1

�Plan Cost

Management

Control

Costs

Estimate Costs

Determine

Budget

�IAMPI 2014 pto

�INPUT

TOOLS &

TECHNIQUES

OUTPUT

�INPUTS

TOOLS &

TECHNIQUES

OUTPUTS

�10

�11

�Cost estimate:

Costs are estimated for all resources that will be charged to the project

(ex: labor, materials, equipment, services, and facilities, inflation, cost of

financing, contingency costs, etc)

Include the identification and consideration of costing alternatives to

initiate and complete the project

A quantitative assessment of the likely costs for resources required to

complete the activity.

A prediction that is based on the information known at a given point in

time

Generally expressed in units of some currency

Should be reviewed and refined during the course of the project to reflect

additional detail as it becomes available and assumptions are tested

The accuracy of a project estimate will increase as the project progresses

through the project life cycle

12

�IAMPI 2014 pto

13

�14

�15

�Tahapan proyek, tipe estimasi dan metode

estimasi

16

�17

�18

�IAMPI 2014 pto

19

�20

� W.B.S BANGUNAN GEDUNG

Project

BANGUNAN

GEDUNG

PERSIAPAN

Sub Project

FONDASI

SubNetwork

Activity

STRUKTUR

BAWAH

STRUKTUR

ATAS

STRUKTUR

BETON

PELAT

KOLOM

FINISHING

STRUKTUR

BAJA

BALOK

MACHANICAL

ELEKTRICAL

� W.B.S BANGUNAN GEDUNG

Activity

BALOK

Sub Activity

BEKISTING

Resources

Material

Breakdown

PEMBETONAN

TENAGA KERJA

PC

MATERIAL

PASIR

PEMBESIAN

PERALATAN

KERIKIL

�IAMPI 2014 pto

23

�Faktor

Indikator

Lokasi

Kondisi perekonomian setempat, Aksesibilitas Daya Dukung

Tanah, Zonasi Gempa, Topografi, dll

Desain

Total Luas Lantai , Ketinggian Gedung, Jumlah Lantai, Jarak

antar Lantai, Panjang Keliling, Bentuk Bangunan, dll

Kualitas Bangunan

Tipe Penutup Lantai, Plafond, Finishing Dinding, Material Pintu &

jendela

Konstruksi

Kelengkapan Dokumen saat ditender, tipe Tender & Kontrak,

sistim pembayaran, metode konstruksi

Waktu

Tahun pembangunan, Durasi, Inflasi

24

�INPUT

TOOLS &

TECHNIQUES

OUTPUT

25

�26

�27

�28

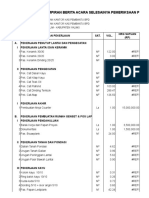

�Anggaran Biaya Langsung

Anggaran biaya langsung untuk pelaksanaan harus

Kontraktor

dirinci untuk keperluan operasional :

Upah

: terdiri dari pek. Galian, timbunan, pasangan,

cor beton, penulangan, form work, dst

Material : terdiri dari material beton, pasir, bata,

batu kali, semen, kayu, tegel, dst

Alat

: terdiri dari depresiasi, bbm / pelumas,

perbaikan, alat sewa, dst .

Subkon : terdiri dari subkon A , subkon B, dst .

Persiapan : terdiri dari pek. Basecamp , jalan kerja ,

dewatering , dst

Overhead: terdiri dari gaji pegawai , honor , dst

� Rincian Anggaran Biaya Upah

No

Jenis Pekerjaan

1.

2.

3.

4.

5.

6.

7.

8

9.

Galian

Timbunan

Pas. Batu kali

Pas. Batu bata

Beton bertulang

Lantai

Kuda-Kuda

Penutup Atap

Dst

Total Biaya Upah

Satuan

Pek.

M3

M3

M3

M2

M3

M2

M3

M2

Harga

Satuan

Pek

(Rp)

Kuantitas pekerjaan

Fondasi

Struktur

Finish-ing

Jumlah

Jumlah

Harga

( Rp )

� Rincian Anggaran Biaya Bahan

No

Jenis Pekerjaan

1.

2.

3.

4.

5.

6.

7.

8

9.

Galian

Timbunan

Pas. Batu kali

Pas. Batu bata

Beton bertulang

Lantai

Kuda-Kuda

Penutup Atap

Dst

Satuan

Pek.

M3

M3

M3

M2

M3

M2

M3

M2

Jumlah

Harga

satuan

Jumlah Harga

Jenis dan Kuantitas bahan

Seme

n

Pasir

Bt.

kali

Bt

Bata

Besi

beton

Kayu

Tege

l

Ds

t

� Rincian Anggaran Biaya Material

Satuan

No

Jenis Material

1.

