Financial Accounting 2

(BM020-3-1)

Control Accounts

�Learning Outcomes

To define control accounts

The purpose of control accounts.

The main types of control accounts.

BM020-3-1-Financial Accounting 2

Slide 1 of 13

�Uses of Control Accounts

A control account is so called because it controls a

section of the ledger.

For example, a sales ledger control account controls

the sales ledger; a purchase ledger controls the

purchase ledger.

If there is a difference on the trial balance, the control

accounts will show whether or not any of the

difference is in the sales or purchase ledgers.

Control accounts are kept in the general ledger.

BM020-3-1-Financial Accounting 2

�Purpose of Control accounts

To act as independent checks on the arithmetical

accuracy of the balances in the sales and purchase

ledgers.

An added advantage of keeping control accounts in

that they can act as mini trial balances, since they

are summary accounts.

To identify ledgers in which errors have been made

when there is a difference on a trial balance.

BM020-3-1-Financial Accounting 2

�Purpose of Control accounts (cont)

To act as an independent internal check

on the work of the sales & purchase

ledger clerks, to detect errors or fraud.

Duties should be divided where the person

keeping the sales or purchase ledgers will

not have access to the control account in

the general ledger.

BM020-3-1-Financial Accounting 2

Slide 1 of 13

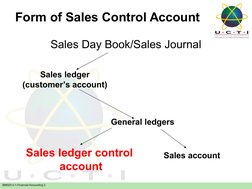

�Form of Sales Control Account

Sales Day Book/Sales Journal

Sales ledger

(customers account)

General ledgers

Sales ledger control

account

BM020-3-1-Financial Accounting 2

Sales account

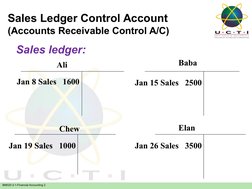

�Sales Ledger Control Account

(Accounts Receivable Control A/C)

Sales ledger:

Ali

Jan 8 Sales 1600

Chew

Jan 19 Sales 1000

BM020-3-1-Financial Accounting 2

Baba

Jan 15 Sales 2500

Elan

Jan 26 Sales 3500

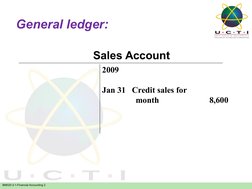

�General ledger:

Sales Account

2009

Jan 31 Credit sales for

month

BM020-3-1-Financial Accounting 2

8,600

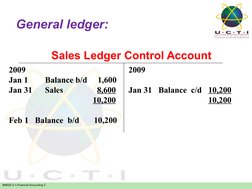

�General ledger:

Sales Ledger Control Account

2009

Jan 1

Jan 31

2009

Balance b/d

Sales

Feb 1 Balance b/d

BM020-3-1-Financial Accounting 2

1,600

8,600

10,200

10,200

Jan 31 Balance c/d 10,200

10,200

�Sales Ledger Control

2009

Jan 1

Balance b/d

xxxx

Jan 31 Sales day book

xxxxx

(total of sales invoiced in the

period

xxxxx

BM020-3-1-Financial Accounting 2

2009

Jan 31

Returns inwards Day Book

(total of all goods returned from

debtors in the period)

xxx

Jan 31

Cash book

xxx

(total of all cash received from

debtors in the period)

Jan 31

Cash book

xxx

(total of all cheques received from

debtors in the period)

Jan 31

Balance c/d

xxx

xxxxx

�Example 1 of Sales ledger control account data:

Debit balances on 1 January 2009

Total credit sales for the month

Cheques received from customers in the month

Cash received from customers in the month

Returns inwards from customers during the month

Debit balances on 31 January as extracted

from the sales ledger

Sales ledger control

BM020-3-1-Financial Accounting 2

1,894

10,290

7,284

1,236

296

3,368

�Example 1 of Sales ledger control account data:

Debit balances on 1 January 2009

Total credit sales for the month

Cheques received from customers in the month

Cash received from customers in the month

Returns inwards from customers during the month

Debit balances on 31 January as extracted

from the sales ledger

1,894

10,290

7,284

1,236

296

3,368

Sales ledger control

2009

Jan 1 Balances b/d

Jan 31 Sales

1,894

10,290

12,184

BM020-3-1-Financial Accounting 2

2009

Jan 31

Jan 31

Jan 31

Jan 31

Bank

7,284

Cash

1,236

Return Inwards 296

Balances c/d

3,368

12,184

�Information for sales ledger

control account

Exhibit 2.1 Source of information for sales ledger control account

BM020-3-1-Financial Accounting 2

�Form of Purchase Control Account

Purchase Day Book/Purchase Journal

Purchase ledger

(creditors account)

General ledgers

Purchases Ledger control

account

BM020-3-1-Financial Accounting 2

Purchases account

�Purchase Ledger control account

The total accounts payable account is

also referred to as the Purchase ledger

control account

The credit balance in this account in the

general ledger must always be equal to

the total of the credit balances of the

individual creditors accounts in the

purchases ledger at a particular point in

time.

BM020-3-1-Financial Accounting 2

�Purchase Ledger Control Account

Purchase ledger:

Sow

Jan 3 Purchases 1,500

Rama

Jan 18 Purchases 10,000

BM020-3-1-Financial Accounting 2

Bob

Jan 10 Purchases 4,500

Tom

Jan 21 Purchases 4,000

�General ledger

Purchase Ledger control account

20X9

Jan 31

Balance c/d

23,000

20X9

Jan 1 Balance b/d

Jan 31 Purchases

23,000

Purchases account

Jan 31 Sundry creditors

BM020-3-1-Financial Accounting 2

23,000

3,000

20,000

23,000

�Information for purchases

ledger control account

Exhibit 2.2 Source of information for purchases ledger control account

BM020-3-1-Financial Accounting 2

�Question and Answer Session

Q&A

BM020-3-1-Financial Accounting 2

Slide 1 of 13

�Exercise

Frank Wood & Alan Sangster (2008)

Business Accounting 1, Eleventh edition,

Prentice Hall.

31.2A, 31.4A, 31.7A, 31.8A (pg 380 382)

BM020-3-1-Financial Accounting 2

Slide 1 of 13

�What we will cover next

Errors and Adjustment

BM020-3-1-Financial Accounting 2

Slide 1 of 13