You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Regina Martin OIG ReportDocument287 pagesRegina Martin OIG ReportChris GothnerNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Engineering Economy Umak: Time Value of MoneyDocument26 pagesEngineering Economy Umak: Time Value of MoneyTangina DenNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Property Amount: Compute For The Gross Estate of Each Decedent BelowDocument2 pagesProperty Amount: Compute For The Gross Estate of Each Decedent Belowjarlen cosasNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- India's Banking System:: Introduction To Indian Banking IndustryDocument3 pagesIndia's Banking System:: Introduction To Indian Banking IndustrySathish KumarNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Recruitment of Probationary Officers in State Bank of IndiaDocument4 pagesRecruitment of Probationary Officers in State Bank of Indiaशेरसिंह खदावNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- November 2010 India DailyDocument147 pagesNovember 2010 India DailymitbanNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- GIRO FormDocument1 pageGIRO FormBrian EllisNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Form A Scss Ac Opening Form 28 Nov 2016Document3 pagesForm A Scss Ac Opening Form 28 Nov 2016Suraj KumarNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Advanced Accounting CH 14, 15Document16 pagesAdvanced Accounting CH 14, 15jessicaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- F214741 Berat Zeka Cafe Le Marche Cafe Le Marche EUDocument2 pagesF214741 Berat Zeka Cafe Le Marche Cafe Le Marche EUCristian CoffeelingNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Bank ReconciliationDocument18 pagesBank ReconciliationFem FataleNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- World Bank GlossaryDocument435 pagesWorld Bank Glossarydon_isauroNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Bacolod City Host Lions Club DISTRICT 301-B1Document2 pagesBacolod City Host Lions Club DISTRICT 301-B1Jackilou BlancoNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

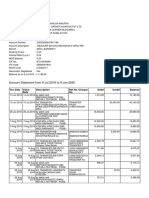

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Volatility Exchange-Traded Notes - Curse or CureDocument25 pagesVolatility Exchange-Traded Notes - Curse or CurelastkraftwagenfahrerNo ratings yet

- Intern JanataDocument59 pagesIntern JanataKhairul IslamNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Associated Bank v. TanDocument1 pageAssociated Bank v. TanAngie JapitanNo ratings yet

- Customer Satisfaction On SharekhanDocument83 pagesCustomer Satisfaction On SharekhanGo Ldy100% (1)

- RiskDocument2 pagesRiskrakesh_danduNo ratings yet

- "Role of SBI in The Indian Banking Sector" Presented By:-Karan Patel-201104100710010 Jignesh Mehta-201104100710048Document10 pages"Role of SBI in The Indian Banking Sector" Presented By:-Karan Patel-201104100710010 Jignesh Mehta-201104100710048Jignesh MehtaNo ratings yet

- El Banco Español-Filipino V. James PetersonDocument1 pageEl Banco Español-Filipino V. James PetersonRia Evita RevitaNo ratings yet

- Practice Problem 2 Cash ReconDocument5 pagesPractice Problem 2 Cash ReconKhyla DivinagraciaNo ratings yet

- Maths F3 KSSM 2019Document132 pagesMaths F3 KSSM 2019蔡卷勋100% (5)

- Brenda Gaba 2021 Electronic Banking ProjectDocument49 pagesBrenda Gaba 2021 Electronic Banking ProjectsamuelNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- ECS FormDocument2 pagesECS FormNaveen NaviNo ratings yet

- Petitioner Vs Vs Respondents: First DivisionDocument8 pagesPetitioner Vs Vs Respondents: First DivisionMichaella Claire LayugNo ratings yet

- KYC Quiz HandoutDocument7 pagesKYC Quiz HandoutBhagyanath MenonNo ratings yet

- 236-Estrada v. Desierto G.R. No. 156160 December 9, 2004Document7 pages236-Estrada v. Desierto G.R. No. 156160 December 9, 2004Jopan SJNo ratings yet

- BES171 Financial Inclusion1 Jandhan Small Savings SchemesDocument29 pagesBES171 Financial Inclusion1 Jandhan Small Savings Schemesroy lexterNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Global Financial Crisis: Module 3 Housing and MortgagesDocument30 pagesThe Global Financial Crisis: Module 3 Housing and MortgagesAlanNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)