You might also like

- Corporate GovernanceDocument21 pagesCorporate GovernancesanupsimonNo ratings yet

- Irac AnalysisDocument6 pagesIrac AnalysisVaishali RathiNo ratings yet

- Divorce Rate of Kerala in Comparison To Other StatesDocument9 pagesDivorce Rate of Kerala in Comparison To Other StatesAditi Bhawsar100% (1)

- Unit 7Document32 pagesUnit 7Radhika SinghaniaNo ratings yet

- Minority Shareholder Protection in IndiaDocument18 pagesMinority Shareholder Protection in IndiaSai Kiran AdusumalliNo ratings yet

- Shareholder Activism in India - Practical LawDocument10 pagesShareholder Activism in India - Practical LawSommya KhandelwalNo ratings yet

- Corporate Law Course ASS 1Document7 pagesCorporate Law Course ASS 1Surabhi singhalNo ratings yet

- R & B M S C A: Ights Enefits To Inority Hareholders Under Ompanies CTDocument5 pagesR & B M S C A: Ights Enefits To Inority Hareholders Under Ompanies CTDeepanshu JharkhandeNo ratings yet

- Challenges in Protecting The Rights of Minority Shareholders-Puneet Rathsharma, Kunal Mehta - BW BusinessworldDocument5 pagesChallenges in Protecting The Rights of Minority Shareholders-Puneet Rathsharma, Kunal Mehta - BW BusinessworldVic BNo ratings yet

- 8141principles of Corporate Governance - OECD Annotations and Indian ConnotationsDocument8 pages8141principles of Corporate Governance - OECD Annotations and Indian Connotations2nablsNo ratings yet

- Independent Directors of A CompanyDocument16 pagesIndependent Directors of A CompanySaumya SrividyaNo ratings yet

- Company FNLDocument30 pagesCompany FNLpriyaNo ratings yet

- Resolution of Disputes NotesDocument114 pagesResolution of Disputes NotesV.Vidhya VasiniNo ratings yet

- BUSINESS ENTITIES, NGONGO LUNDIKAZI 201813006 FinallyDocument4 pagesBUSINESS ENTITIES, NGONGO LUNDIKAZI 201813006 FinallylundingongoNo ratings yet

- Company Law AssignmentDocument6 pagesCompany Law AssignmentAbhishek SinghalNo ratings yet

- Shareholder Activism As A New Facet of Corporate Governance in IndiaDocument11 pagesShareholder Activism As A New Facet of Corporate Governance in IndiaReeya PrakashNo ratings yet

- Rights and Privileges of ShareholdersDocument40 pagesRights and Privileges of Shareholdersswatantra.s887245No ratings yet

- Law and Practice of Governance in The Ethiopian Share CompaniesDocument12 pagesLaw and Practice of Governance in The Ethiopian Share CompaniesAba JifarNo ratings yet

- Company Law Ii End Term NotesDocument40 pagesCompany Law Ii End Term NotesKumar PrabhakarNo ratings yet

- Corpoaret Governance - NeedDocument30 pagesCorpoaret Governance - NeedVaishnavi VenkatesanNo ratings yet

- Article 202Document14 pagesArticle 202manoranjan838241No ratings yet

- Governance Failure at SatyamDocument19 pagesGovernance Failure at SatyamAnil KardamNo ratings yet

- Borrowing Powers of Directors of Public Limited CompaniesDocument14 pagesBorrowing Powers of Directors of Public Limited CompaniesMuhammad Saeed BabarNo ratings yet

- CG - An Overview - Article - MSME ReviewDocument7 pagesCG - An Overview - Article - MSME ReviewChaitanya ShahNo ratings yet

- Unit 3Document36 pagesUnit 3aashmibrijet99No ratings yet

- 01 - Corporate Governance - CONCEPTUAL FRAMEWORK OF CORPORATE GOVERNANCEDocument109 pages01 - Corporate Governance - CONCEPTUAL FRAMEWORK OF CORPORATE GOVERNANCEVij88888No ratings yet

