You might also like

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Corporate FinanceDocument96 pagesCorporate FinanceRohit Kumar80% (5)

- Can Shareholders File Derivative Suits for Corporate Wrongdoing? (35 charactersDocument1 pageCan Shareholders File Derivative Suits for Corporate Wrongdoing? (35 charactersCoco NavarroNo ratings yet

- Chapter 4, AccountingDocument13 pagesChapter 4, AccountingIyadAitHou100% (1)

- A Simple and Reliable Way To Compute Option-Based Risk-Neutral DistributionsDocument42 pagesA Simple and Reliable Way To Compute Option-Based Risk-Neutral Distributionsalanpicard2303No ratings yet

- Wisdom of Intelligent Investors Safal Niveshak Jan. 2018Document40 pagesWisdom of Intelligent Investors Safal Niveshak Jan. 2018Sagar KondaNo ratings yet

- The Term Structure of Interest Rates: Denitsa StefanovaDocument41 pagesThe Term Structure of Interest Rates: Denitsa StefanovathofkampNo ratings yet

- Chapter 2 - AnswerDocument4 pagesChapter 2 - Answerwynellamae80% (5)

- Cutting Edge Dividend AdjustmentDocument2 pagesCutting Edge Dividend AdjustmentVeeken Chaglassian100% (1)

- Quanto Lecture NoteDocument77 pagesQuanto Lecture NoteTze Shao100% (1)

- The Greeks FinanceDocument49 pagesThe Greeks FinanceGerardo Rafael GonzalezNo ratings yet

- Options - ValuationDocument37 pagesOptions - Valuationashu khetanNo ratings yet

- Risk and ReturnDocument43 pagesRisk and ReturnAbubakar OthmanNo ratings yet

- Value at Risk FinalDocument27 pagesValue at Risk FinalAnu BumraNo ratings yet

- CH 5 MARKET RISK - VaRDocument29 pagesCH 5 MARKET RISK - VaRAisyah Vira AmandaNo ratings yet

- Detecting Breakouts From Flags & PennantsDocument9 pagesDetecting Breakouts From Flags & PennantsdrkwngNo ratings yet

- LBO CaseDocument10 pagesLBO Caseneo123120% (1)

- MOS 3311 Final NotesDocument33 pagesMOS 3311 Final Notesshakuntala12321No ratings yet

- Madsen PedersenDocument23 pagesMadsen PedersenWong XianyangNo ratings yet

- Black Scholes ModelDocument10 pagesBlack Scholes ModelSaumya GoelNo ratings yet

- MAFS Topic 1Document151 pagesMAFS Topic 1Bass1237No ratings yet

- Financial Engineering PresentationDocument32 pagesFinancial Engineering PresentationsunnyshocksNo ratings yet

- Event Study Analysis: CLM Chapter 4Document18 pagesEvent Study Analysis: CLM Chapter 4Alexandre FavreNo ratings yet

- Calculating the Black-Scholes Option ValueDocument3 pagesCalculating the Black-Scholes Option ValueVivek SinghNo ratings yet

- DM9 CirculationDocument60 pagesDM9 CirculationNaman JainNo ratings yet

- Chapter 6Document46 pagesChapter 6Quynh Trang DinhNo ratings yet

- Chapter-10 Return & RiskDocument19 pagesChapter-10 Return & Riskaparajita promaNo ratings yet

- Risk Analysis in Capital BudgetingDocument70 pagesRisk Analysis in Capital BudgetingdhavalshahicNo ratings yet

- Risk+Return NTDocument43 pagesRisk+Return NTRana HaiderNo ratings yet

- Pragya: The Best FRM Revision Course!Document18 pagesPragya: The Best FRM Revision Course!mohamedNo ratings yet

- Risk and Return IntroductionDocument18 pagesRisk and Return IntroductionjahanzebNo ratings yet

- Ch03-5 Portifolio Theory - Risk Return AnalysisDocument113 pagesCh03-5 Portifolio Theory - Risk Return AnalysismupiwamasimbaNo ratings yet

- Pricing Model For A Credit-Linked Note On A CDX TrancheDocument6 pagesPricing Model For A Credit-Linked Note On A CDX TranchechertokNo ratings yet

- Robust Hedging in Incomplete Markets: Maastricht UniversityDocument16 pagesRobust Hedging in Incomplete Markets: Maastricht UniversityDmitri StepanovNo ratings yet

