You might also like

- GE Money and BankingDocument110 pagesGE Money and BankingBabita DeviNo ratings yet

- A9Ry0p5e4 Eppe6w 830Document10 pagesA9Ry0p5e4 Eppe6w 830elisaNo ratings yet

- Temperature Scanner and Oximeter Bill of Amazon BillDocument1 pageTemperature Scanner and Oximeter Bill of Amazon BillR.S.No ratings yet

- Fundamental Factors That Affect Currency ValuesDocument3 pagesFundamental Factors That Affect Currency ValuesVishvesh SinghNo ratings yet

- Fundamental Analysis Black BookDocument50 pagesFundamental Analysis Black Bookwagha100% (1)

- Payment Message PDFDocument9 pagesPayment Message PDFPrachi SaxenaNo ratings yet

- Banking FinalsDocument15 pagesBanking FinalsApril CastilloNo ratings yet

- Vol-5 Introduction To Fundamental AnalysisDocument10 pagesVol-5 Introduction To Fundamental Analysisearregui0% (1)

- Fundamental Analysis of ICICI BankDocument79 pagesFundamental Analysis of ICICI BanksantumandalNo ratings yet

- Stock Fundamental Analysis Mastery: Unlocking Company Stock Financials for Profitable TradingFrom EverandStock Fundamental Analysis Mastery: Unlocking Company Stock Financials for Profitable TradingNo ratings yet

- Security Analysis and Portfolio ManagementDocument25 pagesSecurity Analysis and Portfolio ManagementKomal Shujaat0% (1)

- Unit-2 Security AnalysisDocument26 pagesUnit-2 Security AnalysisJoshua JacksonNo ratings yet

- Fundamentalanalysis 150227053710 Conversion Gate02Document46 pagesFundamentalanalysis 150227053710 Conversion Gate02Meera SeshannaNo ratings yet

- Analysis of Variable Income SecuritiesDocument11 pagesAnalysis of Variable Income SecuritiesManjula100% (3)

- Chapter 6 Security AnalysisDocument13 pagesChapter 6 Security Analysistame kibruNo ratings yet

- SAPM Unit-3Document31 pagesSAPM Unit-3Paluvayi SubbaraoNo ratings yet

- Investement Analysis and Portfolio Management Chapter 5Document15 pagesInvestement Analysis and Portfolio Management Chapter 5Oumer ShaffiNo ratings yet

- Mouni (Equity Analysis)Document22 pagesMouni (Equity Analysis)arjunmba119624No ratings yet

- Economy, Industry and Company Analysis - by S. KevinDocument9 pagesEconomy, Industry and Company Analysis - by S. KevinHaiderNo ratings yet

- Undamental Nalysis: Gayatri Mohanty Asst. Professor, Parul Institute of Management & ResearchDocument32 pagesUndamental Nalysis: Gayatri Mohanty Asst. Professor, Parul Institute of Management & Researchkunalacharya5No ratings yet

- Unit 2 - Fundamental Analysis AKTUDocument50 pagesUnit 2 - Fundamental Analysis AKTUharishNo ratings yet

- A Study On Fundamental Analysis of OngcDocument10 pagesA Study On Fundamental Analysis of OngcSaurav tiwariNo ratings yet

- A Study On Equity Analysis at India-InfolineDocument21 pagesA Study On Equity Analysis at India-Infolinearjunmba119624No ratings yet

- TP ImDocument21 pagesTP ImtazimNo ratings yet

- Meaning of Fundamental AnalysisDocument4 pagesMeaning of Fundamental AnalysisSadat ZafreeNo ratings yet

- Chapter 2 Fundamental AnalysisDocument7 pagesChapter 2 Fundamental AnalysisDivya GøwdaNo ratings yet

- Fundamental Analysis of Banking Industry: Interim Report ONDocument29 pagesFundamental Analysis of Banking Industry: Interim Report ONBalpreet KaurNo ratings yet

- Group 1 Equity Research ReportDocument45 pagesGroup 1 Equity Research ReportKuldip DixitNo ratings yet

- The Market: Why It Exists?Document57 pagesThe Market: Why It Exists?Nitish GuptaNo ratings yet

- Shri Guru Ram Rai University Lecture-1 Unit - 3 Principles of Investment POIN: 603Document4 pagesShri Guru Ram Rai University Lecture-1 Unit - 3 Principles of Investment POIN: 603shabnamNo ratings yet

- Assignment Day 3Document12 pagesAssignment Day 3Qazi MobeenNo ratings yet

- Saim 2Document13 pagesSaim 2sapnathakur4444No ratings yet

- Fundamental Analysis in SAPMDocument6 pagesFundamental Analysis in SAPMRoshan VargheseNo ratings yet

