You might also like

- GST Book Bank AnswersDocument10 pagesGST Book Bank AnswersAditya DasNo ratings yet

- Rule 128) : A. ConstitutionDocument20 pagesRule 128) : A. ConstitutionCharles Rivera100% (1)

- Bouviers Law Dictionary and Concise Encyclopedia Vol II 1914 PDFDocument1,130 pagesBouviers Law Dictionary and Concise Encyclopedia Vol II 1914 PDFNETER432100% (3)

- Pal VS CaDocument2 pagesPal VS CaLearsi AfableNo ratings yet

- Decisión Besosa Orden de Mordaza, Revela Documentos Pesquisa SixtoDocument13 pagesDecisión Besosa Orden de Mordaza, Revela Documentos Pesquisa SixtoVictor Torres MontalvoNo ratings yet

- Research Paper M&ADocument15 pagesResearch Paper M&AShrijita GNo ratings yet

- Heirs of Dimaculangan VDocument5 pagesHeirs of Dimaculangan VMeet MeatNo ratings yet

- Acosta v. People, 5 SCRA 774 G.R. No. L-17427 July 31, 1962Document2 pagesAcosta v. People, 5 SCRA 774 G.R. No. L-17427 July 31, 1962Caleb Josh PacanaNo ratings yet

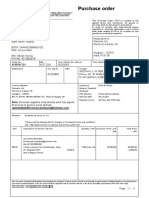

- Purchase OrderDocument3 pagesPurchase OrderSunil kumar SinghNo ratings yet

- Motion To Defer Inpatient Rehab - KEVIN ECHAVEZ BECBECDocument2 pagesMotion To Defer Inpatient Rehab - KEVIN ECHAVEZ BECBECJeddox La Zaga100% (1)

- Vlasons Vs CADocument3 pagesVlasons Vs CARex RegioNo ratings yet

- La. Jimenez vs. Sorongon, G.R. No. 178607, 05 DecemberDocument11 pagesLa. Jimenez vs. Sorongon, G.R. No. 178607, 05 DecemberMaryland AlajasNo ratings yet

- Unbalanced Growth TheoryDocument24 pagesUnbalanced Growth TheorySWETCHCHA MISKA100% (1)

- Dr. Ram Manohar Lohiya National Law University, Lucknow: Subject: Law of Taxation SessionDocument14 pagesDr. Ram Manohar Lohiya National Law University, Lucknow: Subject: Law of Taxation SessionShivam MishraNo ratings yet

- T3 12 Espiritu vs. LimDocument3 pagesT3 12 Espiritu vs. LimLi MarNo ratings yet

- Victorydepot PDFDocument2 pagesVictorydepot PDFAbrar PatelNo ratings yet

- Summer Project Report: "A Comparative Study of GST Return "Document60 pagesSummer Project Report: "A Comparative Study of GST Return "Aditya DaswaniNo ratings yet

- (Delhi) (07 01 2021)Document14 pages(Delhi) (07 01 2021)Akash GuptaNo ratings yet

- Case Laws Singh Caterers and Vendors Vs Union of IndiaDocument2 pagesCase Laws Singh Caterers and Vendors Vs Union of IndiaSWETCHCHA MISKANo ratings yet

- GST Weekly Update - 53 - 2023-24Document4 pagesGST Weekly Update - 53 - 2023-24Sarabjeet SinghNo ratings yet

- Article - GIST of Recent Supreme Court Judgments On GSTDocument5 pagesArticle - GIST of Recent Supreme Court Judgments On GSTsupdtconflNo ratings yet

- GST Update: GST On Merchant Trade TransactionsDocument5 pagesGST Update: GST On Merchant Trade TransactionsvenkatramanNo ratings yet

- 06 Rajashree Foods AAR OrderDocument6 pages06 Rajashree Foods AAR OrderanupNo ratings yet

- 14Nov21-Brochure - Telemedicon-202Document2 pages14Nov21-Brochure - Telemedicon-202TULSI CHARAN DASNo ratings yet

- Shree Balaji Alloys v. CIT (2011) 333 ITR 335 (J&K)Document11 pagesShree Balaji Alloys v. CIT (2011) 333 ITR 335 (J&K)Mahesh ThackerNo ratings yet

- Annexure A Caro Report Revised 2016 - 2017-2018Document7 pagesAnnexure A Caro Report Revised 2016 - 2017-2018Uday ShettyNo ratings yet

