You might also like

- Chapter 1 - Money, Credit, and BankingDocument34 pagesChapter 1 - Money, Credit, and BankingLhara Senioritha95% (20)

- Unit Three Money - Forms and FunctionsDocument6 pagesUnit Three Money - Forms and FunctionsMihai TudorNo ratings yet

- Hegel - Fragment On LoveDocument4 pagesHegel - Fragment On LoveGiulia OskianNo ratings yet

- SWRB Social Work Practice Competencies 2Document3 pagesSWRB Social Work Practice Competencies 2api-291442969No ratings yet

- Finance MIDTERMDocument2 pagesFinance MIDTERMPia SolNo ratings yet

- Business Logic ReviewerDocument3 pagesBusiness Logic ReviewerMarian TorreonNo ratings yet

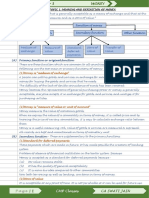

- Functions and Characteristics of Money: Lesson DescriptionDocument9 pagesFunctions and Characteristics of Money: Lesson DescriptionJinky TolentinoNo ratings yet

- 1.1 Basic Finance - 021407Document3 pages1.1 Basic Finance - 021407Angel RamosNo ratings yet

- MonetaryDocument5 pagesMonetaryJOHN ALDRICH CABIGNo ratings yet

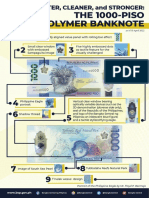

- 1000-Piso Polymer Banknote - Information SheetDocument2 pages1000-Piso Polymer Banknote - Information SheetDiogenes ZurbitoNo ratings yet

- Chapter 14Document4 pagesChapter 14Dao Quynh VyNo ratings yet

- Security Features PhilipinesDocument2 pagesSecurity Features PhilipinescucmungnammoiNo ratings yet

- BafinnnnDocument4 pagesBafinnnnkdot03433No ratings yet

- Basicfinance Module1 AnswersDocument6 pagesBasicfinance Module1 AnswersKryzal GansowenNo ratings yet

- Fake VS GenDocument18 pagesFake VS GenStephanie De La CruzNo ratings yet

- Chapter 1 - Introduction To MoneyDocument9 pagesChapter 1 - Introduction To MoneyThị Hiền Nhi HoàngNo ratings yet

- BESR Reviewer ABM 12Document11 pagesBESR Reviewer ABM 12Krisselyn ReigneNo ratings yet

- Vocabulary List 11Document1 pageVocabulary List 11maribuendiaayalaNo ratings yet

- Parcial L Ingles Tecnico UBPDocument6 pagesParcial L Ingles Tecnico UBPGiovannaNo ratings yet

- FM 305 Reviewer KunoDocument5 pagesFM 305 Reviewer KunoLei JardinNo ratings yet

- Bafin Chap 1Document2 pagesBafin Chap 1Philip DizonNo ratings yet

- QDEDocument19 pagesQDEJustine yuNo ratings yet

- Macroeconomic Analysis I Topic 6: The Asset Market, Money and Prices (Abel, Bernanke & Croushore: Chapter 7)Document40 pagesMacroeconomic Analysis I Topic 6: The Asset Market, Money and Prices (Abel, Bernanke & Croushore: Chapter 7)Enigmatic ElstonNo ratings yet

- UntitledDocument6 pagesUntitledBaavani KNo ratings yet

- QD Lecture PDFDocument15 pagesQD Lecture PDFArgie DionioNo ratings yet

- Comparison of Security Features of Pakistani Currency Notes With The Major CurrenciesDocument21 pagesComparison of Security Features of Pakistani Currency Notes With The Major CurrenciesHunain JawedNo ratings yet

- Money PDFDocument26 pagesMoney PDFDevaang ShuklaNo ratings yet

- Type of SD Levels: Extremes (Valleys and Peaks) Versus Continuation Patterns (CP)Document3 pagesType of SD Levels: Extremes (Valleys and Peaks) Versus Continuation Patterns (CP)CharisNo ratings yet

- Unit - Money & BankingDocument14 pagesUnit - Money & BankingLakshita JangidNo ratings yet

- Group4 - Financial MarketsDocument61 pagesGroup4 - Financial MarketsMarie Pearl NarioNo ratings yet

