You might also like

- Carrefour MarketDocument11 pagesCarrefour MarketMuhammad Ben Mahfouz Al-ZubairiNo ratings yet

- Edible Seaweed Market Analysis 1.17.20Document60 pagesEdible Seaweed Market Analysis 1.17.20NEWS CENTER MaineNo ratings yet

- Villa Green Investment PackageDocument51 pagesVilla Green Investment Packagegarry435No ratings yet

- SCB Strategic Review 2015 PDFDocument49 pagesSCB Strategic Review 2015 PDFamirentezamNo ratings yet

- Wyndham Vacation Ownership v0214Document43 pagesWyndham Vacation Ownership v0214LeesaChenNo ratings yet

- Investment Banking Investment Banking2122Document16 pagesInvestment Banking Investment Banking2122vishal13889100% (2)

- Tops and Bottoms ClassDocument67 pagesTops and Bottoms ClassHerbNo ratings yet

- Stem InvestorPresentation 2022 Sept VFDocument27 pagesStem InvestorPresentation 2022 Sept VFDE ReddyNo ratings yet

- KKR Investor PresentationDocument229 pagesKKR Investor Presentationcjwerner100% (1)

- Q1 2021 Earnings Call: Strategic Priorities and Financial ResultsDocument35 pagesQ1 2021 Earnings Call: Strategic Priorities and Financial ResultsMohit SinghNo ratings yet

- Big Short Movie ReviewDocument14 pagesBig Short Movie ReviewRohan GilaniNo ratings yet

- Kellog PESTLIED For Mexico & PeruDocument25 pagesKellog PESTLIED For Mexico & PeruIoana AgrosoaieNo ratings yet

- Material Requirement Planning PresentationDocument32 pagesMaterial Requirement Planning PresentationAmol BhongadeNo ratings yet

- Indostar: BSE Limited National Stock Exchange of India LimitedDocument49 pagesIndostar: BSE Limited National Stock Exchange of India LimitedAjay BaligaNo ratings yet

- Fourth Quarter 2019 Earnings PresentationDocument26 pagesFourth Quarter 2019 Earnings PresentationShambavaNo ratings yet

- MITT Q1 2022 Earnings Presentation v10 - FiledDocument22 pagesMITT Q1 2022 Earnings Presentation v10 - FiledGiovanni OrsariNo ratings yet

- Huntington National Bank 2021 Q3 Earnings ReviewDocument40 pagesHuntington National Bank 2021 Q3 Earnings ReviewUrderglewerNo ratings yet

- Aviva 2012 Full Year Results PresentationDocument32 pagesAviva 2012 Full Year Results PresentationAviva GroupNo ratings yet

- 2019 North America Investor Tour PresentationsDocument84 pages2019 North America Investor Tour PresentationsNoshan OneitoNo ratings yet

- Capital Limited: H1 2021 Results PresentationDocument35 pagesCapital Limited: H1 2021 Results PresentationFadili ElhafedNo ratings yet

- Investor Presentation - Q2FY22 - 22 FinalDocument62 pagesInvestor Presentation - Q2FY22 - 22 FinalSurya VamsiNo ratings yet

- Investor Presentation: Fourth Quarter 2021Document41 pagesInvestor Presentation: Fourth Quarter 2021orvinwankeNo ratings yet

- Oxy 4 Q 21 Conference Call SlidesDocument48 pagesOxy 4 Q 21 Conference Call SlidesAmol AminNo ratings yet

- Axis Investor Deck v2.4Document20 pagesAxis Investor Deck v2.4Puneet GoelNo ratings yet

- Fall 2021 Investor Slides FINALDocument73 pagesFall 2021 Investor Slides FINALlurigloplayNo ratings yet

- Axis Investor Q3Document19 pagesAxis Investor Q3Puneet GoelNo ratings yet

- F - N & G W A P A: Ranco Evada OLD Heaton Nnounce Lan of RrangementDocument14 pagesF - N & G W A P A: Ranco Evada OLD Heaton Nnounce Lan of RrangementRyan DahlNo ratings yet

- Citi 2nd QTR ResultsDocument10 pagesCiti 2nd QTR ResultsTim MooreNo ratings yet

- Accounting Unit 1 HomeworkDocument8 pagesAccounting Unit 1 Homeworkyeelinxu1128No ratings yet

- Q4 2022 Earnings PresentationDocument21 pagesQ4 2022 Earnings PresentationCesar AugustoNo ratings yet

