You might also like

- Fund. How To Finance An Independent Film.Document11 pagesFund. How To Finance An Independent Film.Buffalo 8100% (17)

- Film FinancingDocument60 pagesFilm Financingwasim100% (1)

- The Walt Disney Company Company AnalysisDocument16 pagesThe Walt Disney Company Company AnalysisSanjay BijaraniaNo ratings yet

- Challenges at Time Warner: Case StudyDocument31 pagesChallenges at Time Warner: Case StudyHoney HonNo ratings yet

- Film Financing Report ConsultingDocument20 pagesFilm Financing Report ConsultingDigendra Rathore100% (1)

- BoeingDocument49 pagesBoeinggallant rana100% (2)

- Walt Disney Strategic CaseDocument28 pagesWalt Disney Strategic CaseArleneCastroNo ratings yet

- Asset Disposal Form: A) To Be Completed by Department Head/Division HeadDocument2 pagesAsset Disposal Form: A) To Be Completed by Department Head/Division HeadPotchara KulNo ratings yet

- Brand Failures: Project byDocument58 pagesBrand Failures: Project bySharanya NarayananNo ratings yet

- Cineplex Group5Document10 pagesCineplex Group5Tarun Gupta100% (1)

- Venture Capital and Credit RatingDocument25 pagesVenture Capital and Credit RatingMinhaz AlamNo ratings yet

- Facility Layout of CocaDocument19 pagesFacility Layout of CocaJagmohan Bisht100% (2)

- Analysis of The Walt Disney CompanyDocument15 pagesAnalysis of The Walt Disney CompanygimbrinelNo ratings yet

- Roku Investment TeaserDocument4 pagesRoku Investment TeaserTruman LauNo ratings yet

- Case Study of New Blockbuster ImageDocument5 pagesCase Study of New Blockbuster ImageSayantanKandar100% (1)

- Edited - Iron Ore Supply Contract and Sales AgreementDocument12 pagesEdited - Iron Ore Supply Contract and Sales AgreementSaid SayreNo ratings yet

- Selected Key Terms For Institutions and AudiencesDocument7 pagesSelected Key Terms For Institutions and AudiencesRFrearsonNo ratings yet

- High-Profit IPO Strategies: Finding Breakout IPOs for Investors and TradersFrom EverandHigh-Profit IPO Strategies: Finding Breakout IPOs for Investors and TradersNo ratings yet

- A New Blockbuster ImageDocument8 pagesA New Blockbuster ImageDescartes ArrezaNo ratings yet

- SWOT Analysis of PRAN Food LimitedDocument2 pagesSWOT Analysis of PRAN Food Limitedreza006475% (4)

- Ott PlatformDocument26 pagesOtt Platformaparnanayar05No ratings yet

- Tgs Kelompok Best BuyDocument10 pagesTgs Kelompok Best BuyLiana ReginaNo ratings yet

- Cineplex Group12Document6 pagesCineplex Group12Keerthi PurushothamanNo ratings yet

- OTT Business Opportunities: Streaming TV, Advertising, TV Apps, Social TV, and tCommerceFrom EverandOTT Business Opportunities: Streaming TV, Advertising, TV Apps, Social TV, and tCommerceNo ratings yet

- Tivo Case Analysis: A. Swot Analysis StrengthDocument4 pagesTivo Case Analysis: A. Swot Analysis StrengthAfshin SalehianNo ratings yet

- TiVo Case Study Analysis - Group 2Document13 pagesTiVo Case Study Analysis - Group 2Parang MehtaNo ratings yet

- Viacom Stahl ReportDocument19 pagesViacom Stahl ReportmattdoughNo ratings yet

- Warner BrothersDocument18 pagesWarner BrothersMahendar SdNo ratings yet

- Viacom PowerPoint PresentationDocument20 pagesViacom PowerPoint PresentationbizdaywebNo ratings yet

- CIEE Contemporary Television #5Document20 pagesCIEE Contemporary Television #5Jonathan KeyNo ratings yet

- Blockbuster 111Document57 pagesBlockbuster 111Kourosh ShNo ratings yet

- TiVo Case AnalysisDocument5 pagesTiVo Case Analysisabhi1385100% (2)