- Comprensión Lectora Parcial 1Document4 pagesComprensión Lectora Parcial 1charli1guevaraNo ratings yet

- BankingDocument44 pagesBankingAdwaith c AnandNo ratings yet

- Business FinanceDocument10 pagesBusiness FinanceMike Reyes (XxMKExX)No ratings yet

- Module 5 FINE 6Document3 pagesModule 5 FINE 6Villasante Rell JohnNo ratings yet

- Characteristics and Functions of MoneyDocument2 pagesCharacteristics and Functions of MoneyAndroid HelpNo ratings yet

- Module 1Document4 pagesModule 1Julia VinoyaNo ratings yet

- 1lmd - Test 01 - Money - 2nd VersionDocument6 pages1lmd - Test 01 - Money - 2nd Versionimen DEBBANo ratings yet

- Accbp 100 ReviewerDocument3 pagesAccbp 100 ReviewerKissey EstrellaNo ratings yet

- Counterfeiting IdentificationDocument5 pagesCounterfeiting IdentificationMark Angelo Soriano BauiNo ratings yet

- FINANCIAL MARKETS REVIEWER. CH 3&4docxDocument29 pagesFINANCIAL MARKETS REVIEWER. CH 3&4docxChristine RepuldaNo ratings yet

- Financial MarketsDocument8 pagesFinancial MarketsMarianne AguilarNo ratings yet

- Four Functions of MoneyDocument5 pagesFour Functions of MoneyLucela InocNo ratings yet

- Reviewer in Financial MarketDocument10 pagesReviewer in Financial MarketJhonalyn MaraonNo ratings yet

- Money and Financial Markets Unit 1Document32 pagesMoney and Financial Markets Unit 1Teddy Jain100% (1)

- Mod 3 & 4 (Markfin)Document7 pagesMod 3 & 4 (Markfin)Alessandra AcuzarNo ratings yet

- Forms: 3.1 Money and Its Importance DefinitionDocument26 pagesForms: 3.1 Money and Its Importance DefinitionBereket MekonnenNo ratings yet

- MoneyDocument8 pagesMoneyFOR AKKNo ratings yet

- Money ReviewerDocument5 pagesMoney ReviewerCalago, James Carlo V.No ratings yet

- Fake Currency Detection Using Image ProcessingDocument4 pagesFake Currency Detection Using Image ProcessingInformatika Universitas Malikussaleh100% (1)

- Know Your CDN Polymer NotesDocument1 pageKnow Your CDN Polymer NotesPrince DhillonNo ratings yet

- Finmar Finals 2021Document45 pagesFinmar Finals 2021Nune SabanalNo ratings yet

- Lecture 6 The Monetary SystemDocument8 pagesLecture 6 The Monetary SystemHiền NguyễnNo ratings yet

- 121 - Notes Q3Document8 pages121 - Notes Q3Tricia KiethNo ratings yet

- Functions of Money - Macro Extra Notes.Document2 pagesFunctions of Money - Macro Extra Notes.SONY GLANCY D SILVANo ratings yet

- Money and Banking: Name - Ayushi Class - 12 Section - C Subject - EconomicsDocument13 pagesMoney and Banking: Name - Ayushi Class - 12 Section - C Subject - EconomicsMitali MishraNo ratings yet

- E BookDocument21 pagesE BookNatsuyuki HanaNo ratings yet

- Investments - Background and Issues: Financial Versus Real AssetsDocument5 pagesInvestments - Background and Issues: Financial Versus Real AssetsLex Acads100% (1)

- BusFin-2nd SemDocument8 pagesBusFin-2nd SemMARCK JULLIAN ALFONSONo ratings yet

- Topic 3: Money: Objective 1: Define The Term MoneyDocument1 pageTopic 3: Money: Objective 1: Define The Term Moneymarcia.jacobNo ratings yet

- Topic 3: Money: Objective 1: Define The Term MoneyDocument1 pageTopic 3: Money: Objective 1: Define The Term Moneymarcia.jacobNo ratings yet

- Financial MarketsDocument3 pagesFinancial MarketsMohammad Raffe GuroNo ratings yet

