NEGOTIATIONS, DEAL STRUCTURING & METHODS OF PAYMENTS

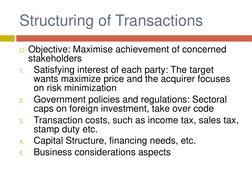

Structuring of Transactions

1.

2.

3.

4.

5.

Objective: Maximise achievement of concerned stakeholders Satisfying interest of each party: The target wants maximize price and the acquirer focuses on risk minimization Government policies and regulations: Sectoral caps on foreign investment, take over code Transaction costs, such as income tax, sales tax, stamp duty etc. Capital Structure, financing needs, etc. Business considerations aspects

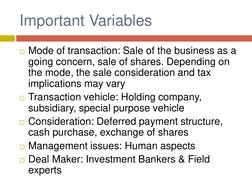

�Important Variables

Mode of transaction: Sale of the business as a going concern, sale of shares. Depending on the mode, the sale consideration and tax implications may vary Transaction vehicle: Holding company, subsidiary, special purpose vehicle Consideration: Deferred payment structure, cash purchase, exchange of shares Management issues: Human aspects Deal Maker: Investment Bankers & Field experts

�Regulatory Approvals

In US or EU, anti trust laws are very stringent. Requires approval from the Federal Trade Commission or the Department of Justice for any acquisition in US, EC for any target in EU. It also examines distortion in market competition. It even asks a company to divest if acquiring leads monopoly It dictates how employees are to be protected when ownership of company changes

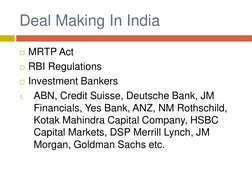

�Deal Making In India

1.

MRTP Act RBI Regulations Investment Bankers ABN, Credit Suisse, Deutsche Bank, JM Financials, Yes Bank, ANZ, NM Rothschild, Kotak Mahindra Capital Company, HSBC Capital Markets, DSP Merrill Lynch, JM Morgan, Goldman Sachs etc.

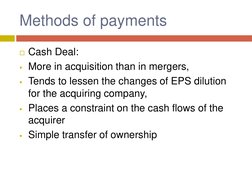

�Methods of payments

Cash Deal: More in acquisition than in mergers, Tends to lessen the changes of EPS dilution for the acquiring company, Places a constraint on the cash flows of the acquirer Simple transfer of ownership

�Methods of payments

Exchange of Shares: Financed by debt are called leveraged buyouts In some cases the shareholders of acquired company end up owning most of the acquired company Decline the EPS of the acquirer company

�Methods of payments

Hybrid: Combination of cash & debt, Cash & stock

�Factors affecting Choice of Payment

Accounting, tax aspects, financial strategy If bidder highly geared, taking a loan to pay for an acquisition is less attractive and share exchange is more lucrative Consider share exchange when acquirer considers their shares as overvalued. Risk is spread Consider Cash when transaction is plain & simple Deferred Payment Sharing of risk between acquirer and target

�Types of Exchange of Shares

Fixed Shares Fixed Value

��FUNDING OF ACQUISITIONS

�From the perspective of how the merge is financed, there are two types of mergers: purchase mergers and consolidation mergers. Each has certain implications for the companies involved and for investors: Purchase Mergers - As the name suggests, this kind of merger occurs when one company purchases another one. The purchase is made by cash or through the issue of some kind of debt instrument, and the sale is taxable. Acquiring companies often prefer this type of merger because it can provide them with a tax benefit. Acquired assets can be written-up to the actual purchase price, and the difference between book value and purchase price of the assets can depreciate annually, reducing taxes payable by the acquiring company Consolidation Mergers - With this merger, a brand new company is formed and both companies are bought and combined under the new entity. The tax terms are the same as those of a purchase merger.

�Methods for Effecting Payment of Consideration

The consideration for transfer of business may be discharged either through issue of shares (equity or preference) or other instruments of the transferee company or by cash. 1. By issue of equity shares of Acquirer Company 2. By issue of preference shares of Acquirer Company 3. By issue of secured debt instruments of Acquirer Company 4. By Payment in Cash 5. By any combination of the above

�Issue of equity shares of Acquirer Company Share Swap Method

Issues in using share swap method If the acquirer company is unlisted this method would not work Determination of the correct swap ratio in conformity with SEBI takeover regulations, commercially accepted to the tendering company and economical to the acquirer company.