- Fundamentals of Banking A Project ReportDocument45 pagesFundamentals of Banking A Project Reportaftabshaikh04No ratings yet

- MF0010 Set1 Q1& 2Document5 pagesMF0010 Set1 Q1& 2s_konarNo ratings yet

- How To Analyze The Stock MarketDocument9 pagesHow To Analyze The Stock MarketantumanipadamNo ratings yet

- Ajibefun - A Guide To Trading With Fundamental AnalysisDocument21 pagesAjibefun - A Guide To Trading With Fundamental AnalysisBardly JonesNo ratings yet

- Quantitative Recession PredictionDocument10 pagesQuantitative Recession PredictionRd PatelNo ratings yet

- Kotak Securities - Fundamental Analysis Book 1 - IntroductionDocument8 pagesKotak Securities - Fundamental Analysis Book 1 - IntroductionRajesh Bellamkonda0% (1)

- Economic AnalysisDocument6 pagesEconomic Analysisabdulraqeeb alareqiNo ratings yet

- SAPM - Security AnalysisDocument7 pagesSAPM - Security AnalysisTyson Texeira100% (1)

- Unit 3Document43 pagesUnit 3ModitNo ratings yet

- Oneliners P5Document4 pagesOneliners P5Nirvana BoyNo ratings yet

- Fundamental AnalysisDocument7 pagesFundamental AnalysisAdarsh KumarNo ratings yet

- Master in Business Administration - Semester 3 MF0010 - Security Analysis and Portfolio Management - 4 Credits Assignment Set-1 (60 Marks)Document11 pagesMaster in Business Administration - Semester 3 MF0010 - Security Analysis and Portfolio Management - 4 Credits Assignment Set-1 (60 Marks)Sumit ChhuganiNo ratings yet

- Economic Significance of Index MovementsDocument10 pagesEconomic Significance of Index MovementsNILA ANo ratings yet

- Fundamental AnalysisDocument52 pagesFundamental AnalysisLisha lalwaniNo ratings yet

- Economic Analysis: Ashok Kumar RawaniDocument14 pagesEconomic Analysis: Ashok Kumar RawaniAman RajNo ratings yet

- Top-Down Valuation (EIC Analysis) : EconomyDocument5 pagesTop-Down Valuation (EIC Analysis) : EconomyManas MohapatraNo ratings yet

- Ashok Kumar Rawani: Department of Commerce Jamshedpur Co-Operative CollegeDocument14 pagesAshok Kumar Rawani: Department of Commerce Jamshedpur Co-Operative CollegeNorleen Rose S. AguilarNo ratings yet

- Fundamental Analysis and Stock Returns: An Indian Evidence: Full Length Research PaperDocument7 pagesFundamental Analysis and Stock Returns: An Indian Evidence: Full Length Research PaperMohana SundaramNo ratings yet

- Balaji NayakDocument24 pagesBalaji NayakMohmmed KhayyumNo ratings yet

- What Is Fundamental Analysis?Document3 pagesWhat Is Fundamental Analysis?MEGHANA DIGHENo ratings yet

- Chapter 1 - IntroductionDocument4 pagesChapter 1 - IntroductionShoaib KhattakNo ratings yet

- Portfolio Management CH 3Document11 pagesPortfolio Management CH 3Prakash KumarNo ratings yet

- SAPM Fundamental AnalysisDocument17 pagesSAPM Fundamental Analysisanjusawlani86100% (4)

- Project 1Document90 pagesProject 1Darshan NallodeNo ratings yet

- Fundamental Analysis of Icici Bank: School of Management Studies Punjabi University PatialaDocument21 pagesFundamental Analysis of Icici Bank: School of Management Studies Punjabi University Patialapuneet_kissNo ratings yet

- Fundamental Analysis: Economic AnalysisDocument12 pagesFundamental Analysis: Economic AnalysisluvnehaNo ratings yet

- Portfolio Management NotesDocument25 pagesPortfolio Management NotesRigved DarekarNo ratings yet

- Factors Affecting Stock PricesDocument4 pagesFactors Affecting Stock PricesSHIVANGI SINGH 21221043No ratings yet

- E-Note 16153 Content Document 20240226013550PMDocument36 pagesE-Note 16153 Content Document 20240226013550PMytmandar29No ratings yet

- E-Note 16272 Content Document 20240301112637AMDocument20 pagesE-Note 16272 Content Document 20240301112637AMytmandar29No ratings yet

- Presentation 16246 Content Document 20240229020643PMDocument73 pagesPresentation 16246 Content Document 20240229020643PMytmandar29No ratings yet

- E-Note 16259 Content Document 20240301122755AMDocument20 pagesE-Note 16259 Content Document 20240301122755AMytmandar29No ratings yet