- Act 2017Document5 pagesAct 2017John A. DavisNo ratings yet

- Corporate Governance: Indian Institute of Foreign TradeDocument14 pagesCorporate Governance: Indian Institute of Foreign TradeT_haque2No ratings yet

- Independent Directors and Their Role in Corporate GovernanceDocument2 pagesIndependent Directors and Their Role in Corporate GovernanceSALONI KUMARINo ratings yet

- Shareholder ActivismDocument16 pagesShareholder ActivismSiddhant SodhiaNo ratings yet

- Company Law Cheat SheetDocument21 pagesCompany Law Cheat SheetAdarsh RamisettyNo ratings yet

- Future of Corporate Governance in IndiaDocument9 pagesFuture of Corporate Governance in Indiatony montanaNo ratings yet

- Saurabh Singh: The Clause 49 of Listing Agreement With Pertinence To Corporate Governance in IndiaDocument9 pagesSaurabh Singh: The Clause 49 of Listing Agreement With Pertinence To Corporate Governance in IndiaSaurabh singhNo ratings yet

- @csupdates RCD - Chapter - 1 - Dec - 22 - CS - ProfessionalDocument16 pages@csupdates RCD - Chapter - 1 - Dec - 22 - CS - ProfessionalAGHBALOUNo ratings yet

- Company Unit-2Document6 pagesCompany Unit-2thehackerdude09No ratings yet

- An Analysis of The Rights of Minority Shareholders and The Remedies Available To Them in Case of Oppression Done by The Majority ShareholdersDocument14 pagesAn Analysis of The Rights of Minority Shareholders and The Remedies Available To Them in Case of Oppression Done by The Majority ShareholdersIpkshita SinghNo ratings yet

- RCD - Shareholders' Democracy - CS Muskan Gupta - Yes Academy, PuneDocument23 pagesRCD - Shareholders' Democracy - CS Muskan Gupta - Yes Academy, PuneSANTHOSH KUMAR T MNo ratings yet

- Corporate Governance May Be Defined As FollowsDocument7 pagesCorporate Governance May Be Defined As Followsbarkha chandnaNo ratings yet

- Business Ethics (Unit 3)Document6 pagesBusiness Ethics (Unit 3)prabhav1822001No ratings yet

- Consultation Paper of SEBIDocument15 pagesConsultation Paper of SEBIPulkitMathurNo ratings yet

- C P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaDocument54 pagesC P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaPradyoth C JohnNo ratings yet

- 1Document15 pages1srkraman24No ratings yet

- The New Ethiopian Commercial Code A Highlight of Major ChangesDocument5 pagesThe New Ethiopian Commercial Code A Highlight of Major ChangesBooruuNo ratings yet

- Auditing and Corporate GovernanceDocument6 pagesAuditing and Corporate Governancesuraj agarwalNo ratings yet

- Corporate Governance Part-1Document13 pagesCorporate Governance Part-1Varun KumarNo ratings yet

- Research PaperDocument16 pagesResearch PaperavinashbawaneNo ratings yet

- Neral Features of Business Forms in Vietnam - ENT LawDocument5 pagesNeral Features of Business Forms in Vietnam - ENT LawPassionNo ratings yet

- Comparative Analysis of Corporate Governance Code in India and USDocument6 pagesComparative Analysis of Corporate Governance Code in India and USvishesh knNo ratings yet

- Assignment - 1: Indukaka Ipcowala Institute of ManagementDocument7 pagesAssignment - 1: Indukaka Ipcowala Institute of ManagementhardikgosaiNo ratings yet

- Corporate Governance Framework in India By: Vaish Associates Advocates Vinay Vaish Hitender MehtaDocument28 pagesCorporate Governance Framework in India By: Vaish Associates Advocates Vinay Vaish Hitender Mehtaeric grimsonNo ratings yet

- Company Law ProjectDocument7 pagesCompany Law ProjectSiddhanth AroraNo ratings yet

- Company JonaDocument22 pagesCompany JonaUjjwal AnandNo ratings yet

- Assignment of Company LawDocument26 pagesAssignment of Company LawPriyankaJain0% (1)

