You might also like

- R05 Time Value of Money IFT Notes PDFDocument28 pagesR05 Time Value of Money IFT Notes PDFAbbas0% (1)

- MTM 508: Financial Management: Session 1: Time Value of Money (TVM)Document6 pagesMTM 508: Financial Management: Session 1: Time Value of Money (TVM)Chelsea BustamanteNo ratings yet

- Sample/practice Exam 5 April Year, Questions and Answers: Company Law For Business (Curtin University)Document24 pagesSample/practice Exam 5 April Year, Questions and Answers: Company Law For Business (Curtin University)milk teaNo ratings yet

- Medical Research Corporation Is Expanding Its Research and Production CapacityDocument1 pageMedical Research Corporation Is Expanding Its Research and Production CapacityAmit PandeyNo ratings yet

- Time Value of Money: Lesson 5.1Document24 pagesTime Value of Money: Lesson 5.1Tin CabosNo ratings yet

- Ross FCF 11ce IM Ch05Document10 pagesRoss FCF 11ce IM Ch05Jeffrey O'LearyNo ratings yet

- Chapter 2 Time Value of MoneyDocument47 pagesChapter 2 Time Value of Moneymarketing bbs 2nd year pdfNo ratings yet

- File To Mail - Session 1Document5 pagesFile To Mail - Session 1Elisten DabreoNo ratings yet

- The Time Value of Money: Section 5.1Document5 pagesThe Time Value of Money: Section 5.1Mary DenizeNo ratings yet

- Fin440 Chapter 5Document29 pagesFin440 Chapter 5sajedulNo ratings yet

- Unit 2 Tutorials Time Value of Money and Financial SecuritiesDocument84 pagesUnit 2 Tutorials Time Value of Money and Financial SecuritiesAldrin Kevin TamseNo ratings yet

- Tvom 1Document82 pagesTvom 1Jennifer KhoNo ratings yet

- Time Value of MoneyDocument50 pagesTime Value of MoneyKarthik ShanklaNo ratings yet

- FIN2004 - 2704 Week 3Document84 pagesFIN2004 - 2704 Week 3ZenyuiNo ratings yet

- Time Value of MoneyDocument19 pagesTime Value of MoneyQueens CarinoNo ratings yet

- Corporate Finance 1St Edition Booth Solutions Manual Full Chapter PDFDocument36 pagesCorporate Finance 1St Edition Booth Solutions Manual Full Chapter PDFvernon.amundson153100% (11)

- Corporate Finance 1st Edition Booth Solutions Manual 1Document19 pagesCorporate Finance 1st Edition Booth Solutions Manual 1james100% (35)

- Fundamentals of Corporate Finance 3rd Edition Parrino Solutions Manual 1Document36 pagesFundamentals of Corporate Finance 3rd Edition Parrino Solutions Manual 1michaelhooverspnjdgactf100% (22)

- Lecture 4Document89 pagesLecture 4Lee Li HengNo ratings yet

- Unit 3 (a) : Time Value Of Money 1: Analyzing Single Cash Flows 货币时间价值 1 :分析单一现金流 - Chapter 4Document72 pagesUnit 3 (a) : Time Value Of Money 1: Analyzing Single Cash Flows 货币时间价值 1 :分析单一现金流 - Chapter 4KaMan CHAUNo ratings yet

- Foundations of Finance: The Time Value of MoneyDocument75 pagesFoundations of Finance: The Time Value of MoneyMaya HusniatiNo ratings yet

- CH4 - FM - For StudentsDocument45 pagesCH4 - FM - For Studentsjajo200110No ratings yet

- Time Value of Money Chapter 5Document78 pagesTime Value of Money Chapter 5herculesNo ratings yet

- Chapter 6 - Time Value of MoneyDocument7 pagesChapter 6 - Time Value of MoneyJean EliaNo ratings yet

- Time Value of Money: All Rights ReservedDocument55 pagesTime Value of Money: All Rights Reservedjaz hoodNo ratings yet

- Time Value of MoneyDocument79 pagesTime Value of MoneyAsistio, Karl Lawrence B.No ratings yet

- Importance of Time Value of Money in Financial ManagementDocument16 pagesImportance of Time Value of Money in Financial Managementtanmayjoshi969315No ratings yet

- Fin254 Ch05 NNH TVM UpdatedDocument80 pagesFin254 Ch05 NNH TVM Updatedamir khanNo ratings yet

- Banking Foundation Course v2.1Document178 pagesBanking Foundation Course v2.1Soumen MitraNo ratings yet