- Biodefense 2012 FinalProgramDocument116 pagesBiodefense 2012 FinalProgramniogarzNo ratings yet

- Database Management SystemDocument284 pagesDatabase Management Systemavinash pandeyNo ratings yet

- 20 Terms and Conditions of LoveDocument3 pages20 Terms and Conditions of LovedasariramakiranNo ratings yet

- A Letter To Satyamev JayateDocument3 pagesA Letter To Satyamev JayateBharat SharmaNo ratings yet

- Artículo - Assessment of Vitamin D Status - A Changing LandscapeDocument24 pagesArtículo - Assessment of Vitamin D Status - A Changing LandscapePaoloNo ratings yet

- Banana Island ResortDocument20 pagesBanana Island Resortthugnature0% (2)

- Program 1772284084 BFa8FfXGC1Document8 pagesProgram 1772284084 BFa8FfXGC1Danitza1459No ratings yet

- The Spotted CowDocument7 pagesThe Spotted CowFrecelyn AbluyanNo ratings yet

- Lyn Capili LP Final DemoDocument4 pagesLyn Capili LP Final Demoapi-556696781No ratings yet

- Human Body Temperature Measurement ListDocument2 pagesHuman Body Temperature Measurement ListproNo ratings yet

- Technical Service Information: Chrysler Diagnostic CodesDocument6 pagesTechnical Service Information: Chrysler Diagnostic CodesMario MastronardiNo ratings yet

- Laboratory 5 - The Convolution IntegralDocument10 pagesLaboratory 5 - The Convolution IntegralOsama AlqahtaniNo ratings yet

- Case Paper On Child DevelopmentDocument8 pagesCase Paper On Child Developmentapi-248983324No ratings yet

- Km31401 Makmal IV AcDocument3 pagesKm31401 Makmal IV AcChee OnnNo ratings yet

- ISO 9001 Applied As A Healthcare Quality Management ToolDocument1 pageISO 9001 Applied As A Healthcare Quality Management ToolonatbrossNo ratings yet

- Statistics For Business and Economics: Hypothesis Testing IIDocument48 pagesStatistics For Business and Economics: Hypothesis Testing IIfour threepioNo ratings yet

- Intelligent Agent: Dept. of Computer Science Faculty of Science and TechnologyDocument40 pagesIntelligent Agent: Dept. of Computer Science Faculty of Science and TechnologyJobayer HayderNo ratings yet

- Project Procedure IMP 16Document22 pagesProject Procedure IMP 16Jose R C FernandesNo ratings yet

- Chapter3-5 Mechanical SensorsDocument79 pagesChapter3-5 Mechanical SensorsNguyễn Thanh Tuấn KiệtNo ratings yet

- SAP MM - Source Determination/ListDocument7 pagesSAP MM - Source Determination/ListSathya SatzNo ratings yet

- Shell Spirax S4 Atf HDX: Performance, Features & Benefits Specifications, Approvals & RecommendationsDocument2 pagesShell Spirax S4 Atf HDX: Performance, Features & Benefits Specifications, Approvals & RecommendationsKieran MañalacNo ratings yet

- Pelling Ormal: Mia TijamDocument15 pagesPelling Ormal: Mia TijamJess VergaraNo ratings yet

- Cointegration or Spurious Regression - Stata BlogDocument7 pagesCointegration or Spurious Regression - Stata Blogdkoers_beginNo ratings yet

- Agust 2020Document29 pagesAgust 2020Danny YanuarNo ratings yet

- Drug Calculations Ratio and Proportion Problems For Clinical Practice 9th Edition Brown Test BankDocument18 pagesDrug Calculations Ratio and Proportion Problems For Clinical Practice 9th Edition Brown Test Bankkarenyoungsbpmkaxioz100% (14)

- Final Manuscript For Thesis Proposal (1st Revision) - MineralesDocument70 pagesFinal Manuscript For Thesis Proposal (1st Revision) - MineralesMae Anne ESPANOLANo ratings yet

- 2022 - 1st Round UEUS Key FindingsDocument17 pages2022 - 1st Round UEUS Key FindingsEyobNo ratings yet

- 1.0 Overview of The Current State of TechnologyDocument4 pages1.0 Overview of The Current State of TechnologyNordz MamentingNo ratings yet