- Personal Selling: Department of Management StudiesDocument16 pagesPersonal Selling: Department of Management Studiesytmandar29No ratings yet

- L&T PDFDocument26 pagesL&T PDFytmandar29No ratings yet

- Presentation 14791 Content Document 20240103101324AMDocument21 pagesPresentation 14791 Content Document 20240103101324AMytmandar29No ratings yet

- Maruti Suzuki India: Msil in Staged For A Strong ComebackDocument40 pagesMaruti Suzuki India: Msil in Staged For A Strong ComebackShArp ,No ratings yet

- Analysis of Textile Industry of PakistanDocument25 pagesAnalysis of Textile Industry of PakistanSumrah KhalidNo ratings yet

- Acct Statement - XX9050 - 28022022Document1 pageAcct Statement - XX9050 - 28022022Suman BasakNo ratings yet

- Energy Storage For A High Penetration of RenewablesDocument10 pagesEnergy Storage For A High Penetration of RenewablesRosalind CardenasNo ratings yet

- FINC521-Corporate Finance - Part1 PDFDocument3 pagesFINC521-Corporate Finance - Part1 PDFAjit Kumar100% (1)

- 'Pati Bet', Schumannianthus Dichotomus (Roxb.) Gagnep. - A Raw Material For Preparation of Livelihood Supporting HandicraftsDocument6 pages'Pati Bet', Schumannianthus Dichotomus (Roxb.) Gagnep. - A Raw Material For Preparation of Livelihood Supporting HandicraftsBengal TextileNo ratings yet

- Thesis Oil IndustryDocument8 pagesThesis Oil Industrybsgyhhnc100% (2)

- Alam Consciousness Centre UbudDocument28 pagesAlam Consciousness Centre UbudKomanoNo ratings yet

- Risk and Its Measurement - v.1Document3 pagesRisk and Its Measurement - v.1ashleysavetNo ratings yet

- Financial Instruments With Characteristics of Equity: Discussion PaperDocument34 pagesFinancial Instruments With Characteristics of Equity: Discussion PaperMohammedYousifSalihNo ratings yet

- LIST OF BANK ACCOUNTS CMS-IFSC Codes 130911 121111Document1 pageLIST OF BANK ACCOUNTS CMS-IFSC Codes 130911 121111anuragshangari6812No ratings yet

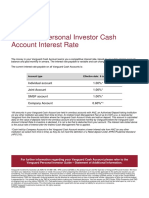

- AU-Vanguard Personal Investor-Cash Account Interest RateDocument1 pageAU-Vanguard Personal Investor-Cash Account Interest RateNick KNo ratings yet

- Application For Locational Clearance Form - 05-27-22Document1 pageApplication For Locational Clearance Form - 05-27-22Mariel Jane FuentiblancaNo ratings yet

- Financial Leverage and Performance of Nepalese Commercial BanksDocument23 pagesFinancial Leverage and Performance of Nepalese Commercial BanksPushpa Shree PandeyNo ratings yet

- NIFTY 500: 2019 2020 (Upto 16-04-2020)Document11 pagesNIFTY 500: 2019 2020 (Upto 16-04-2020)Power of Stock MarketNo ratings yet

- Answers For Chapter 19Document1 pageAnswers For Chapter 19Wan MP WilliamNo ratings yet

- SOP - A.01.01. Petty Cash AdvanceDocument14 pagesSOP - A.01.01. Petty Cash AdvanceVenesya Widya AuliaNo ratings yet

- Report On Smart Cities Development Project: By: Anurag Singh M.SC 4 Semester C - 402 PracticalDocument9 pagesReport On Smart Cities Development Project: By: Anurag Singh M.SC 4 Semester C - 402 PracticalAnurag SinghNo ratings yet

- Statistical Information On Nepalese Agriculture 2077 78Document274 pagesStatistical Information On Nepalese Agriculture 2077 78Kranti KariNo ratings yet

- IntroductionDocument23 pagesIntroductionSari MolisaNo ratings yet

- To Whom So Ever It May ConsernDocument1 pageTo Whom So Ever It May ConsernrajNo ratings yet

- Exam On CH 11fswfwrfDocument5 pagesExam On CH 11fswfwrfkareem abozeedNo ratings yet

- Sesi 2Document23 pagesSesi 2smpurnolietaniaNo ratings yet

- Chapter 5. Consumer BehaviourDocument21 pagesChapter 5. Consumer BehaviourEl rincón de las 5 EL RINCÓN DE LAS 5No ratings yet

- Finance Detective - Ratio AnalysisDocument2 pagesFinance Detective - Ratio AnalysisAndhitiawarman NugrahaNo ratings yet

- Bcom Part 1 Ae Business Economics B 138 2019Document2 pagesBcom Part 1 Ae Business Economics B 138 2019Narendra BandeNo ratings yet