You might also like

- Basel II - Assessing The Default and Loss Characteristics of Project Finance LoansDocument23 pagesBasel II - Assessing The Default and Loss Characteristics of Project Finance Loansptgoel0% (1)

- Risk Management and Basel II: Bank Alfalah LimitedDocument72 pagesRisk Management and Basel II: Bank Alfalah LimitedtanhaitanhaNo ratings yet

- Automatic Gearbox ZF 4HP 20Document40 pagesAutomatic Gearbox ZF 4HP 20Damien Jorgensen100% (3)

- Architectural ConcreteDocument24 pagesArchitectural ConcreteSaud PathiranaNo ratings yet

- Risk Based Supervision Under Basel II Jeffrey CarmichaelDocument31 pagesRisk Based Supervision Under Basel II Jeffrey CarmichaelAbhishek MishraNo ratings yet

- BaselDocument38 pagesBaselsourabhs90No ratings yet

- Basel NormsDocument42 pagesBasel NormsBluehacksNo ratings yet

- MineDocument19 pagesMineAbhishek AgrawalNo ratings yet

- Capital Adequacy: Prof. B.B.BhattacharyyaDocument115 pagesCapital Adequacy: Prof. B.B.BhattacharyyaSheetal IyerNo ratings yet

- Basle Ii and Economic CapitalDocument44 pagesBasle Ii and Economic Capitalaboloe5451100% (2)

- The New Basel Capital AccordDocument24 pagesThe New Basel Capital AccordGaurav SonarNo ratings yet

- Base 2Document20 pagesBase 2asifanisNo ratings yet

- Capital Adequacy Mms 2011Document121 pagesCapital Adequacy Mms 2011Aishwary KhandelwalNo ratings yet

- 2011 Early Bird Offer - 2nd Person 25% DiscountDocument8 pages2011 Early Bird Offer - 2nd Person 25% DiscountFaruk HossainNo ratings yet

- International Convergence of Capital Measurement & Capital StandardsDocument57 pagesInternational Convergence of Capital Measurement & Capital StandardsskartyknNo ratings yet

- Unit 0Document57 pagesUnit 0Carey DonNo ratings yet

- Index: Acknowledgement Executive Summary Chapter-1Document85 pagesIndex: Acknowledgement Executive Summary Chapter-1Kiran KatyalNo ratings yet

- The Impact of Credit Risk Management On The Performance of Commercial Banks in CameroonDocument20 pagesThe Impact of Credit Risk Management On The Performance of Commercial Banks in CameroonAmbuj GargNo ratings yet

- CRO Guide To Solvency II: The Journey From Complexity To Best PracticeDocument40 pagesCRO Guide To Solvency II: The Journey From Complexity To Best PracticePablo Velázquez Méndez100% (1)

- Pre ClassPPT 1Document16 pagesPre ClassPPT 1Arjun SainiNo ratings yet

- Risk Management & Basel Ii: By: Kajal Gupta Deepanshu Sapra Sanchit BhasinDocument11 pagesRisk Management & Basel Ii: By: Kajal Gupta Deepanshu Sapra Sanchit Bhasinsanchit bhasinNo ratings yet

- AMM 2008 LawrenceDocument18 pagesAMM 2008 LawrenceSoujanya NagarajaNo ratings yet

- Royal Bank of Canada: BUS 419 - Advanced Derivatives Securities Heng I (Miki) Pun Jeff Chan Macau Chan Nathan YauDocument90 pagesRoyal Bank of Canada: BUS 419 - Advanced Derivatives Securities Heng I (Miki) Pun Jeff Chan Macau Chan Nathan YauAbhijeet PatilNo ratings yet

- Moving Towards Basel Ii: Issues & ConcernsDocument36 pagesMoving Towards Basel Ii: Issues & Concernstejasdhanu786No ratings yet

- Internal Controls in The NewsDocument102 pagesInternal Controls in The NewsManav PatelNo ratings yet

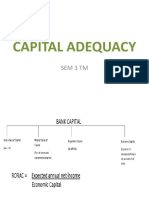

- Capital Adequacy: Sem 3 TMDocument45 pagesCapital Adequacy: Sem 3 TMahsan habibNo ratings yet

- Credit Risk ManagementDocument13 pagesCredit Risk ManagementVallabh UtpatNo ratings yet

- Risk Management and Basel II: Bank Alfalah LimitedDocument72 pagesRisk Management and Basel II: Bank Alfalah LimitedCarl RodriguezNo ratings yet

- Mohan Bhatia BookDocument5 pagesMohan Bhatia Bookr.jeyashankar9550No ratings yet