- Q322 Investor PresentationDocument42 pagesQ322 Investor PresentationAlex ENo ratings yet

- Q4 2022 Investor Presentation FinalDocument18 pagesQ4 2022 Investor Presentation Finalmagdalena floresNo ratings yet

- Whitecap Resources Inc.: Equity ResearchDocument7 pagesWhitecap Resources Inc.: Equity ResearchForexliveNo ratings yet

- Aviva PLC HY2021 Results PresentationDocument49 pagesAviva PLC HY2021 Results PresentationSimonSaysNo ratings yet

- CS 2023 Fixed-Income-Investor-UpdateDocument20 pagesCS 2023 Fixed-Income-Investor-UpdateJohn GrundNo ratings yet

- Berry Plastics Group Investor Presentation August 2019 - FINALDocument42 pagesBerry Plastics Group Investor Presentation August 2019 - FINALAndyNo ratings yet

- Second Quarter 2021 Results: Credit SuisseDocument38 pagesSecond Quarter 2021 Results: Credit SuisseVu HoangNo ratings yet

- Titomic H1 23 Results Company PresentationDocument28 pagesTitomic H1 23 Results Company PresentationJohn JonovskiNo ratings yet

- Q1 Interim Management Statement: Presentation To Analysts and Investors - 25 April 2018Document3 pagesQ1 Interim Management Statement: Presentation To Analysts and Investors - 25 April 2018saxobobNo ratings yet

- MCK q2 Fy22 Presentation FinalDocument31 pagesMCK q2 Fy22 Presentation FinalFaris RahmanNo ratings yet

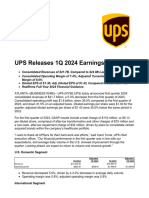

- UPS Releases 1Q 2024 Earnings: U.S. Domestic SegmentDocument8 pagesUPS Releases 1Q 2024 Earnings: U.S. Domestic Segmentrborgesdossantos37No ratings yet

- 2022 Q2 BAM LTR To Shareholders FF BDocument8 pages2022 Q2 BAM LTR To Shareholders FF BDan-S. ErmicioiNo ratings yet

- 2022 - HCPEA - Financial Due Diligence OverviewDocument25 pages2022 - HCPEA - Financial Due Diligence OverviewYogender Singh RawatNo ratings yet

- Ge Webcast Presentation 07282009Document32 pagesGe Webcast Presentation 07282009ZerohedgeNo ratings yet

- The Management 10 KgsDocument14 pagesThe Management 10 KgsskimbryNo ratings yet

- Qwest: A Focus On Presentation and Disclosure: SynopsisDocument3 pagesQwest: A Focus On Presentation and Disclosure: SynopsisCryptic LollNo ratings yet

- Project Finance 2008Document176 pagesProject Finance 2008Piyush VakilNo ratings yet

- Popular, Inc. Conference Call PresentationDocument24 pagesPopular, Inc. Conference Call PresentationRubén E. Morales RiveraNo ratings yet

- STRR Investor Deck - May 2021 - FinalDocument34 pagesSTRR Investor Deck - May 2021 - Finalsawilson1No ratings yet

- Airtel Africa Investor Presentation FY 2022Document44 pagesAirtel Africa Investor Presentation FY 2022Ranbir KapoorNo ratings yet

- Enbridge FY21Document103 pagesEnbridge FY21BrockNo ratings yet

- Teneco Federal MergerDocument29 pagesTeneco Federal Mergerdont-want100% (1)

- RIIO2 FD - NG Response - FinalDocument14 pagesRIIO2 FD - NG Response - FinalSerge KabatiNo ratings yet

- Bank of America Merrill Lynch 2009 Global Industries Conference December 8, 2009Document29 pagesBank of America Merrill Lynch 2009 Global Industries Conference December 8, 2009traunerdjtNo ratings yet

- Bandhan Bankinvestor - Presentation - Q2FY21-22Document28 pagesBandhan Bankinvestor - Presentation - Q2FY21-22dumboooodogNo ratings yet

- OriginalDocument52 pagesOriginalmdyafi8084No ratings yet

- 1q23 Results PresentationDocument28 pages1q23 Results PresentationKumar SaketNo ratings yet

- Draft CooperDocument3 pagesDraft CooperRitveek GargNo ratings yet

- FISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020Document25 pagesFISCAL 2021 Q2 Earnings: NOVEMBER 5, 2020sl7789No ratings yet

