply For Electricity: BSES Rajdhani Power LimitedDocument4 pagesBill of Supply For Electricity: BSES Rajdhani Power LimitedHema KatiyarNo ratings yet

- 23 Calo vs. RoldanDocument2 pages23 Calo vs. RoldanGilbert YapNo ratings yet

- Hoffman ComplaintDocument9 pagesHoffman ComplaintKenan FarrellNo ratings yet

- External Whistleblowing ProceduresDocument9 pagesExternal Whistleblowing Proceduresgautham kannanNo ratings yet

- A R ANTULAY V R S NAYAKDocument100 pagesA R ANTULAY V R S NAYAKShayan Ghosh50% (2)

- Duties and Tasks of Indonesian PoliceDocument1 pageDuties and Tasks of Indonesian PoliceName ToomNo ratings yet

- Capital One - No Bills DueDocument2 pagesCapital One - No Bills Duesabra el100% (1)

- Accreditation Form 0Document2 pagesAccreditation Form 0MalikNo ratings yet

- Berbano vs. BarcelonaDocument9 pagesBerbano vs. BarcelonaAnisah AquilaNo ratings yet

- Exhibit CDocument62 pagesExhibit Ckbarrier214No ratings yet

- David vs. CADocument2 pagesDavid vs. CAchatmche-06No ratings yet

- LIFEAsia Base System Guide V10.1 LatestDocument291 pagesLIFEAsia Base System Guide V10.1 LatestCM100% (5)

- Bagchi, Towards EqualityDocument14 pagesBagchi, Towards EqualitySuchintan DasNo ratings yet

- Purchase Order: NRE - One Time Engineering CostDocument8 pagesPurchase Order: NRE - One Time Engineering CostChetan PrajapatiNo ratings yet

- Invalid Andhra Pradesh Reorganisation Act, 2014Document37 pagesInvalid Andhra Pradesh Reorganisation Act, 2014N. SasidharNo ratings yet

- Ando V CampoDocument1 pageAndo V CampoAllen Windel BernabeNo ratings yet

- Paw Print Keychain Free Crochet PatternDocument5 pagesPaw Print Keychain Free Crochet PatternDian Dian AyuNo ratings yet

- Petition For NotarialDocument4 pagesPetition For NotarialShirley DayaoNo ratings yet

- Tax Receipt Transport Department, Government of West Bengal Registration Authority UTTAR DINAJPUR RTO, West BengalDocument1 pageTax Receipt Transport Department, Government of West Bengal Registration Authority UTTAR DINAJPUR RTO, West BengalSiwam ChoudharyNo ratings yet

- Itinerary of Travel: Lynette H. CaupayanDocument6 pagesItinerary of Travel: Lynette H. CaupayanlavNo ratings yet

- LME3701 102 2018 3 BDocument8 pagesLME3701 102 2018 3 BT1100% (1)

- Labour Code - I, LW 4012,8th SemDocument9 pagesLabour Code - I, LW 4012,8th SemfxujyrxfNo ratings yet

- Candidate Information SheetDocument4 pagesCandidate Information SheetAman kumarNo ratings yet

- Test Bank For Financial Management Theory and Practice 14th Edition by BrighamDocument36 pagesTest Bank For Financial Management Theory and Practice 14th Edition by Brighammanywisegroschen3ppq100% (28)

- Research Paper On Privacy Laws in IndiaDocument9 pagesResearch Paper On Privacy Laws in IndiaNiharika SinhaNo ratings yet

- PALE Reflection PaperDocument3 pagesPALE Reflection PaperJose MasarateNo ratings yet

- Rent Agreement Jan22Document5 pagesRent Agreement Jan22uday xeroxNo ratings yet

- (Sept 22, 2017) - Lawyers Call With Speedup and Marek - Redacted-V1 - Redacted PDFDocument5 pages(Sept 22, 2017) - Lawyers Call With Speedup and Marek - Redacted-V1 - Redacted PDFDavid HundeyinNo ratings yet