- Tivo Case Analysis BulletsDocument4 pagesTivo Case Analysis BulletsyellowbirdhnNo ratings yet

- G322 Film Industry RevisionDocument17 pagesG322 Film Industry RevisionAndy MurphyNo ratings yet

- Product Placement POV DocumentDocument3 pagesProduct Placement POV DocumentTom SaunterNo ratings yet

- Walt Disney Company 2015-05-13Document20 pagesWalt Disney Company 2015-05-13Fredrik StenkilNo ratings yet

- Marketing PlanDocument11 pagesMarketing PlanleopiyaNo ratings yet

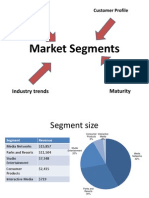

- Market Segments - GautamDocument5 pagesMarket Segments - GautamGautam SchaanNo ratings yet

- Aaj Tak' News Channel's Success StoryDocument17 pagesAaj Tak' News Channel's Success StoryManu MalavNo ratings yet

- Introduction To Brightcove The Promise of Internet TV Internet TV Businesses Brightcove Overview Product Demonstration Questions & AnswersDocument19 pagesIntroduction To Brightcove The Promise of Internet TV Internet TV Businesses Brightcove Overview Product Demonstration Questions & Answersdwitting2693No ratings yet

- First Research Industry Profile - Motion Picture Production and DistributionDocument14 pagesFirst Research Industry Profile - Motion Picture Production and DistributionVictoria YampolskyNo ratings yet

- Internet Media & OTT PPT by Kagan 2017-11-2Document17 pagesInternet Media & OTT PPT by Kagan 2017-11-2mattdoughNo ratings yet

- British Film IndustryDocument177 pagesBritish Film IndustryEmily BowersNo ratings yet

- Media EconomicsDocument30 pagesMedia EconomicsSukaran ThakurNo ratings yet

- Zenith: Marketing Research For High Definition Television (HDTV)Document13 pagesZenith: Marketing Research For High Definition Television (HDTV)Bhavik NasitNo ratings yet

- HMVDocument7 pagesHMVSsam KRayNo ratings yet

- Q4 2008 State of The IndustryDocument7 pagesQ4 2008 State of The IndustrysergiubirisNo ratings yet

- Television Media & Its Impact On Business ManagementDocument19 pagesTelevision Media & Its Impact On Business ManagementV Satya DeepakNo ratings yet

- Perceptual Mapping Lecture17Document20 pagesPerceptual Mapping Lecture17shalsak100% (3)

- SLM Nov 2000power Point Investor PresentationDocument17 pagesSLM Nov 2000power Point Investor Presentationstanleemedia1No ratings yet

- IPO Paper Week5 Scott BarnesDocument7 pagesIPO Paper Week5 Scott BarnessdbarnesNo ratings yet

- Netflix ManagementDocument6 pagesNetflix ManagementCarina MariaNo ratings yet

- Digital Dawn A Revolution in Movie DistributionDocument32 pagesDigital Dawn A Revolution in Movie DistributionRomdhi Fatkhur RoziNo ratings yet

- StratMan 8thed Ch3 2017 Webtext FinalDocument32 pagesStratMan 8thed Ch3 2017 Webtext FinalReyn CebuNo ratings yet

- Overview of AOLDocument14 pagesOverview of AOLTaqbir TalhaNo ratings yet

- Sony Bravia Marketing PlanDocument22 pagesSony Bravia Marketing PlanShafiullah Shawn100% (2)

- Global Advertising EffectivenessDocument21 pagesGlobal Advertising EffectivenessMunish Nagar100% (1)

- N T P P: EW Rends IN Roduct LacementDocument21 pagesN T P P: EW Rends IN Roduct Lacementmalikrocks3436No ratings yet

- SonyDocument21 pagesSonyNeha UpadhyayNo ratings yet

- Opera + AdcolonyDocument12 pagesOpera + Adcolonycarlyblack2006No ratings yet

- Best Buy Team PresentationDocument10 pagesBest Buy Team PresentationSandra Medina-CortesNo ratings yet