- TVMDocument38 pagesTVMbenjamin.labayenNo ratings yet

- Time Value of MoneyDocument9 pagesTime Value of Moneykedir MekonnenNo ratings yet

- Chapter 4Document50 pagesChapter 422GayeonNo ratings yet

- Introduction To Corporate Finance 4th Edition Booth Test Bank DownloadDocument36 pagesIntroduction To Corporate Finance 4th Edition Booth Test Bank DownloadJudy Snell100% (21)

- Time Value of MoneyDocument22 pagesTime Value of MoneyNaufal Farras MNo ratings yet

- Chapter 2Document35 pagesChapter 2TarekegnBelayNo ratings yet

- Time Value of Money: All Rights ReservedDocument79 pagesTime Value of Money: All Rights ReservedBilal SahuNo ratings yet

- Time Value of Money: All Rights ReservedDocument94 pagesTime Value of Money: All Rights Reservedjcgaide3No ratings yet

- Learning Packet 5 Time Value of MoneyDocument10 pagesLearning Packet 5 Time Value of MoneyPrincess Marie BaldoNo ratings yet

- Preliminary Knowledge On Insurance PricingDocument8 pagesPreliminary Knowledge On Insurance PricinggdobrinichNo ratings yet

- EMSE 260 Clhapter 4 Time Value of MoneyDocument59 pagesEMSE 260 Clhapter 4 Time Value of Moneytgonzalez2072No ratings yet

- Fin 254 - Chapter 5 CorrectedDocument61 pagesFin 254 - Chapter 5 CorrectedsajedulNo ratings yet

- Time Value of MoneyDocument69 pagesTime Value of MoneyAhasan HabibNo ratings yet

- Mata Kuliah: Manajemen Keuangan 1 Kode Mata Kuliah/Sks: Mn5003 / 3 Sks Kurikulum: 2012 Versi: 0.1Document52 pagesMata Kuliah: Manajemen Keuangan 1 Kode Mata Kuliah/Sks: Mn5003 / 3 Sks Kurikulum: 2012 Versi: 0.1Faishal Alghi FariNo ratings yet

- Unit 3 (a) : Time Value Of Money 1: Analyzing Single Cash Flows 货币时间价值1:分析单一现金流 - Chapter 4Document72 pagesUnit 3 (a) : Time Value Of Money 1: Analyzing Single Cash Flows 货币时间价值1:分析单一现金流 - Chapter 4KaMan CHAUNo ratings yet

- Parrino 2e PowerPoint Review Ch05Document42 pagesParrino 2e PowerPoint Review Ch05Khadija AlkebsiNo ratings yet

- Financial Management Time Value of MoneyDocument13 pagesFinancial Management Time Value of MoneyNoelia Mc DonaldNo ratings yet

- Chap 5Document31 pagesChap 5ahmad altoufailyNo ratings yet

- Mod-2 TIME - VALUE - OF - MONEYDocument80 pagesMod-2 TIME - VALUE - OF - MONEYamrj27609No ratings yet

- Chapter-03-Time Value of Money-IsmatDocument74 pagesChapter-03-Time Value of Money-Ismatamzadrony7No ratings yet

- 30 TVM 1 PPDocument34 pages30 TVM 1 PPAlbertoNo ratings yet

- Chapter 3 Time Value of MoneyDocument80 pagesChapter 3 Time Value of MoneyMary Nica BarceloNo ratings yet

- CCFC 511 - Chapter 3 (Present Value)Document22 pagesCCFC 511 - Chapter 3 (Present Value)michi.berto.2020No ratings yet

- Time Value of MoneyDocument12 pagesTime Value of MoneyMuhammad Saad IqbalNo ratings yet

- Introduction To Valuation: The Time Value of Money: Rights Reserved Mcgraw-Hill/IrwinDocument12 pagesIntroduction To Valuation: The Time Value of Money: Rights Reserved Mcgraw-Hill/IrwinYasser MaamounNo ratings yet

- Introduction To Business Finance (Fin201) : Time Value of MoneyDocument55 pagesIntroduction To Business Finance (Fin201) : Time Value of MoneyAhsan KamranNo ratings yet

- 2023 EBAD401 - Chapter 5 PPT LecturerDocument36 pages2023 EBAD401 - Chapter 5 PPT Lecturermaresa bruinersNo ratings yet

- Effective Annual Interest Rate: Lesson 5.2Document15 pagesEffective Annual Interest Rate: Lesson 5.2Just TinNo ratings yet