2.

3.

4.

5.

6.

7.

8

9.

Semen

Batu Kali

Pasir

Batu pecah

Batu Bata

Tegel

Kayu

Kosen

Dst

Harga

Satuan

(Rp)

Kuantitas material

Fondasi

Struktur

Finish

-ing

Zak

M3

M3

M3

bh

bh

M3

M3

Total Biaya Material

Jumlah

Jumlah

Harga

( Rp )

� Rincian Anggaran Biaya Alat

No Jenis Alat

1.

2.

3.

4.

5.

6.

Jam Harga

oper Sewa

asi

Alat Sendiri

BBM

Oli

Perba

ikan

Mob/

De- Jumlah

mob

Buldozer

Excavator

T. Crane

D. Truck

Pompa

Dst

Jumlah biaya Alat

� Rincian Anggaran Biaya Subkontraktor

No

Jenis

Pekerjaan

1.

2.

3.

4.

5.

6.

7.

8

9.

Galian

Timbunan

Pas. Batu kali

Pas. Batu

bata

Beton

bertulang

Lantai

Kuda-Kuda

Penutup Atap

Dst

Jumlah

Vol.

Pek

.

Budget

Pek (Rp)

Subkon A

Vol.

pek

Harga

Subkon

Sbkon B

Vol.

pek

Harga

Subkon

�Kel.

Sub.Kel

Rekap Cost Budget

Kontraktor

PEMBEBANAN

Rp.

Keterangan

BIAYA LANGSUNG PROYEK

II.

1.

BAHAN / MATERIAL

2.

UPAH

3.

ALAT

4.

SUBKONTRAK

5.

PERSIAPAN / PENYELESAIAN

6.

OVERHEAD LAPANGAN

SUB TOTAL

KEWAJIBAN PAJAK

III

1.

PPN ( 10% )

2.

PPH

SUB TOTAL

BIAYA TIDAK LANGSUNG

IV

1.

OVERHEAD PUSAT / CABANG/ PERW.

2.

PENYUSUSTAN AKTIVA TETAP

SDUB TOTAL

LABA / RUGI PROYEK

TOTAL

35

� KODE PEMBUKUAN (CONTROL ACCOUNT)

Secara keseluruhan semua bukti transaksi

dibukukan dan diberikan peng-kode-an

Tidak ada standar dlm pemberian kode,

setiap Perusahaan dapat membuat sendiri.

Contoh untuk bahasan peng-kode-an, sbb:

Kode Kelompok

Pendapatan :

I

Biaya Langsung :

II

Pajak :

III

Biaya tidak langsung

:

IV

� KODE UNSUR BIAYA LANGSUNG

Dari contoh bahasan diatas, kode biaya langsung (II) dirinci lagi menjadi, subkelompok:

Jenis Biaya

Kode Subkelompok

(1) Biaya bahan

II . 1

(2) Biaya Upah

II . 2

(3) Biaya Alat

II . 3

(4) Biaya Subkon

II . 4

(5) Biaya Pers/Penyel.

II . 5

(6) Biaya Overhead Lap. :

II . 6

� KODE JENIS TIAP UNSUR B.L

Untuk keperluan tindakan dari Management,

diperlukan kode jenis dari tiap subkelompok

(1) Kode Sub kelompok Bahan ( II . 1 )

- Semen

: II . 1 . 1

- Pasir

: II . 1 . 2

- Batu pecah

: II . 1 . 3

- Besi beton

: II . 1 . 4

- Dan seterusnya

: II . 1 . n

�INPUT

TOOLS &

TECHNIQUES

OUTPUT

39

�40

�41

�42

�43

�Konsep Earned Value

Term

Definition

Planned Value (PV)

Akumulasi anggaran biaya yang dialokasikan berdasarkan

rencana kerja yang telah disusun terhadap waktu

Actual Cost (AC)

Realisasi akumulasi biaya aktual yang telah dikeluarkan untuk

penyelesaian pekerjaan menurut laporan keuangan dalam

periode tertentu

Earned Value (EV)

Akumulasi dari progres pekerjaan yang diekspresikan

berdasarkan budget yang dialokasikan untuk melaksanakan

pekerjaan

Cost Variance (CV) =

EV - AC

Ukuran kinerja biaya berdasarkan selisih antara nilai EV - AC

Schedule Variance (SV)

