You might also like

- TranscriptDocument6 pagesTranscriptjohn doeNo ratings yet

- Tax 02-Lesson 04 - Property RelationsDocument27 pagesTax 02-Lesson 04 - Property RelationsMama MiyaNo ratings yet

- Lesson 5 PDFDocument14 pagesLesson 5 PDFRitesh AgarwalNo ratings yet

- AGibson 13E Ch10Document24 pagesAGibson 13E Ch10finance tutorNo ratings yet

- Collector of Internal Revenue v. Club Filipino, Inc. de Cebu, GRN-L 12719, May 31, 1962Document2 pagesCollector of Internal Revenue v. Club Filipino, Inc. de Cebu, GRN-L 12719, May 31, 1962Al Jay MejosNo ratings yet

- Corporation Law by Ladia Chapter 3 CasesDocument3 pagesCorporation Law by Ladia Chapter 3 CasesRoxanne PeñaNo ratings yet

- CIR Vs Club Filipino DigestDocument2 pagesCIR Vs Club Filipino DigestJC100% (2)

- Tax Exempt Corporationunder Tha NircDocument13 pagesTax Exempt Corporationunder Tha NircaletheialogheiaNo ratings yet

- Question Bank 1Document11 pagesQuestion Bank 1Pooja MBANo ratings yet

- Association of Non Profit Clubs Vs BIRDocument2 pagesAssociation of Non Profit Clubs Vs BIREllenNo ratings yet

- CIR Vs ST LukeDocument7 pagesCIR Vs ST LukeMark Lester Lee Aure100% (2)

- Collector of Internal Revenue Vs Club Filipino, Inc. de Cebu 5 SCRA 321 (1962)Document4 pagesCollector of Internal Revenue Vs Club Filipino, Inc. de Cebu 5 SCRA 321 (1962)KarlNo ratings yet

- Collector V Club FilipinoDocument6 pagesCollector V Club FilipinoKatrina ManiquisNo ratings yet

- Preparing Analyzing and Forecasting Financial StatementsDocument48 pagesPreparing Analyzing and Forecasting Financial StatementsDumplings DumborNo ratings yet

- CIR V Club FilipinoDocument2 pagesCIR V Club FilipinoMark TanoNo ratings yet

- Collector of Internal Revenue v. Club Filipino, Inc. de CebuDocument2 pagesCollector of Internal Revenue v. Club Filipino, Inc. de CebuJosephine Redulla LogroñoNo ratings yet

- HRM732 Final Exam Review Practice Questions SUMMER 2022Document12 pagesHRM732 Final Exam Review Practice Questions SUMMER 2022Rajwinder KaurNo ratings yet

- Title: Commissioner of Internal Revenue vs. St. Luke's Medical Center, IncDocument3 pagesTitle: Commissioner of Internal Revenue vs. St. Luke's Medical Center, IncKim GuevarraNo ratings yet

- 02 CIR v. CFI de CebuDocument2 pages02 CIR v. CFI de CebuFrances Angelica Domini KoNo ratings yet

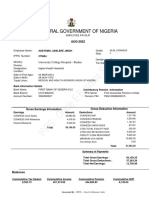

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaHalleluyah HalleluyahNo ratings yet

- ANPC vs. BIRDocument2 pagesANPC vs. BIRAnneNo ratings yet

- CIR vs. Club FilipinoDocument1 pageCIR vs. Club FilipinoJay-ar Rivera BadulisNo ratings yet

- Commissioner of Internal Revenue vs. ST Luke's Medical CenterDocument14 pagesCommissioner of Internal Revenue vs. ST Luke's Medical CenterRaquel DoqueniaNo ratings yet

- Corpo Outline 3 2Document183 pagesCorpo Outline 3 2Edmart VicedoNo ratings yet

- IRS-BIR On NGO'sDocument5 pagesIRS-BIR On NGO'sgaryNo ratings yet

- Rolling Rock Club v. United States, 785 F.2d 93, 3rd Cir. (1986)Document12 pagesRolling Rock Club v. United States, 785 F.2d 93, 3rd Cir. (1986)Scribd Government DocsNo ratings yet