- ATL Practice Questions June 2023 290323Document84 pagesATL Practice Questions June 2023 290323sarang chawareNo ratings yet

- Piyush Shamjibhai Vasoya Vs Union of India and OrsGJ2021230621170837110COM917632Document3 pagesPiyush Shamjibhai Vasoya Vs Union of India and OrsGJ2021230621170837110COM917632Subbu RajNo ratings yet

- GPIL Letter of OfferDocument70 pagesGPIL Letter of OfferAmey KadamNo ratings yet

- Edge Techno Chem 24aagfe2710d1z5 GST DetailsDocument4 pagesEdge Techno Chem 24aagfe2710d1z5 GST DetailsvisabltdNo ratings yet

- Challenges Issues Relating To SEZs Under GST RegimeDocument3 pagesChallenges Issues Relating To SEZs Under GST RegimeDeepak KariaNo ratings yet

- question-IDT-GM - 4Document8 pagesquestion-IDT-GM - 4Prajwal AradhyaNo ratings yet

- ZealGlobalServices ProspDocument267 pagesZealGlobalServices ProspvishnuNo ratings yet

- Indian GSTDocument55 pagesIndian GSTShivam KharuleNo ratings yet

- GST Case Law Compendium - March 24 EditionDocument33 pagesGST Case Law Compendium - March 24 Editionvani.gupta300No ratings yet

- NDkySFNWeWUyYTVQbU9KSC85akVaUT09 InvoiceDocument2 pagesNDkySFNWeWUyYTVQbU9KSC85akVaUT09 InvoiceInclusive Education BranchNo ratings yet

- SCS202243656Document2 pagesSCS202243656Jyotiprakash SahooNo ratings yet

- 07.12.2023-GST E-News-LetterDocument2 pages07.12.2023-GST E-News-LetterCA Thirumalesu ENo ratings yet

- Intouch Issue 3 2022Document21 pagesIntouch Issue 3 2022Shermadurai VNo ratings yet

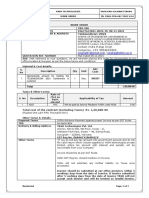

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountBilal Ahmed MultaniNo ratings yet

- Adhyatmik Satsang CaseDocument9 pagesAdhyatmik Satsang CaseDhanvanthNo ratings yet

- Darshan Shetty - Offer LetterDocument2 pagesDarshan Shetty - Offer Letterdarshan shettyNo ratings yet

- Po-21 Aac BlocksDocument1 pagePo-21 Aac Blocksajit.chavanNo ratings yet

- Blackbook COVER PAGE 2021-2022Document52 pagesBlackbook COVER PAGE 2021-2022NikkiNo ratings yet

- Limited Towers, India.: StreetDocument6 pagesLimited Towers, India.: StreetAbhishek khandeliaNo ratings yet

- 16 5 2020 Case Summaries Webinar Adv BadrinarayananDocument11 pages16 5 2020 Case Summaries Webinar Adv Badrinarayanandalip.singhNo ratings yet

- Package Scheme of Incentives in Maharashtra - Is It Actually Incentivizing?Document3 pagesPackage Scheme of Incentives in Maharashtra - Is It Actually Incentivizing?pr_abhatNo ratings yet

- Bhavesh Kiritbhai Kalani Vs Union of India 1904202GJ202116072116544677COM521824Document6 pagesBhavesh Kiritbhai Kalani Vs Union of India 1904202GJ202116072116544677COM521824Subbu RajNo ratings yet

- Aryan ProjectDocument61 pagesAryan ProjectAryan SinghalNo ratings yet

- Notice Pay - Amneal-Pharmaceuticals-Pvt.-Ltd.-GST-AAR-GujratDocument7 pagesNotice Pay - Amneal-Pharmaceuticals-Pvt.-Ltd.-GST-AAR-Gujratashim1No ratings yet

- Alpha - HoneywellDocument2 pagesAlpha - HoneywellASFAN CHAUDHARYNo ratings yet

- Digitally Signed by Sandhya Sethia Date: 2024.05.01 16:38:18 +05'30'Document2 pagesDigitally Signed by Sandhya Sethia Date: 2024.05.01 16:38:18 +05'30'Pratik RajgorNo ratings yet