- N0.2 ConstitutionDocument10 pagesN0.2 ConstitutionKaiwenNo ratings yet

- Protection of Minority Rights Under Company's Affairs:: Aparajita BhargavaDocument2 pagesProtection of Minority Rights Under Company's Affairs:: Aparajita BhargavaKrishan Bir SinghNo ratings yet

- Corporate Law AssignmentDocument11 pagesCorporate Law AssignmentGoranshi GuptaNo ratings yet

- How A Board of Trustees WorksDocument3 pagesHow A Board of Trustees WorksPhilip VinskyNo ratings yet

- Corporate GovernanceDocument23 pagesCorporate GovernancehhhhhhhuuuuuyyuyyyyyNo ratings yet

- 10 Issues in Implementing Corporate Governance Practices 1. Getting The Board RightDocument4 pages10 Issues in Implementing Corporate Governance Practices 1. Getting The Board Rightmohamed saidNo ratings yet

- Company ActDocument92 pagesCompany ActSunny ProjectNo ratings yet

- Is The Indian Constitution LiberalDocument12 pagesIs The Indian Constitution LiberalAditi BhawsarNo ratings yet

- Overriding Effect of Arbitration Act Over Insolvency and Bankruptcy CodeDocument11 pagesOverriding Effect of Arbitration Act Over Insolvency and Bankruptcy CodeAditi BhawsarNo ratings yet

- International Law of The Sea: An Overlook and Case Study: Arif AhmedDocument20 pagesInternational Law of The Sea: An Overlook and Case Study: Arif AhmedAditi BhawsarNo ratings yet

- Patent Politics and The Covid-19 VaccineDocument16 pagesPatent Politics and The Covid-19 VaccineAditi BhawsarNo ratings yet

- An Introduction To Public International Law by S K Verma 2nd Edition PDFDocument1,150 pagesAn Introduction To Public International Law by S K Verma 2nd Edition PDFAditi BhawsarNo ratings yet

- Humanitarian Law: The Challenges Faced While Implementing International Humanitarian LawDocument3 pagesHumanitarian Law: The Challenges Faced While Implementing International Humanitarian LawAditi BhawsarNo ratings yet

- The Refugee Concept Under International LawDocument4 pagesThe Refugee Concept Under International LawAditi BhawsarNo ratings yet

- Trade Fair Monitoring: Promotional Material Such As Brochure, Price List Etc. Collecting Evidences of SamplesDocument2 pagesTrade Fair Monitoring: Promotional Material Such As Brochure, Price List Etc. Collecting Evidences of SamplesAditi BhawsarNo ratings yet

- Name: Aditi Bhawsar College: National University of Study and Research in Law, Ranchi. Contact No.: 7000578331Document8 pagesName: Aditi Bhawsar College: National University of Study and Research in Law, Ranchi. Contact No.: 7000578331Aditi BhawsarNo ratings yet

- Company Name Purchases: 1. Unique Component: in Flipkart Internet Private Limited, Flipkart Is The Unique ComponentDocument2 pagesCompany Name Purchases: 1. Unique Component: in Flipkart Internet Private Limited, Flipkart Is The Unique ComponentAditi BhawsarNo ratings yet

- Ip Acquisition ServiceDocument2 pagesIp Acquisition ServiceAditi BhawsarNo ratings yet

- Dicey'S Rule of Law: National University of Study and Research in Law, RanchiDocument11 pagesDicey'S Rule of Law: National University of Study and Research in Law, RanchiAditi BhawsarNo ratings yet

- National University OF Study AND Research IN Law, Ranchi: Submitted TO Submitted BYDocument10 pagesNational University OF Study AND Research IN Law, Ranchi: Submitted TO Submitted BYAditi BhawsarNo ratings yet

- Directors DutiesDocument27 pagesDirectors Dutieskalaclinton644No ratings yet

- Company Law Notes - Unit-IvDocument58 pagesCompany Law Notes - Unit-IvTanya MalviyaNo ratings yet

- CORPORATE RAIDERS OriginalDocument16 pagesCORPORATE RAIDERS OriginalSandeep KaurNo ratings yet

- The Effect of Company Size and Leverage Towards Company Performance After Malaysian Economic CrisisDocument18 pagesThe Effect of Company Size and Leverage Towards Company Performance After Malaysian Economic CrisisIwan SetiawanNo ratings yet