- Cir vs. Club Filipino, (Corp)Document3 pagesCir vs. Club Filipino, (Corp)patrickenaje23No ratings yet

- Collector Vs Club Filipino de CebuDocument3 pagesCollector Vs Club Filipino de CebuRachel CayangaoNo ratings yet

- 05-CIR Vs The Club Filipino IncDocument3 pages05-CIR Vs The Club Filipino IncthelawanditscomplexitiesNo ratings yet

- CIR V Club FilipinoDocument3 pagesCIR V Club FilipinoParis LisonNo ratings yet

- CIR v. Club Filipino Inc. de Cebu, 1962Document3 pagesCIR v. Club Filipino Inc. de Cebu, 1962Randy SiosonNo ratings yet

- Digest CIR Vs Club FilipinoDocument5 pagesDigest CIR Vs Club FilipinoKenneth Ray AgustinNo ratings yet

- CIR Vs The Club FIlipinoDocument2 pagesCIR Vs The Club FIlipinoKaryl Ann Aquino-CaluyaNo ratings yet

- Restaurant Was A Necessary Incident To The Operation of The Club and Its Golf-CourseDocument2 pagesRestaurant Was A Necessary Incident To The Operation of The Club and Its Golf-Coursewmovies18No ratings yet

- Social Welfare What Does It MeanDocument39 pagesSocial Welfare What Does It MeanjamesNo ratings yet

- Pittsburgh Press Club v. United States, 536 F.2d 572, 3rd Cir. (1976)Document7 pagesPittsburgh Press Club v. United States, 536 F.2d 572, 3rd Cir. (1976)Scribd Government DocsNo ratings yet

- Commissioner of Internal Revenue vs. ST Luke's Medical CenterDocument5 pagesCommissioner of Internal Revenue vs. ST Luke's Medical CenterMarie CecileNo ratings yet

- 09 CirDocument4 pages09 CirjorementillaNo ratings yet

- Collector of Internal Revenue vs. Club Filipino, Inc. de CebuDocument4 pagesCollector of Internal Revenue vs. Club Filipino, Inc. de CebuPau SaulNo ratings yet

- CORP Full CASES 3Document137 pagesCORP Full CASES 3Mae de DiosNo ratings yet

- Collector Vs Club Filipino de CebuDocument2 pagesCollector Vs Club Filipino de CebuRoselito MaligroNo ratings yet

- Rochester Liederkranz, Inc. v. United States, 456 F.2d 152, 2d Cir. (1972)Document9 pagesRochester Liederkranz, Inc. v. United States, 456 F.2d 152, 2d Cir. (1972)Scribd Government DocsNo ratings yet

- COBLAW K50 Malit CaseInfoDocument2 pagesCOBLAW K50 Malit CaseInfoIversonNo ratings yet

- The Collector of Internal Revenue, Petitioner, vs. The CLUB FILIPINO, INC. DE CEBU, RespondentDocument5 pagesThe Collector of Internal Revenue, Petitioner, vs. The CLUB FILIPINO, INC. DE CEBU, RespondentSamNo ratings yet

- The Brook, Inc. v. Commissioner of Internal Revenue, 799 F.2d 833, 2d Cir. (1986)Document13 pagesThe Brook, Inc. v. Commissioner of Internal Revenue, 799 F.2d 833, 2d Cir. (1986)Scribd Government DocsNo ratings yet

- Corp Sept 14 Print!Document27 pagesCorp Sept 14 Print!Rina TruNo ratings yet

- Corpo Sep 14Document34 pagesCorpo Sep 14Ýel ÄcedilloNo ratings yet

- G.R. No. L-12719 May 31, 1962 The Collector of Internal Revenue, Petitioner, The Club Filipino, Inc. de Cebu, RespondentDocument73 pagesG.R. No. L-12719 May 31, 1962 The Collector of Internal Revenue, Petitioner, The Club Filipino, Inc. de Cebu, RespondentBianca Margaret TolentinoNo ratings yet