- Time Value of MoneyDocument40 pagesTime Value of MoneyAhmedmughalNo ratings yet

- Topic 4 Valuation of Future Cashflows - Time Value For MoneyDocument39 pagesTopic 4 Valuation of Future Cashflows - Time Value For MoneyQianyiiNo ratings yet

- DHA-BHI-404 - Unit4 - Time Value of MoneyDocument17 pagesDHA-BHI-404 - Unit4 - Time Value of MoneyFë LïçïäNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Futures and Options Final TestDocument15 pagesFutures and Options Final TestCarolina SáNo ratings yet

- Bootstrapping Definition - InvestopediaDocument3 pagesBootstrapping Definition - InvestopediaBob KaneNo ratings yet

- BodieDocument7 pagesBodiepinoNo ratings yet

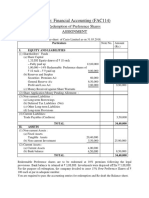

- Preference Shares AssignmentDocument4 pagesPreference Shares AssignmentDhairya ShahNo ratings yet

- UTS AKL 2 - Resky Awaliah (A031181004)Document3 pagesUTS AKL 2 - Resky Awaliah (A031181004)Resky AwaliahNo ratings yet

- Peso Emperor Fund - Fund Fact Sheet - October - 2020Document2 pagesPeso Emperor Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNo ratings yet

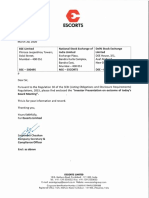

- Escort PDFDocument13 pagesEscort PDFKripashankar MauryaNo ratings yet

- Jenga Inc Solution: Strictly ConfidentialDocument3 pagesJenga Inc Solution: Strictly Confidentialanjali shilpa kajal100% (1)

- Risk and Returns Consideration in Portfolio Management and Investments in IiflDocument65 pagesRisk and Returns Consideration in Portfolio Management and Investments in IiflADITYA PANDEYNo ratings yet

- Tenants in Common 1031 ExchangeDocument2 pagesTenants in Common 1031 ExchangeRayNo ratings yet

- Target Market Determination: October 2021Document5 pagesTarget Market Determination: October 2021leNo ratings yet

- P Iail PDFDocument323 pagesP Iail PDFAFC Capital LimitedNo ratings yet

- Questions For Solving Case Study of Anandam MFG CoDocument3 pagesQuestions For Solving Case Study of Anandam MFG CoSubodh Sahastrabuddhe100% (1)

- DSV Expansion To MalaysiaDocument38 pagesDSV Expansion To MalaysiaDavid IskanderNo ratings yet

- Offshore Banking Definition, Benefits & Offshore AccountDocument8 pagesOffshore Banking Definition, Benefits & Offshore AccountRoy Navarro VispoNo ratings yet

- Solution Ipa Week 9 Chapter 15Document38 pagesSolution Ipa Week 9 Chapter 15poppy seedNo ratings yet

- Funds Flow StatementDocument14 pagesFunds Flow StatementGurpreet SinghNo ratings yet

- A Study On Comparative Analysis of Mutual FundDocument87 pagesA Study On Comparative Analysis of Mutual FundAkhil KesharwaniNo ratings yet

- GR12 Business Finance Module 1-2Document7 pagesGR12 Business Finance Module 1-2Jean Diane JoveloNo ratings yet

- CS PFG Asia Market Overview Presentation - February 2021Document24 pagesCS PFG Asia Market Overview Presentation - February 2021Rishika RankaNo ratings yet

- Team 4 - (Case Study 5-1 and 5-3) Investment PropertyDocument47 pagesTeam 4 - (Case Study 5-1 and 5-3) Investment PropertyRahman PanjaitanNo ratings yet

- 2ii - Jakob ThomaeDocument15 pages2ii - Jakob ThomaeValerio ScaccoNo ratings yet

- JegiDocument5 pagesJegiAnonymous Feglbx5No ratings yet

- How Do People Spend Their Lottery WinningsDocument5 pagesHow Do People Spend Their Lottery WinningsmaloNo ratings yet

- RBC Canadian Small & Mid-Cap Resources Fund - Series FDocument3 pagesRBC Canadian Small & Mid-Cap Resources Fund - Series FNikal upNo ratings yet

- Gaia Iar 2020Document114 pagesGaia Iar 2020m_edas4262No ratings yet

- FM212 2018 PaperDocument5 pagesFM212 2018 PaperSam HanNo ratings yet

- IAS 36 Impairment of AssetsDocument45 pagesIAS 36 Impairment of AssetsvidiNo ratings yet