You might also like

- Tesco Bank - No Claim Discount 28.11.17Document2 pagesTesco Bank - No Claim Discount 28.11.17eujenio50% (2)

- Tom Houggard MergedDocument269 pagesTom Houggard MergedTomojeet Chakraborty100% (2)

- Porter's Five Forces: Understand competitive forces and stay ahead of the competitionFrom EverandPorter's Five Forces: Understand competitive forces and stay ahead of the competitionRating: 4 out of 5 stars4/5 (10)

- Business Economics Assignment (Ankit Sonj)Document4 pagesBusiness Economics Assignment (Ankit Sonj)ankitsoni2328No ratings yet

- Lecture Chapter6Document7 pagesLecture Chapter6Angelica Joy ManaoisNo ratings yet

- Monopolistic CompetitionDocument1 pageMonopolistic CompetitionMVPNo ratings yet

- Monopolistic CompetitionDocument4 pagesMonopolistic CompetitionCookie LayugNo ratings yet

- Market Structure and Price Out Determination - 20231121 - 220505 - 0000Document26 pagesMarket Structure and Price Out Determination - 20231121 - 220505 - 0000CIELO ESTONANTONo ratings yet

- Lesson 4Document5 pagesLesson 4April Joy DelacruzNo ratings yet

- Subject-Business Economics Project Report On Different MarketsDocument5 pagesSubject-Business Economics Project Report On Different MarketsMegha PatelNo ratings yet

- Mefa Free Writing 5Document5 pagesMefa Free Writing 5abinashreddy792No ratings yet

- Monopolistic CompetitionDocument3 pagesMonopolistic CompetitionAkshay RathiNo ratings yet

- Market StructuresDocument8 pagesMarket StructuresJojie De RamosNo ratings yet

- MC ScriptDocument2 pagesMC ScriptGeoffrey PilarNo ratings yet

- 1.5.monopolistic CompetitionDocument13 pages1.5.monopolistic CompetitionManhin Bryan KoNo ratings yet

- Characteristics of OligopolyDocument3 pagesCharacteristics of OligopolyJulie ann YbanezNo ratings yet

- ECONOMICSDocument6 pagesECONOMICSShuchismita KashyapNo ratings yet

- 4 Market Structures SOBREVINASDocument3 pages4 Market Structures SOBREVINASpongsensei11No ratings yet

- Oligopoly in India: A Case Study.Document37 pagesOligopoly in India: A Case Study.The Munning Guy100% (4)

- Monopolistic Competition and Oligopoly 1Document6 pagesMonopolistic Competition and Oligopoly 1Katrina LabisNo ratings yet

- 62219ac095fc49000f2e0f1d-1646369555-SIM BE 121 Week 8-9 Big PictureDocument4 pages62219ac095fc49000f2e0f1d-1646369555-SIM BE 121 Week 8-9 Big PictureRhea Gin RamosNo ratings yet

- Economics 1: Types of Markets Week 5 Rafał Sieradzki, Ph.D. Cracow University of EconomicsDocument39 pagesEconomics 1: Types of Markets Week 5 Rafał Sieradzki, Ph.D. Cracow University of EconomicsPretty SweetNo ratings yet

- Unit 4 CC 4 PDFDocument49 pagesUnit 4 CC 4 PDFKamlesh AgrawalNo ratings yet

- Market Structure NotesDocument8 pagesMarket Structure NotesABDUL HADINo ratings yet

- Theory of Market: Perfect Competition: Nature and Relevance Monopoly and Monopolistic Competition OligopolyDocument18 pagesTheory of Market: Perfect Competition: Nature and Relevance Monopoly and Monopolistic Competition OligopolyDivyanshu BargaliNo ratings yet

- Economics Market StructureDocument30 pagesEconomics Market StructureKim simborioNo ratings yet

- Managerial Eco 2 - MergedDocument8 pagesManagerial Eco 2 - Mergedlolalone58No ratings yet

- Report Kay Maam ManaloDocument18 pagesReport Kay Maam ManaloMary Anne De LunaNo ratings yet