- Casus Omissus Pro Omisso Habendus Est - A Person, Object, or Thing Omitted FromDocument3 pagesCasus Omissus Pro Omisso Habendus Est - A Person, Object, or Thing Omitted FromCP LugoNo ratings yet

- Agenda 11 (Viii) - Section 7 of CGSTDocument5 pagesAgenda 11 (Viii) - Section 7 of CGSTADAYSA HOTANo ratings yet

- Tax 6-14Document36 pagesTax 6-14mjpjoreNo ratings yet

- Lobbying Regulations On Nonprofit OrganizationsDocument16 pagesLobbying Regulations On Nonprofit OrganizationsValerie F. Leonard100% (1)

- The County Trust Company of New YorkDocument54 pagesThe County Trust Company of New YorkAmberChanNo ratings yet

- Case # 160 Collector of Internal Revenue v. Club Filipino, G.R. No. L-12719, 5 SCRA 321, May 31, 1962Document3 pagesCase # 160 Collector of Internal Revenue v. Club Filipino, G.R. No. L-12719, 5 SCRA 321, May 31, 1962Je S BeNo ratings yet

- Ocean Pines Ass'n, Inc. v. Cir, 672 F.3d 284, 4th Cir. (2012)Document13 pagesOcean Pines Ass'n, Inc. v. Cir, 672 F.3d 284, 4th Cir. (2012)Scribd Government DocsNo ratings yet

- Assessment of Charitable Trust and InstitutionDocument52 pagesAssessment of Charitable Trust and InstitutionAnonymous JJhHAdY5HzNo ratings yet

- A Look Into The NFL As NPO - Kris WilliamsDocument18 pagesA Look Into The NFL As NPO - Kris WilliamsKris WilliamsNo ratings yet

- TaxationDocument6 pagesTaxationNoel IV T. Borromeo0% (1)

- Solicitor General For Petitioner. V .Jaime & L. E. Petilla For RespondentDocument152 pagesSolicitor General For Petitioner. V .Jaime & L. E. Petilla For RespondentairarowenaNo ratings yet

- Collector Vs Club FilipinoDocument2 pagesCollector Vs Club FilipinoRaymart SalamidaNo ratings yet

- IRC 501 C 4 OrganizationsDocument40 pagesIRC 501 C 4 OrganizationsjamesNo ratings yet

- CIR Vs ST LukesDocument4 pagesCIR Vs ST LukesJohn Dexter FuentesNo ratings yet

- Computation of Income TaxDocument6 pagesComputation of Income TaxshakiraNo ratings yet

- Sample Format For Club Bylaws: Soroptimist International of (Insert Name of Club)Document4 pagesSample Format For Club Bylaws: Soroptimist International of (Insert Name of Club)Dyeriko KinzonNo ratings yet

- Exempt Organizations Technical Guide: TG 3-20 Introduction To Private Foundations & Special Rules IRC 508Document16 pagesExempt Organizations Technical Guide: TG 3-20 Introduction To Private Foundations & Special Rules IRC 508bwarner6986No ratings yet

- BylawsDocument10 pagesBylawsRitesh AgarwalNo ratings yet

- Heat Capacity and Other Thermodynamic Properties of Linear Macromolecules. VIII. Polyesters and PolyamidesDocument25 pagesHeat Capacity and Other Thermodynamic Properties of Linear Macromolecules. VIII. Polyesters and PolyamidesRitesh AgarwalNo ratings yet

- Thermodynamic Properties of Polyethylene: R. M. C. PetreeDocument10 pagesThermodynamic Properties of Polyethylene: R. M. C. PetreeRitesh AgarwalNo ratings yet