- Key Features of Basel IDocument16 pagesKey Features of Basel IAltaf Hasan KhanNo ratings yet

- Fraud & Risk Management Workshop2Document26 pagesFraud & Risk Management Workshop2Abubaker KakuleNo ratings yet

- The Future of Prudential Regulation in AsiaDocument19 pagesThe Future of Prudential Regulation in AsiaFiza AnjumNo ratings yet

- Risk Management: Capital Management & Profit PlanningDocument25 pagesRisk Management: Capital Management & Profit Planningharry2learnNo ratings yet

- Certified Strategic ALM 0 Balance Sheet Management Masterclass - 2023Document5 pagesCertified Strategic ALM 0 Balance Sheet Management Masterclass - 2023Sirak AynalemNo ratings yet

- Basel Norms IIDocument3 pagesBasel Norms IImanoranjan838241No ratings yet

- Topic 5-Financial SupervisionDocument43 pagesTopic 5-Financial Supervisionmerlinda ratuNo ratings yet

- Basel NormsDocument20 pagesBasel NormsAbhilasha Mathur100% (1)

- Risk ManagementDocument31 pagesRisk ManagementAnkit ChawlaNo ratings yet

- Theroleofriskgovernanceineffectiveriskmanagement Tunji Adesida 071312Document58 pagesTheroleofriskgovernanceineffectiveriskmanagement Tunji Adesida 071312Mohamed BarbarioNo ratings yet

- Basel 1:: Tier-I Capital Tier-II CapitalDocument4 pagesBasel 1:: Tier-I Capital Tier-II CapitalRafiur RahmanNo ratings yet

- Group 2 Case Basel IIDocument6 pagesGroup 2 Case Basel IInisargpatel19No ratings yet

- Basel II Accord: Presentation To Information Systems Audit and Control AssociationDocument30 pagesBasel II Accord: Presentation To Information Systems Audit and Control AssociationprjiviNo ratings yet

- What Is Basel IIDocument7 pagesWhat Is Basel IIyosefmekdiNo ratings yet

- College ProjectDocument72 pagesCollege Projectcha7738713649No ratings yet

- NYIF Williams Credit Risk Analysis IV 2018Document95 pagesNYIF Williams Credit Risk Analysis IV 2018jojozieNo ratings yet

- Quantifying Operational Risk: Possibilities and Limitations: Hansj Org Furrer Swiss LifeDocument59 pagesQuantifying Operational Risk: Possibilities and Limitations: Hansj Org Furrer Swiss LiferberrospiNo ratings yet

- CMA Exam Part 2: Overview, Syllabus and Pass RateDocument21 pagesCMA Exam Part 2: Overview, Syllabus and Pass RateJaved Khan50% (2)

- Basel Norms I, II and IIIDocument30 pagesBasel Norms I, II and IIIYashwanth PrasadNo ratings yet

- Credit Risk Part I RMBKDocument52 pagesCredit Risk Part I RMBKGourav BaidNo ratings yet

- The Evolution To Basel IIDocument34 pagesThe Evolution To Basel IIShakila ParvinNo ratings yet

- Basel III and Its Implications For Banks' Treasurers: Edited by Prof. Gvs RaoDocument39 pagesBasel III and Its Implications For Banks' Treasurers: Edited by Prof. Gvs Raosubba raoNo ratings yet

- Lecture 7 Credit Risk Basel AccordsDocument44 pagesLecture 7 Credit Risk Basel AccordsAjid Ur RehmanNo ratings yet

- Risk Management & Banks: Analytics & Information RequirementDocument118 pagesRisk Management & Banks: Analytics & Information RequirementAbhishek KarekarNo ratings yet

- Operational Risk - The Challenge AheadDocument8 pagesOperational Risk - The Challenge AheadKeith WardenNo ratings yet

- Basel II PresentationDocument21 pagesBasel II PresentationMuhammad SaqibNo ratings yet

- R53 Global BaselIII v1 1Document16 pagesR53 Global BaselIII v1 1douglasNo ratings yet

- BaselDocument37 pagesBaselRohit BeheraNo ratings yet

- Commercial Bank Project: Annual Report 2018 Credit Libanais SAL & Bank of BeirutDocument10 pagesCommercial Bank Project: Annual Report 2018 Credit Libanais SAL & Bank of BeirutNaja NaddafNo ratings yet

- Group 4 CBM Bsel IIIDocument18 pagesGroup 4 CBM Bsel IIISourav PoddarNo ratings yet

- The Evolution To Basel II: Donald InscoeDocument45 pagesThe Evolution To Basel II: Donald InscoeKawneet BhasinNo ratings yet