- (2022) 136 Taxmann - Com 6 (Delhi) - (2022) 91 GST 406 (Delhi) (11-02-2022) Saurabh Mittal vs. Union of IndiaDocument9 pages(2022) 136 Taxmann - Com 6 (Delhi) - (2022) 91 GST 406 (Delhi) (11-02-2022) Saurabh Mittal vs. Union of IndiaAkash GuptaNo ratings yet

- Weekly GST Communique A2Z Taxcorp LLP 18-03-2024Document60 pagesWeekly GST Communique A2Z Taxcorp LLP 18-03-2024xetay24207No ratings yet

- BMOUTCOMEDocument17 pagesBMOUTCOMEakshay kausaleNo ratings yet

- Direct Tax Case LawDocument17 pagesDirect Tax Case Lawsathish_61288@yahooNo ratings yet

- Jeetika Aggarwal-ICA-Tax LawDocument9 pagesJeetika Aggarwal-ICA-Tax Lawshivanjay aggarwalNo ratings yet

- Goods and Services Tax, A/5, Rajya Kar Bhavan, Ashram Road, Ahmedabad - 380 009Document7 pagesGoods and Services Tax, A/5, Rajya Kar Bhavan, Ashram Road, Ahmedabad - 380 009Santosh KumarNo ratings yet

- Ty Bba 5th Sem Project EditedDocument37 pagesTy Bba 5th Sem Project EditedOm AherNo ratings yet

- Mohd Nazim SaifiDocument42 pagesMohd Nazim SaifiNazim SaifiNo ratings yet

- 19-63 Manasvi Pinge - Taxation - II FDDocument14 pages19-63 Manasvi Pinge - Taxation - II FDManasviNo ratings yet

- ITC Denial For Non-Payment To Suppliers - Order QuashedDocument7 pagesITC Denial For Non-Payment To Suppliers - Order QuashedMaunik ParikhNo ratings yet

- Analysis On Supreme Court Judgment in Northern Operating Systems Upholding RCM On Manpower Supply For Secondment EmployeeDocument7 pagesAnalysis On Supreme Court Judgment in Northern Operating Systems Upholding RCM On Manpower Supply For Secondment EmployeeSbs and Company LLPNo ratings yet

- GLKJP'OIKanhs'pikhn PASDDocument3 pagesGLKJP'OIKanhs'pikhn PASDomkar daveNo ratings yet

- Invoice 13dec2023 VIE1LBOV108085 1702457835Document1 pageInvoice 13dec2023 VIE1LBOV108085 1702457835dileep.jcmNo ratings yet

- A Govt CompanyDocument6 pagesA Govt Companyabhiramreddy3No ratings yet

- Final Research Proposal 2024Document19 pagesFinal Research Proposal 2024Sherab ZangmoNo ratings yet

- Digital Assignment-3 Lean Startup Management MGT1022 Submitted To: Prof:Aravind Raj SDocument9 pagesDigital Assignment-3 Lean Startup Management MGT1022 Submitted To: Prof:Aravind Raj SPriya SinghNo ratings yet

- Case Study of Rangaswami v. Registrar of Trade Unions by SivagangaDocument7 pagesCase Study of Rangaswami v. Registrar of Trade Unions by SivagangaSiva Ganga Siva0% (1)

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- Gogte Infrastructure Development Corporation Ltd. AAR KarnatakaDocument7 pagesGogte Infrastructure Development Corporation Ltd. AAR KarnatakaSWETCHCHA MISKANo ratings yet

- Bio Technology Law IDocument6 pagesBio Technology Law ISWETCHCHA MISKANo ratings yet

- Legal Professional Ethics ProjectDocument17 pagesLegal Professional Ethics ProjectSWETCHCHA MISKANo ratings yet

- Bci V Bonnifie Law CollegeDocument7 pagesBci V Bonnifie Law CollegeSWETCHCHA MISKANo ratings yet

- International Environmental LawDocument16 pagesInternational Environmental LawSWETCHCHA MISKANo ratings yet

- Criminal Law Project IIDocument3 pagesCriminal Law Project IISWETCHCHA MISKANo ratings yet

- Law and Poverty ProjectDocument35 pagesLaw and Poverty ProjectSWETCHCHA MISKANo ratings yet

- Amnesty PresentationDocument8 pagesAmnesty PresentationSWETCHCHA MISKANo ratings yet

- Constitution Reaserch PapersDocument27 pagesConstitution Reaserch PapersSWETCHCHA MISKANo ratings yet