- TH BL K TH BL KSHL MDL SHL MDL The Black The Black - Scholes Model Scholes ModelDocument7 pagesTH BL K TH BL KSHL MDL SHL MDL The Black The Black - Scholes Model Scholes ModelPrashantKumarNo ratings yet

- Risky Asset Valuation and The Efficient Market Hypothesis: Susan Thomas IGIDR, BombayDocument42 pagesRisky Asset Valuation and The Efficient Market Hypothesis: Susan Thomas IGIDR, BombayrexkingdomNo ratings yet

- Risk and Return - : For 9.220, Term 1, 2002/03 02 - Lecture12.ppt Student VersionDocument18 pagesRisk and Return - : For 9.220, Term 1, 2002/03 02 - Lecture12.ppt Student VersionShakeelaNo ratings yet

- Comparison of VaR Approaches on Stock PortfolioDocument10 pagesComparison of VaR Approaches on Stock Portfolioraj_gargiNo ratings yet

- CFA - 2 & 3. Quantitative MethodDocument22 pagesCFA - 2 & 3. Quantitative MethodChan Kwok WanNo ratings yet

- Risk & Return An Overview of Capital Market TheoryDocument20 pagesRisk & Return An Overview of Capital Market TheoryVaishnav KumarNo ratings yet

- Financial Decision-Making Under UncertaintyDocument18 pagesFinancial Decision-Making Under UncertaintyMateo PulidoNo ratings yet

- Risk and Return For PrintDocument30 pagesRisk and Return For PrintTahir DestaNo ratings yet

- FINS 2624 Tutorial Week 3 SlidesDocument12 pagesFINS 2624 Tutorial Week 3 SlidesWahaaj RanaNo ratings yet

- 8.risk and ReturnDocument26 pages8.risk and ReturnJorge Luis Astudillo ArévaloNo ratings yet

- AFM Formula SheetDocument15 pagesAFM Formula Sheetganesh bhaiNo ratings yet

- Chapter 8Document29 pagesChapter 8jgau0017No ratings yet

- Hedging Barriers: Comparing StrategiesDocument27 pagesHedging Barriers: Comparing StrategiesXu ZhengpingNo ratings yet

- BSMODELDocument20 pagesBSMODELkal74No ratings yet

- Financial Derivatives: Section 5Document38 pagesFinancial Derivatives: Section 5palpakratwr9030No ratings yet

- Chapter Seven Analysis of Derivative SecuritiesDocument25 pagesChapter Seven Analysis of Derivative Securitiesbiniyam zelekeNo ratings yet

- Long-Horizon Investing in A Non-CAPM World: Christopher Polk Dimitri Vayanos Paul WoolleyDocument42 pagesLong-Horizon Investing in A Non-CAPM World: Christopher Polk Dimitri Vayanos Paul WoolleyTom HardyNo ratings yet

- Module 6.1: EAY and Compounding Frequency: The Number of Compounding Periods Per YearDocument162 pagesModule 6.1: EAY and Compounding Frequency: The Number of Compounding Periods Per Year乐冰莹No ratings yet

- Portfolio ManagementDocument50 pagesPortfolio ManagementmamunimamaNo ratings yet

- Vol 2 Issue 1 ExternalDocument5 pagesVol 2 Issue 1 ExternalNikolas JNo ratings yet

- Chapter 3: Risk Analysis: 3.1 Introduction: What Is Risk?Document4 pagesChapter 3: Risk Analysis: 3.1 Introduction: What Is Risk?Pravin ThoratNo ratings yet

- Métodos Cuantitativos: Alex Contreras MirandaDocument23 pagesMétodos Cuantitativos: Alex Contreras MirandaRafael BustamanteNo ratings yet

- Portfolio Management ProcessDocument21 pagesPortfolio Management ProcessAksaya CaNo ratings yet

- Combinepdf PDFDocument65 pagesCombinepdf PDFCam SpaNo ratings yet

- Short Note VP AtolityDocument12 pagesShort Note VP AtolityceikitNo ratings yet

- International Financial Management PgapteDocument35 pagesInternational Financial Management PgapterameshmbaNo ratings yet

- CH 04 RevisedDocument20 pagesCH 04 RevisedPrakash PandeyNo ratings yet

- Lecture 4 Risk Aversion and Capital Allocation To Risky AssetsDocument20 pagesLecture 4 Risk Aversion and Capital Allocation To Risky AssetsLuisLoNo ratings yet