- UPSSDocument12 pagesUPSSAndre TorresNo ratings yet

- Capitaland 2021 H1Document88 pagesCapitaland 2021 H1Kiva DangNo ratings yet

- Enphase Investor Day 11 - 16 - 2021 - LowresDocument68 pagesEnphase Investor Day 11 - 16 - 2021 - LowresBruno CarvalheiroNo ratings yet

- 2022 ND - FM Suggested AnswerDocument10 pages2022 ND - FM Suggested Answermiradvance studyNo ratings yet

- Maxwell Needham Conference DeckDocument15 pagesMaxwell Needham Conference DeckFred Lamert100% (6)

- Five Stages of The Entrepreneurial ProcessDocument12 pagesFive Stages of The Entrepreneurial ProcessLakshmish Gopal60% (5)

- Chapter 3 Productivity, Innovation, and Strategy: Experiencing MIS, Canadian Edition, 5e (Kroenke)Document24 pagesChapter 3 Productivity, Innovation, and Strategy: Experiencing MIS, Canadian Edition, 5e (Kroenke)ayaNo ratings yet

- Business Combination - EM Sample ProblemDocument32 pagesBusiness Combination - EM Sample ProblemJohn Stephen PendonNo ratings yet

- Supplier SelectionDocument10 pagesSupplier Selectionmihai simionescu0% (1)

- Measuring Financial Literacy PDFDocument21 pagesMeasuring Financial Literacy PDFVishal SutharNo ratings yet

- PPB3033 Introductory Management Assignment 2Document25 pagesPPB3033 Introductory Management Assignment 2Amirah JaleelNo ratings yet

- Submitted To: Submitted By:: Himani Aggarwal Diksha JaiswalDocument12 pagesSubmitted To: Submitted By:: Himani Aggarwal Diksha JaiswalDiksha JaiswalNo ratings yet

- WGSN CoolhuntingDocument6 pagesWGSN CoolhuntingvictoriasvenssonNo ratings yet

- "Threahcy Boutique": Business PlanDocument6 pages"Threahcy Boutique": Business PlanWenslette Imee C. BalauroNo ratings yet

- BMO Nesbitt Burns - Research Highlights - March 5Document32 pagesBMO Nesbitt Burns - Research Highlights - March 5smutgremlinNo ratings yet

- Client Risk Profile QuestionaireDocument3 pagesClient Risk Profile QuestionaireKewal TareNo ratings yet

- 2014 - A - Levels Actual Grade A Essay by Harvey LeeDocument3 pages2014 - A - Levels Actual Grade A Essay by Harvey Leecherylhzy100% (1)

- Globalization Operation 4Document1 pageGlobalization Operation 4Alvin Gee Kin YuenNo ratings yet

- Refresher Illustrative Problems - Partnership Liquidation LumpsumDocument2 pagesRefresher Illustrative Problems - Partnership Liquidation LumpsumLeiNo ratings yet

- Students Are The Future of A NationDocument1 pageStudents Are The Future of A NationJumadin Mu'adzNo ratings yet

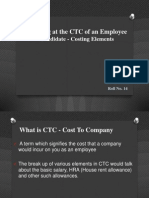

- Arriving at The CTC of An Employee, Hadavle SirDocument13 pagesArriving at The CTC of An Employee, Hadavle SirRogil Jacob DanielNo ratings yet

- Bank Copy Account Copy Academic Copy StudentDocument2 pagesBank Copy Account Copy Academic Copy StudentAashiq Hussain Peerzada 5314-FSL/LLB/F17No ratings yet

- Process of Assurance: Planning The AssignmentDocument30 pagesProcess of Assurance: Planning The AssignmentAslam HossainNo ratings yet

- Talent Acquisition and Talent ManagementDocument14 pagesTalent Acquisition and Talent ManagementKalpita KotkarNo ratings yet

- Sanchit - Sharma EX2019 ChallengeYourself 4 3Document4 pagesSanchit - Sharma EX2019 ChallengeYourself 4 3sanchit sharmaNo ratings yet

- Bulk Duitnow (RPP)Document24 pagesBulk Duitnow (RPP)jamal mohdNo ratings yet

- Introduction To RetailingDocument7 pagesIntroduction To RetailingShabana ShabzzNo ratings yet

- Corporate Plan SLBFE PDFDocument38 pagesCorporate Plan SLBFE PDFSisiraPinnawalaNo ratings yet

- Consumer Behaviour - PGDMMDocument20 pagesConsumer Behaviour - PGDMMPranesh DebnathNo ratings yet