- Triskelion ArticlesDocument15 pagesTriskelion ArticlesBORDALLO JAYMHARKNo ratings yet

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyFrom EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyRating: 5 out of 5 stars5/5 (1)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantFrom EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantRating: 4 out of 5 stars4/5 (104)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (89)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- Happy Go Money: Spend Smart, Save Right and Enjoy LifeFrom EverandHappy Go Money: Spend Smart, Save Right and Enjoy LifeRating: 5 out of 5 stars5/5 (4)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- The Best Team Wins: The New Science of High PerformanceFrom EverandThe Best Team Wins: The New Science of High PerformanceRating: 4.5 out of 5 stars4.5/5 (31)

- How To Budget And Manage Your Money In 7 Simple StepsFrom EverandHow To Budget And Manage Your Money In 7 Simple StepsRating: 5 out of 5 stars5/5 (4)

- Money Management: An Essential Guide on How to Get out of Debt and Start Building Financial Wealth, Including Budgeting and Investing Tips, Ways to Save and Frugal Living IdeasFrom EverandMoney Management: An Essential Guide on How to Get out of Debt and Start Building Financial Wealth, Including Budgeting and Investing Tips, Ways to Save and Frugal Living IdeasRating: 3 out of 5 stars3/5 (1)

- Improve Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouFrom EverandImprove Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouRating: 5 out of 5 stars5/5 (5)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationFrom EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationRating: 4.5 out of 5 stars4.5/5 (18)

- Summary of You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You Want by Jesse MechamFrom EverandSummary of You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You Want by Jesse MechamRating: 5 out of 5 stars5/5 (1)

- Sacred Success: A Course in Financial MiraclesFrom EverandSacred Success: A Course in Financial MiraclesRating: 5 out of 5 stars5/5 (15)

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)From EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Rating: 3.5 out of 5 stars3.5/5 (9)

- Smart, Not Spoiled: The 7 Money Skills Kids Must Master Before Leaving the NestFrom EverandSmart, Not Spoiled: The 7 Money Skills Kids Must Master Before Leaving the NestRating: 5 out of 5 stars5/5 (1)

- The New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningFrom EverandThe New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningRating: 4.5 out of 5 stars4.5/5 (8)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Complete Strategy Guide to Day Trading for a Living in 2019: Revealing the Best Up-to-Date Forex, Options, Stock and Swing Trading Strategies of 2019 (Beginners Guide)From EverandThe Complete Strategy Guide to Day Trading for a Living in 2019: Revealing the Best Up-to-Date Forex, Options, Stock and Swing Trading Strategies of 2019 (Beginners Guide)Rating: 4 out of 5 stars4/5 (34)

- Buy the Milk First: ... and Other Secrets to Financial Prosperity, Regardless of Your IncomeFrom EverandBuy the Milk First: ... and Other Secrets to Financial Prosperity, Regardless of Your IncomeNo ratings yet

- Money Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayFrom EverandMoney Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayRating: 3.5 out of 5 stars3.5/5 (2)

- How to Save Money: 100 Ways to Live a Frugal LifeFrom EverandHow to Save Money: 100 Ways to Live a Frugal LifeRating: 5 out of 5 stars5/5 (1)

- Altcoins Coins The Future is Now Enjin Dogecoin Polygon Matic Ada: blockchain technology seriesFrom EverandAltcoins Coins The Future is Now Enjin Dogecoin Polygon Matic Ada: blockchain technology seriesRating: 5 out of 5 stars5/5 (1)

- Bitcoin Secrets Revealed - The Complete Bitcoin Guide To Buying, Selling, Mining, Investing And Exchange Trading In Bitcoin CurrencyFrom EverandBitcoin Secrets Revealed - The Complete Bitcoin Guide To Buying, Selling, Mining, Investing And Exchange Trading In Bitcoin CurrencyRating: 4 out of 5 stars4/5 (4)

- 109 Personal Finance Tips: Things you Should Have Learned in High SchoolFrom Everand109 Personal Finance Tips: Things you Should Have Learned in High SchoolNo ratings yet