= EV - PV

Ukuran kinerja waktu berdasarkan selisih antara nilai EV - PV

Cost Performance

Index (CPI) = EV/AC

Ukuran efisiensi biaya dari sumberdaya yang dialokasikan

berdasarkan rasio EV/AC

Schedule Performance

Index (SPI) = EV/PV

Ukuran efisiensi waktu berdasarkan rasio EV/AC

44

�Performance Measure

45

�Forecasting

Term

Definition

Budget At Completion

(BAC)

Adalah total PV untuk menyelesaikan seluruh pekerjaan

Estimate At Completion

(EAC)

Total biaya yang diperlukan untuk meyelesaikan seluruh

pekerjaan yang diekspresikan sebagai total biaya aktual sampai

dengan saat ini dan estimasi untuk menyelesaikan

EAC = BAC/CPI

EAC Alt 1, If the CPI is expected to be the same for the

remainder of the project

EAC = AC + BAC EV

EAC Alt 2, If future work will be accomplished at the planned

rate

EAC = AC + Bottom-up

ETC

EAC Alt 3, If the initial plan is no longer valid

EAC = AC + [(BAC

EV)/(CPI x SPI)]

EAC Alt 4, If both the CPI and SPI influence the remaining work

ECD = Actual Time +

(Planned Time Actual

Time)/SPI

Estimate Completion Date

46

�Earned Value: Graphical

Representation

47

�CASE STUDY: Hasil Monitoring Proyek Akhir

Bulan ke 3

Kegiatan

Anggaran

Biaya

Realisasi

Biaya

4000

5000

3000

3000

6000

4000

5000

2500

8000

1000

Kegiatan sdh dilaksanakan

Kegiatan belum dilaksanakan

�Earned Value Analysis

Term

Value

Planned Value (PV)

14.000

Actual Cost (AC)

15.500

Earned Value (EV)

11.000

Cost Variance (CV) = EV - AC

-4.500

Schedule Variance (SV) = EV - PV

-3.000

Cost Performance Index (CPI) = EV/AC

0,709 < 1

Schedule Performance Index (SPI) = EV/PV

0,786 < 1

Budget At Completion (BAC)

26.000

BAC = 4000 + 3000 + 6000 + 5000 + 8000 = 26.000

PV = 4000 + 3000 + (4/8)x(6000) + (4/10)x(5000) + (2/8)x(8000) = 14.000

EV = 4000+ (5/6)x(3000)+(2/8)x(6000)+(6/10)x(5000)+(0/8)x(8000) =

11.000

AC = 5000 + 3000 + 4000 + 2500 + 1000 =15.500

49

�Forecasting

Term

Definition

Value

EAC = BAC/CPI

EAC Alt 1, If the CPI is expected to be the

same for the remainder of the project

36.671

EAC = AC + BAC EV

EAC Alt 2, If future work will be

accomplished at the planned rate

30.500

EAC = AC + Bottom-up

ETC

EAC Alt 3, If the initial plan is no longer

valid, and new estimate for remaining work

15.500 +

20.000 (est) =

35.500

EAC = AC + [(BAC EV)/

(CPI x SPI)]

EAC Alt 4, If both the CPI and SPI influence

the remaining work

42.417

ECD = Actual Time +

(Remaining Time)/SPI

Estimate Completion Date

6,82 months

Pelaksanaan pekerjaan terlambat dan realisasi biaya melebihi

anggaran

Range EAC = 30.500 sd 42.417

ECD = 6.82 months

50

�Projected

Slippage

GRAFIK EARNED VALUE

Reporting

Cut Off Date

31200

28600

Projected

Overrun

26000

23400

AC

20800

18200

PV

15600

13000

10400

7800

EV

5200

2600

0

6

6.82

51

�MEKANISME COST CONTROL

COST

BUDGET

PENGADAAN &

KONSTRUKSI

REALISASI

BIAYA

TINDAKAN

PERBAIKAN

ANALISIS

PENYIMPANGAN.

SESUAI

BUDGET

EVALUASI

BIAYA

DOKUMENTASI

OVER

BUDGET

�Referensi:

1.Project Management Institute (PMI), A Guide to project

Management Body Of Knowledge, PMBOK Guide 5th Edition, 2013

2.Ikatan Ahli Manajemen Proyek Indonesia (IAMPI), Pelatihan

Sertifikasi Manajemen Proyek, Materi Project Cost Management,

2014

3.Asiyanto, MBA, IPM, Ir, Construction Project Cost Management",

PT. Pradnya Paramita Jakarta, 2005.

4.DellIsola, M.D., Architects Essentials of Cost Management,

John Wiley & Sons Inc, 2002

53

�Terima Kasih

54