- Form 45 - Return of Beneficial InterestDocument6 pagesForm 45 - Return of Beneficial InterestRussell O'NeillNo ratings yet

- Assignment Chapter 15Document4 pagesAssignment Chapter 15Ibrahim AbdallahNo ratings yet

- Project Stella RHP SignedDocument536 pagesProject Stella RHP SignedabhayNo ratings yet

- Industry and Environmental Analysis: Business Opportunity IdentificationDocument17 pagesIndustry and Environmental Analysis: Business Opportunity IdentificationHannahbea LindoNo ratings yet

- Ma2-2019 - Phan Gia BaoDocument8 pagesMa2-2019 - Phan Gia BaoBao PNo ratings yet

- First Meeting Minutes of ShareholdersDocument4 pagesFirst Meeting Minutes of ShareholdersFetco PrimeNo ratings yet

- CG Progression Matrix SME 043019Document12 pagesCG Progression Matrix SME 043019Hassan ZareenNo ratings yet

- MSEZ Annual Report 2019 20 - FinalDocument180 pagesMSEZ Annual Report 2019 20 - FinalDebasis MohantyNo ratings yet

- FM Study Notes ZellDocument185 pagesFM Study Notes Zell5561 ROSHAN K PATELNo ratings yet

- Entrepreneurship - MGT602 Power Point Slides Lecture 29Document11 pagesEntrepreneurship - MGT602 Power Point Slides Lecture 29faizan.kareemNo ratings yet

- AB CFS 217675 Oil & Gas Ltd.Document3 pagesAB CFS 217675 Oil & Gas Ltd.Karen KleissNo ratings yet

- Important Mcqs - Chapter Iv: Company Law Share Capital and Debentures - Part 3Document28 pagesImportant Mcqs - Chapter Iv: Company Law Share Capital and Debentures - Part 3amitNo ratings yet

- Accounting For Corporations IIIDocument25 pagesAccounting For Corporations IIIibrahim mohamedNo ratings yet

- Shareholders Vs ManagementDocument33 pagesShareholders Vs ManagementTeo VisanNo ratings yet

- Planning and Executing Early Exits Alberta Deal Generator Edmonton 20091105Document65 pagesPlanning and Executing Early Exits Alberta Deal Generator Edmonton 20091105Farley RamosNo ratings yet

- Modulo 7, RepasoDocument39 pagesModulo 7, RepasoAngel MuñozNo ratings yet

- Tutorial Letter 102/3/2018: Entrepreneurial LawDocument17 pagesTutorial Letter 102/3/2018: Entrepreneurial LawJabulani MakanyaNo ratings yet

- Anti Takeover MeasuresDocument54 pagesAnti Takeover MeasuresParvesh Aghi50% (2)

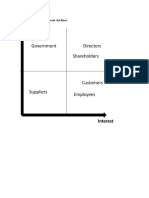

- Government Directors Shareholders: PowerDocument5 pagesGovernment Directors Shareholders: Powerhuy dinh ducNo ratings yet

- Partial Text 2Document7 pagesPartial Text 2Spring000No ratings yet

- Tullow Oil PLC 2017 Annual Report PDFDocument188 pagesTullow Oil PLC 2017 Annual Report PDFBernard MusembiNo ratings yet

- Types of Business Organization The Private SectorDocument7 pagesTypes of Business Organization The Private SectorAmna ShawgiNo ratings yet

- Vbook - Pub Business Combination QuizDocument3 pagesVbook - Pub Business Combination QuizRialeeNo ratings yet

- 2015 Fluor Sustainability Report PDFDocument57 pages2015 Fluor Sustainability Report PDFBlue CliffNo ratings yet

- Board of Directors: Selection, Compensation, and RemovalDocument25 pagesBoard of Directors: Selection, Compensation, and Removalshahzad AhmadNo ratings yet

- A 1 The Statement Is Entitled Consolidated Balance SheetsDocument1 pageA 1 The Statement Is Entitled Consolidated Balance SheetsM Bilal SaleemNo ratings yet