- Waltdisney2 PPT CrdownloadDocument33 pagesWaltdisney2 PPT CrdownloadRaman ManchandaNo ratings yet

- Netflix EnriquezDocument4 pagesNetflix EnriquezJoshua ReyesNo ratings yet

- Sales Presentation - Consumer DurablesDocument50 pagesSales Presentation - Consumer DurablesdrifterdriverNo ratings yet

- Pepsi Cola Company: Click To Edit Master Subtitle StyleDocument24 pagesPepsi Cola Company: Click To Edit Master Subtitle StyleArjay DascoNo ratings yet

- NPD & Product MixDocument24 pagesNPD & Product MixArpit ChauhanNo ratings yet

- Capital Budgeting Techniques Data AnalysisDocument6 pagesCapital Budgeting Techniques Data AnalysisMani KandanNo ratings yet

- Introduction To Operations ManagementDocument11 pagesIntroduction To Operations ManagementAnamul NadimNo ratings yet

- Brief History of Estee LauderDocument2 pagesBrief History of Estee Lauderzeshan_secNo ratings yet

- Closed PTW AuditDocument1 pageClosed PTW Auditf.BNo ratings yet

- 1 Annex I. Imprimatur Investment Agreement: Example Offer Letter, Key Terms and Outline ProcessDocument5 pages1 Annex I. Imprimatur Investment Agreement: Example Offer Letter, Key Terms and Outline ProcessAfandie Van WhyNo ratings yet

- Excel Hotel Data (Conjoint)Document13 pagesExcel Hotel Data (Conjoint)bhavinkapoorNo ratings yet

- U.S. Customs Form: CBP Form 3347A - Declaration of Consignee When Entry Is Made by An AgentDocument2 pagesU.S. Customs Form: CBP Form 3347A - Declaration of Consignee When Entry Is Made by An AgentCustoms FormsNo ratings yet

- 10 Examples of LinkedIn Ads That Totally Crushed It - LinkedIn Marketing Blog PDFDocument6 pages10 Examples of LinkedIn Ads That Totally Crushed It - LinkedIn Marketing Blog PDFSonakshi GargNo ratings yet

- Impact of Credit Risk Management On Financial Performance of Commercial Banks of PakistanDocument15 pagesImpact of Credit Risk Management On Financial Performance of Commercial Banks of PakistanSaifullahJaspalNo ratings yet

- Total Lock & Security, Inc., D/b/a The Door Switch v. Door Control ServicesDocument6 pagesTotal Lock & Security, Inc., D/b/a The Door Switch v. Door Control ServicesPriorSmartNo ratings yet

- TI India - PPT - Oct 12Document60 pagesTI India - PPT - Oct 12vishmittNo ratings yet

- Sevilla Trading Co vs. SemanaDocument1 pageSevilla Trading Co vs. Semanaida_chua8023No ratings yet

- Luxury Fusionwear at Citrine, KolkataDocument36 pagesLuxury Fusionwear at Citrine, KolkataCitrine KolkataNo ratings yet

- Mpa SwotDocument14 pagesMpa Swotkylexian1No ratings yet

- Amzn PM 30 190127175213Document4 pagesAmzn PM 30 190127175213ipsita pandaNo ratings yet

- Profile of The Chatime FounderDocument1 pageProfile of The Chatime FounderWinnee NgNo ratings yet

- Las Bambas No Podrá Continuar Con La Producción de Cobre A Partir Del 18 de DiciembreDocument1 pageLas Bambas No Podrá Continuar Con La Producción de Cobre A Partir Del 18 de DiciembrePaola Villar SNo ratings yet

- Balveer Singh PDFDocument2 pagesBalveer Singh PDFsunilNo ratings yet

- 1 - Sub Activity 2 GuidelinesDocument4 pages1 - Sub Activity 2 Guidelinessir BryanNo ratings yet

- JAIBB SyllabusDocument7 pagesJAIBB SyllabuszubishuNo ratings yet

- Internship ReportDocument57 pagesInternship ReportNoufal Km92% (12)

- Final Project Report of HRMDocument41 pagesFinal Project Report of HRMFatima RazzaqNo ratings yet