- MKT Structure !Document25 pagesMKT Structure !jakowanNo ratings yet

- Market StructuresDocument2 pagesMarket StructuressaaruzerruNo ratings yet

- Economics AssignmentDocument21 pagesEconomics AssignmentMichael RopNo ratings yet

- Astu Micro II ModuleDocument247 pagesAstu Micro II Modulezemede zelekeNo ratings yet

- Market StructureDocument3 pagesMarket StructurePranjal TiwariNo ratings yet

- Monopolistic CompetitionDocument13 pagesMonopolistic CompetitionPark MinaNo ratings yet

- BA1. Malabanan Nica.Document4 pagesBA1. Malabanan Nica.Andrea WaganNo ratings yet

- 21 CenturyDocument19 pages21 CenturyDanica LlamazaresNo ratings yet

- WK12 Basic-MicroeconomicsDocument10 pagesWK12 Basic-MicroeconomicsWhats PoppinNo ratings yet

- AAU Micro II ModuleDocument245 pagesAAU Micro II Moduleyiho83% (6)

- Monopolistically CompetitiveDocument26 pagesMonopolistically Competitivebeth el100% (1)

- BE II - U1 Market Structure and PricingDocument6 pagesBE II - U1 Market Structure and PricingVishal AgrawalNo ratings yet

- Market StructuresDocument59 pagesMarket StructuresCharlene Mae GraciasNo ratings yet

- Explorations in Economics: Alan B. Krueger & David A. AndersonDocument30 pagesExplorations in Economics: Alan B. Krueger & David A. AndersonZaw Ye HtikeNo ratings yet

- 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsDocument6 pages8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsMikkoNo ratings yet

- Task Monopolistic CompetitionDocument2 pagesTask Monopolistic CompetitionmulianiNo ratings yet

- Market StructureDocument4 pagesMarket StructurePranjal TiwariNo ratings yet

- Monopolistic CompetitionDocument3 pagesMonopolistic Competitionjoshcastv27No ratings yet

- Market StructuresDocument12 pagesMarket StructuresTanya PribylevaNo ratings yet

- Module 6 - ReadingDocument7 pagesModule 6 - ReadingChristine Mae MansiaNo ratings yet

- Microeconomics ReportDocument5 pagesMicroeconomics Reportad0986523No ratings yet

- What Is Market Structure?Document4 pagesWhat Is Market Structure?S S addamsNo ratings yet

- Firms in Competitive Markets - BesarioDocument2 pagesFirms in Competitive Markets - BesarioLorelyn Sharaim BesarioNo ratings yet

- Me Market-StructureDocument3 pagesMe Market-Structurebenedick marcialNo ratings yet

- Applied Economics Module 5Document11 pagesApplied Economics Module 5Sher-Anne Fernandez - Belmoro67% (3)

- Me 4 (Part A)Document6 pagesMe 4 (Part A)Anuj YadavNo ratings yet

- Managerial Economics - Chapter 6Document48 pagesManagerial Economics - Chapter 6francis albaracinNo ratings yet

- 13 Market StructureDocument14 pages13 Market StructureCristine ParedesNo ratings yet

- Part Report Applied EconDocument18 pagesPart Report Applied Econrosemarie salipioNo ratings yet

- Types of Market StructuresDocument3 pagesTypes of Market Structuresjojo chowNo ratings yet

- Types of Market and Price DeterminationDocument4 pagesTypes of Market and Price DeterminationSaurabhNo ratings yet

- Applied Economics q1 w5 Capistrano Camille G.Document21 pagesApplied Economics q1 w5 Capistrano Camille G.Cheska BlaireNo ratings yet

- Topic No. 4-Defenition of Market StructureDocument5 pagesTopic No. 4-Defenition of Market StructureKristy Veyna BautistaNo ratings yet

- Market Sturucture and PriceDocument3 pagesMarket Sturucture and PriceJessa MingoNo ratings yet

- Performance ManagementDocument23 pagesPerformance Managementankitsoni2328No ratings yet

- Organizational DevelopmentDocument14 pagesOrganizational Developmentankitsoni2328No ratings yet