- Risk and Return TheoryDocument45 pagesRisk and Return Theoryanshika rathoreNo ratings yet

- International Accounting IssuesDocument29 pagesInternational Accounting IssuesHetal GadhviNo ratings yet

- Commercial Law 2020 SyllabusDocument36 pagesCommercial Law 2020 SyllabusVanessa MuzonesNo ratings yet

- Ceat Balance SheetDocument2 pagesCeat Balance Sheetkcr kc100% (2)

- UK Company Law Case Law Lists 2017Document25 pagesUK Company Law Case Law Lists 2017Ryan WongNo ratings yet

- Vouching & Verification: Ms. Fleur Dsouza Asst. Prof., BMS SIES CollegeDocument44 pagesVouching & Verification: Ms. Fleur Dsouza Asst. Prof., BMS SIES Collegesagar kasalkarNo ratings yet

- 6 Options Trading Mistakes To Avoid - Tips To Save You Time, Money and Frustration by Bryan PerryDocument3 pages6 Options Trading Mistakes To Avoid - Tips To Save You Time, Money and Frustration by Bryan PerryAndrew ChanNo ratings yet

- Virtual Stock Trading Journal: in Partial Fulfilment of The RequirementsDocument13 pagesVirtual Stock Trading Journal: in Partial Fulfilment of The RequirementsIrahq Yarte TorrejosNo ratings yet

- Application For PAN Through Online Services: Tax Information NetworkDocument6 pagesApplication For PAN Through Online Services: Tax Information NetworkGaurav GuptaNo ratings yet

- Subsequent Acquisition PDFDocument21 pagesSubsequent Acquisition PDFEvangeline WongNo ratings yet

- Convergence Black-Scholes To BinomialDocument9 pagesConvergence Black-Scholes To BinomialLuis Hernandez100% (1)

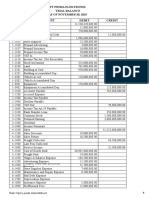

- PT PRIMA ELEKTRONIK TRIAL BALANCEDocument21 pagesPT PRIMA ELEKTRONIK TRIAL BALANCENadyaNo ratings yet

- Forward Rate and Future Spot Rate RelationshipDocument20 pagesForward Rate and Future Spot Rate Relationshipveronica100% (1)

- The Influence of Investment Knowledge, Perceived Risk and Perceived Behavioral Control Towards Tock Investment IntentionDocument12 pagesThe Influence of Investment Knowledge, Perceived Risk and Perceived Behavioral Control Towards Tock Investment IntentionInternational Journal of Business Marketing and ManagementNo ratings yet

- Adani Ports and Sez Economic Zone Companyname: Strong Quarter Encouraging GuidanceDocument13 pagesAdani Ports and Sez Economic Zone Companyname: Strong Quarter Encouraging GuidanceAmey TiwariNo ratings yet

- Unit 2 Assignment Managing Financial Resources & Decisions SamDocument9 pagesUnit 2 Assignment Managing Financial Resources & Decisions SamBenNo ratings yet

- Numerical Methods for Valuing Financial DerivativesDocument111 pagesNumerical Methods for Valuing Financial DerivativesFarhan SarwarNo ratings yet

- Chapter 06, Modern Advanced Accounting-Review Q & ExrDocument33 pagesChapter 06, Modern Advanced Accounting-Review Q & Exrrlg481488% (16)

- HLA Venture Income Fund Jan 22Document3 pagesHLA Venture Income Fund Jan 22ivyNo ratings yet

- A Study On Performance Evaluation of Select Textile Companies An Empirical Analysis'Document5 pagesA Study On Performance Evaluation of Select Textile Companies An Empirical Analysis'mohan ksNo ratings yet

- FS TypesDocument23 pagesFS TypesAnamika VermaNo ratings yet

- Capital MarketDocument14 pagesCapital MarketVikash kumarNo ratings yet

- SPCL Ncba and SBD CasesDocument115 pagesSPCL Ncba and SBD Casesjhen agustinNo ratings yet

- Accountancy - Class XII SQP (2019-20Document8 pagesAccountancy - Class XII SQP (2019-20Inder Singh NegiNo ratings yet

- Corpo QuizDocument4 pagesCorpo QuizMotu PropioNo ratings yet