- Financial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsFrom EverandFinancial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Colorfastness of Zippers To Light: Standard Test Method ForDocument2 pagesColorfastness of Zippers To Light: Standard Test Method ForShaker QaidiNo ratings yet

- Decision Trees For Management of An Avulsed Permanent ToothDocument2 pagesDecision Trees For Management of An Avulsed Permanent ToothAbhi ThakkarNo ratings yet

- Amendments To The PPDA Law: Execution of Works by Force AccountDocument2 pagesAmendments To The PPDA Law: Execution of Works by Force AccountIsmail A Ismail100% (1)

- Convection Transfer EquationsDocument9 pagesConvection Transfer EquationsA.N.M. Mominul Islam MukutNo ratings yet

- Guidelines For Prescription Drug Marketing in India-OPPIDocument23 pagesGuidelines For Prescription Drug Marketing in India-OPPINeelesh Bhandari100% (2)

- Hydro Electric Fire HistoryDocument3 pagesHydro Electric Fire HistorygdmurfNo ratings yet

- (Campus of Open Learning) University of Delhi Delhi-110007Document1 page(Campus of Open Learning) University of Delhi Delhi-110007Sahil Singh RanaNo ratings yet

- How To Convert Files To Binary FormatDocument1 pageHow To Convert Files To Binary FormatAhmed Riyadh100% (1)

- EKRP311 Vc-Jun2022Document3 pagesEKRP311 Vc-Jun2022dfmosesi78No ratings yet

- Chapter 4 - Basic ProbabilityDocument37 pagesChapter 4 - Basic Probabilitynadya shafirahNo ratings yet

- DION IMPACT 9102 SeriesDocument5 pagesDION IMPACT 9102 SeriesLENEEVERSONNo ratings yet

- 19c Upgrade Oracle Database Manually From 12C To 19CDocument26 pages19c Upgrade Oracle Database Manually From 12C To 19Cjanmarkowski23No ratings yet

- FpsecrashlogDocument19 pagesFpsecrashlogtim lokNo ratings yet

- Implications of A Distributed Environment Part 2Document38 pagesImplications of A Distributed Environment Part 2Joel wakhunguNo ratings yet

- Draft JV Agreement (La Mesa Gardens Condominiums - Amparo Property)Document13 pagesDraft JV Agreement (La Mesa Gardens Condominiums - Amparo Property)Patrick PenachosNo ratings yet

- Predator U7135 ManualDocument36 pagesPredator U7135 Manualr17g100% (1)

- Multimodal Essay FinalDocument8 pagesMultimodal Essay Finalapi-548929971No ratings yet

- The Privatization PolicyDocument14 pagesThe Privatization PolicyRIBLEN EDORINANo ratings yet

- Trade MarkDocument2 pagesTrade MarkRohit ThoratNo ratings yet

- DS Agile - Enm - C6pDocument358 pagesDS Agile - Enm - C6pABDERRAHMANE JAFNo ratings yet

- MSC-MEPC.2-Circ.17 - 2019 Guidelines For The Carriage of Blends OfBiofuels and Marpol Annex I Cargoes (Secretariat)Document4 pagesMSC-MEPC.2-Circ.17 - 2019 Guidelines For The Carriage of Blends OfBiofuels and Marpol Annex I Cargoes (Secretariat)DeepakNo ratings yet

- Satish Gujral - FinalDocument23 pagesSatish Gujral - Finalsatya madhuNo ratings yet

- Sankranthi PDFDocument39 pagesSankranthi PDFMaruthiNo ratings yet

- Artificial Intelligence Techniques For Encrypt Images Based On The Chaotic System Implemented On Field-Programmable Gate ArrayDocument10 pagesArtificial Intelligence Techniques For Encrypt Images Based On The Chaotic System Implemented On Field-Programmable Gate ArrayIAES IJAINo ratings yet

- Curriculum Guide Ay 2021-2022: Dr. Gloria Lacson Foundation Colleges, IncDocument9 pagesCurriculum Guide Ay 2021-2022: Dr. Gloria Lacson Foundation Colleges, IncJean Marie Itang GarciaNo ratings yet

- Jan 25th 6 TicketsDocument2 pagesJan 25th 6 TicketsMohan Raj VeerasamiNo ratings yet

- Editan - Living English (CD Book)Document92 pagesEditan - Living English (CD Book)M Luthfi Al QodryNo ratings yet

- Iphone and Ipad Development TU GrazDocument2 pagesIphone and Ipad Development TU GrazMartinNo ratings yet