- Hart - FullerDocument3 pagesHart - Fullerankitsoni2328No ratings yet

- Nanotechnology ASCEpaperfinalDocument10 pagesNanotechnology ASCEpaperfinalankitsoni2328No ratings yet

- Speccoats AntiCorrosiveBrochureDocument36 pagesSpeccoats AntiCorrosiveBrochurereinpolyNo ratings yet

- Assignment 1Document4 pagesAssignment 1saitamaNo ratings yet

- Smed PDFDocument10 pagesSmed PDFSakline MinarNo ratings yet

- Results For Sai Teja Traders - Rajahmundry - ZonalinfoDocument4 pagesResults For Sai Teja Traders - Rajahmundry - ZonalinfoManoj Digi LoansNo ratings yet

- Every Child Matters A Practical Guide For Teachers PDFDocument2 pagesEvery Child Matters A Practical Guide For Teachers PDFBarbaraNo ratings yet

- WW Treatment EENV 4332 HWK 1Document2 pagesWW Treatment EENV 4332 HWK 1Karim ShamashergyNo ratings yet

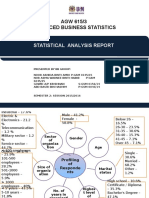

- AGW 615/3 Advanced Business Statistics: Statistical Analysis ReportDocument10 pagesAGW 615/3 Advanced Business Statistics: Statistical Analysis ReportNida AmriNo ratings yet

- 20th Century Arch'ReDocument6 pages20th Century Arch'ReRachelleGomezLatrasNo ratings yet

- 5 A Case Study: The Domino PuzzleDocument6 pages5 A Case Study: The Domino PuzzleqwqqwwNo ratings yet

- U3 01 Simplifying Shapes GuideDocument4 pagesU3 01 Simplifying Shapes GuideMuhammad Bobby BangsawanNo ratings yet

- Alfred Rosenberg's MemoirsDocument119 pagesAlfred Rosenberg's MemoirsSir Robin of LoxleyNo ratings yet

- Enc28j60 HDocument12 pagesEnc28j60 HMokhammad Sanpradipto JaluntoroNo ratings yet

- Personal StatementDocument4 pagesPersonal StatementZoha RehmanNo ratings yet

- Yarn Over 101Document3 pagesYarn Over 101Bea Ann83% (6)

- Sheet Metal Nesting Report For Plasma and Laser CuttingDocument1 pageSheet Metal Nesting Report For Plasma and Laser CuttingcititorulturmentatNo ratings yet

- JV Punj Lloyd - SICIMDocument9 pagesJV Punj Lloyd - SICIMBarock NaturelNo ratings yet

- Excavator O&KDocument8 pagesExcavator O&Keknasius iwan sugoro100% (2)

- Strategic ManagementDocument214 pagesStrategic ManagementThomas JinduNo ratings yet

- Biopure BrochureDocument7 pagesBiopure BrochureJOSE SANTOS PAZ VARELA0% (1)

- Lecture 4. Theories of International TradeDocument39 pagesLecture 4. Theories of International TradeBorn HyperNo ratings yet

- Sbo43sp2 Whats New enDocument14 pagesSbo43sp2 Whats New enPierreNo ratings yet

- Systems": General Ledger Systems ShouldDocument2 pagesSystems": General Ledger Systems ShouldKaren CaelNo ratings yet

- Financial CrisisDocument53 pagesFinancial CrisisMehedi Hassan RanaNo ratings yet

- Lecture 13 - Lumber GradingDocument20 pagesLecture 13 - Lumber GradingimanolkioNo ratings yet

- BSC It Syllabus Mumbai UniversityDocument81 pagesBSC It Syllabus Mumbai UniversitysanNo ratings yet

- Enforcement Question 3Document2 pagesEnforcement Question 3Tan Chen WuiNo ratings yet

- Principles of Compiler Design PDFDocument177 pagesPrinciples of Compiler Design PDFLavlesh Jaiswal0% (1)

- PDPR Bahasa Inggeris Tahun 5 12 July 2021 / MondayDocument12 pagesPDPR Bahasa Inggeris Tahun 5 12 July 2021 / MondayKiran KaurNo ratings yet