- History - II Project WorkDocument28 pagesHistory - II Project WorkSWETCHCHA MISKANo ratings yet

- Political Science Changes Swecha ProjectDocument24 pagesPolitical Science Changes Swecha ProjectSWETCHCHA MISKANo ratings yet

- History II ProjectDocument22 pagesHistory II ProjectSWETCHCHA MISKANo ratings yet

- Torts 18 PagesDocument18 pagesTorts 18 PagesSWETCHCHA MISKANo ratings yet

- Research Paper CRPC 2018LLB124Document28 pagesResearch Paper CRPC 2018LLB124SWETCHCHA MISKANo ratings yet

- Jurisprudence Project IDocument24 pagesJurisprudence Project ISWETCHCHA MISKANo ratings yet

- Criminal Law Reaserch Paper IDocument32 pagesCriminal Law Reaserch Paper ISWETCHCHA MISKANo ratings yet

- Contracts II Reaserch PapersDocument34 pagesContracts II Reaserch PapersSWETCHCHA MISKANo ratings yet

- Family Law Project IDocument26 pagesFamily Law Project ISWETCHCHA MISKANo ratings yet

- Balanced Growth TheoryDocument18 pagesBalanced Growth TheorySWETCHCHA MISKA100% (1)

- Philippine Court Jurisdiction by Grace EDocument4 pagesPhilippine Court Jurisdiction by Grace ELarssen IbarraNo ratings yet

- Ang Mga Kaanib Sa Iglesia NG Dios Kay Kristo Hesus v. Iglesia NG Dios Kay Cristo JesusDocument8 pagesAng Mga Kaanib Sa Iglesia NG Dios Kay Kristo Hesus v. Iglesia NG Dios Kay Cristo JesusCassie GacottNo ratings yet

- Maharashtra National Law University, Mumbai: Life Cycle of A Suit'Document24 pagesMaharashtra National Law University, Mumbai: Life Cycle of A Suit'kjjgv gffxcghklNo ratings yet

- Final Request For Interrogatories in A Debt Collection Suit Instructions, Example and Sample FormDocument5 pagesFinal Request For Interrogatories in A Debt Collection Suit Instructions, Example and Sample FormJames Bradley StoddartNo ratings yet

- Panlilio vs. VictorioDocument2 pagesPanlilio vs. VictorioGilbert YapNo ratings yet

- STAMPF V TRIGG - OpinionDocument32 pagesSTAMPF V TRIGG - Opinionml07751No ratings yet

- ADDITIONAL CASES FULL and DIGESTSDocument17 pagesADDITIONAL CASES FULL and DIGESTSjannagotgoodNo ratings yet

- Moot MemorialDocument14 pagesMoot MemorialNikhil khaleefaNo ratings yet

- Judicial PrecedentDocument3 pagesJudicial Precedentcs4rsrtnksNo ratings yet

- Del Castillo 31-36Document1,161 pagesDel Castillo 31-36Tokie TokiNo ratings yet

- Civil Case 46 of 2015Document16 pagesCivil Case 46 of 2015wanyamaNo ratings yet

- Digest By: Ella Cobol: Saludo V American Express GR No. 159507Document1 pageDigest By: Ella Cobol: Saludo V American Express GR No. 159507Ella CblNo ratings yet

- Criminal Law Practice Test 1Document10 pagesCriminal Law Practice Test 1Emil SamaniegoNo ratings yet

- Demurrer To EvidenceDocument7 pagesDemurrer To EvidenceApril Dawn DaepNo ratings yet

- NCBA 6 Abacus Real Estate V Manila Banking CorpDocument4 pagesNCBA 6 Abacus Real Estate V Manila Banking CorpCol. McCoyNo ratings yet

- Answer (Yek-146)Document8 pagesAnswer (Yek-146)Ilmioamore InfermiereNo ratings yet

- 11.22.21 Re Margaret Garnett's Fraud in US V Ware 17 - 2214 2d CirDocument14 pages11.22.21 Re Margaret Garnett's Fraud in US V Ware 17 - 2214 2d CirThomas WareNo ratings yet

- Ley Construction v. SedanoDocument9 pagesLey Construction v. Sedanomarybianca parolanNo ratings yet

- Arada v. CADocument12 pagesArada v. CAKay QuintanaNo ratings yet

- Update To The Court - Sheriff's OfficeDocument5 pagesUpdate To The Court - Sheriff's OfficeNBC MontanaNo ratings yet