- ECN Calculation PaperDocument4 pagesECN Calculation PaperRitesh AgarwalNo ratings yet

- Study of The PP Pyrolysis KineticsDocument1 pageStudy of The PP Pyrolysis KineticsRitesh AgarwalNo ratings yet

- Marcilla 2003 - Page 1 PDFDocument1 pageMarcilla 2003 - Page 1 PDFRitesh AgarwalNo ratings yet

- Msedcl Payment April 2018Document1 pageMsedcl Payment April 2018Ritesh AgarwalNo ratings yet

- Assignment Questions - Suggested Answers (E1-9, E1-11, P1-1, P1-2)Document4 pagesAssignment Questions - Suggested Answers (E1-9, E1-11, P1-1, P1-2)Ivy KwokNo ratings yet

- Testkingpdf: Valid Test Online & Stable Pass King & Latest PDF DumpsDocument19 pagesTestkingpdf: Valid Test Online & Stable Pass King & Latest PDF DumpsRamkrishana PathakNo ratings yet

- Tally Era Conti...Document5 pagesTally Era Conti...Olivia OwenNo ratings yet

- Business Finance Lesson 2 1Document36 pagesBusiness Finance Lesson 2 1Alldren Manalo GunoNo ratings yet

- This Study Resource Was: Universiti Teknologi Mara Common Test 1 Answer SchemeDocument4 pagesThis Study Resource Was: Universiti Teknologi Mara Common Test 1 Answer SchemeSyazryna AzlanNo ratings yet

- 3A. Capital Structure Leverages Numerical MarkedDocument3 pages3A. Capital Structure Leverages Numerical MarkedSundeep MogantiNo ratings yet

- Personal Details Form - SOPDocument4 pagesPersonal Details Form - SOPVirat GadhviNo ratings yet

- City College of Calamba Department of Business Education Bs Accountancy Bridge Program For Non Abm StudentsDocument18 pagesCity College of Calamba Department of Business Education Bs Accountancy Bridge Program For Non Abm StudentsMerdwindelle AllagonesNo ratings yet

- Salary Slip: Employee Name: Month Designation: Year OrganisationDocument3 pagesSalary Slip: Employee Name: Month Designation: Year Organisationshakti.iyyappanNo ratings yet

- STEEL AUTHORITY OF INDIA LI AutoRecoveredDocument58 pagesSTEEL AUTHORITY OF INDIA LI AutoRecoveredShambhavi SinhaNo ratings yet

- Impact Incidence ShiftingDocument2 pagesImpact Incidence ShiftingRuhul AminNo ratings yet

- MenahilDocument4 pagesMenahilsaudoryxNo ratings yet

- 6.1 Class Work Question On PGBPDocument5 pages6.1 Class Work Question On PGBPRakNo ratings yet

- The NinnyDocument2 pagesThe NinnyrafookaziNo ratings yet

- ICAEW Principles of Taxation CH 1-4Document34 pagesICAEW Principles of Taxation CH 1-4ITALIANO hohNo ratings yet

- Pfm15e Im Ch11Document40 pagesPfm15e Im Ch11vdav hadhNo ratings yet

- Taxation in IndiaDocument8 pagesTaxation in Indiajasim ansariNo ratings yet

- 4 - BF - For STUDENTSDocument47 pages4 - BF - For STUDENTSPhill SamonteNo ratings yet

- Stock Valuation QuestionsDocument3 pagesStock Valuation QuestionsperiNo ratings yet

- Summary of Thailand-Tax-Guide and LawsDocument34 pagesSummary of Thailand-Tax-Guide and LawsPranav BhatNo ratings yet

- The Case Against TippingDocument29 pagesThe Case Against TippingYm MNo ratings yet

- Ratio Analysis Project ReportDocument80 pagesRatio Analysis Project Reportpriya,eNo ratings yet

- Pub 505 - Estimated Tax (2002)Document49 pagesPub 505 - Estimated Tax (2002)andrewh3No ratings yet