�Issue of equity shares of Acquirer Company Share Swap Method

Issues in using share swap method The tendering company would accept shares instead of cash if the valuation of acquirer companys shares is substantially low than its intrinsic value to make additional gains as a reward for not accepting the cash. The tendering shareholders also expects that the value of the acquirer companys share considered for the swap ratio is at a significant discount to its current market price. Share swap method normally leads to making acquisitions more expensive for the acquiring company. Swap ratio is ideally a bull phase option

�Issue of equity shares of Acquirer Company Share Swap Method

Issues in using share swap method It leads to the dilution of EPS as also of the stake of the acquirer companys promoters in the acquirer company resulting in company market price nosediving due to issuing of additional equity or making the acquirer company vulnerable to the takeover. This method can be effectively used when one is acquiring a relatively much smaller company

�Issue of equity shares of Acquirer Company Share Swap Method

Issues in using share swap method Normally, before making an open offer, the acquirer company would either enter into a block deal (negotiated deal) with the target companys promoters or with an institutional shareholder or it would acquire shares from the stock market just below the trigger level of an open offer

The acquirer companys promoters would not prefer to issue a large chunk of their companys shares to the promoters of the target company

�Issue of equity shares of Acquirer Company Share Swap Method

Issues in using share swap method There is no exemption nor deferment available from payment of capital gains tax even if there is no cash consideration flowing from the acquirer to the tendering company shareholders in the pure swap method though available in other countries.

The tendering shareholders are forced to pay tax from their own pockets since they do not receive any cash which is not acceptable by many shareholders

�Issue of equity shares of Acquirer Company Share Swap Method

Issues in using share swap method Foreign retail shareholders have no appetite for the shares of an Indian company

�Issue of preference shares of Acquirer Company

SEBI takeover code do not allow issuance of preference shares in lieu of payment of consideration for shares acquired from the public during the course of an open offer However this prohibition does not apply in case of negotiated block deal entered into by the acquirer company with the existing promoters or institutional investors

�Issue of secured debt instruments of Acquirer Company

Chances of acceptance of secured debt instruments instead of cash would be better if the company resorts to differential pricing and also if debt instruments are listed on the stock exchanges Less possible if this debt instruments are not listed on the exchanges. However, the acquirer company can provide liquidity to them by having arrangements with banks or NBFC for granting loans against them or buying at a discounted rate

�Payment in Cash

Most favored method

�Sources of Funds For Equity

Internal Accruals Hindalco, entire cost of Rs.218.19 crore to acquire Indal M&M , Rs. 486.65 crore to acquire Punjab Tractors Ltd., Swaraj Automative Ltd. and Swaraj Engines Ltd. Jet acquisition of Air Sahara for Rs.1450 cr.

�Sources of Funds For Equity

IPO / FPO / Right Issues

Tata Motors right issue of Rs.4145cr for prepayment of part of the short term bridge loan availed by Jaguar Land Rover Ltd. Hindalco rights issue of Rs.5048 for repayment of bridge loan availed by AV Minerals (Netherlands) BV for acquisition of Novelis

�Sources of Funds For Equity

Private Placement / PE Funds ADR /GDR

�Sources of Funds Borrowed Funds

Banks and FIs

IDFC, HDFC requires mortgage of shares of the acquirer company as security. If stock market tanks.. Further shares are required as security. This can be sold in market on non repayment of loan on time thus increasing vulnerability of takeover.

ECB: not permitted in India

�Leveraged Buyouts

LBO means mobilizing borrowed funds based on the security of assets and cash flows of the target company (before the takeover) and using these funds to acquire the target company

�Leveraged Buyouts

Steps: 1. Incorporation of a privately/ wholly owned company to act as a special purpose vehicle (SPV) for acquisition of the target company. 2. Mobilization of borrowed funds in the SPV, based on the security of assets and cash flows of the target company (before its takeover) 3. Acquisition of the entire share capital of the target company. 4. Merger of the target company into the SPV. This last move has two effects: (1) It brings the assets of the target company and the loans taken by SPV into one balance sheet by which the lenders security no more remains a third party security. (2) It makes the target company go private, i.e. the target company gets unlisted.

�Management Buyouts

When the professional management or the nonpromoter management of the company carries out leveraged buyout of the company from its promoters, the same is called as management buyout or MBO