You might also like

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Income Tax Act - 1961Document37 pagesIncome Tax Act - 1961Aniket KottalagiNo ratings yet

- Taxable Income RahulDocument18 pagesTaxable Income RahulRahul ParitNo ratings yet

- Income Tax, IndiaDocument11 pagesIncome Tax, Indiahimanshu_mathur88No ratings yet

- Chapter 1 1 CotxaDocument27 pagesChapter 1 1 Cotxafs5kxrcn2gNo ratings yet

- Direct Tax CodeDocument17 pagesDirect Tax CodeRashmi RathoreNo ratings yet

- Topic 4-Income Tax Act-Imposition of Income TaxDocument35 pagesTopic 4-Income Tax Act-Imposition of Income TaxDeus MalimaNo ratings yet

- CE22 - 14 - After Tax Economic AnalysisDocument50 pagesCE22 - 14 - After Tax Economic AnalysisNina MabantaNo ratings yet

- TAX MGT PPT 1Document28 pagesTAX MGT PPT 1Rahul DesaiNo ratings yet

- Direct & Indirect TaxesDocument33 pagesDirect & Indirect Taxesdinanikarim50% (2)

- 61a38d5c7b74a - INcome Tax and ETA HandwrittenDocument15 pages61a38d5c7b74a - INcome Tax and ETA HandwrittenAnuska ThapaNo ratings yet

- E Filing Income Tax Return OnlineDocument53 pagesE Filing Income Tax Return OnlineMd MisbahNo ratings yet

- Income Tax Law and Practice: Bba - 5 Sem BBA - 301Document39 pagesIncome Tax Law and Practice: Bba - 5 Sem BBA - 301Aarti Dhanrajani HaswaniNo ratings yet

- Income Tax Law & Practice-Lesson - 1 To 12Document250 pagesIncome Tax Law & Practice-Lesson - 1 To 12Space ResearchNo ratings yet

- Eco SeminarDocument17 pagesEco SeminarPavan GowdaNo ratings yet

- IncomeTax MaterialDocument91 pagesIncomeTax MaterialSandeep JaiswalNo ratings yet

- DTC - FinalDocument18 pagesDTC - FinalvjranavjNo ratings yet

- Direct Taxes Code Bill, 2009: at A GlanceDocument181 pagesDirect Taxes Code Bill, 2009: at A GlanceSanni KumarNo ratings yet

- MidTerm Lesson Part 1Document34 pagesMidTerm Lesson Part 1ARMAN WAYNE ANGELESNo ratings yet

- Income and Withholding Taxes-2015Document132 pagesIncome and Withholding Taxes-2015Elaine Llarina-RojoNo ratings yet

- L.B and TaxationDocument18 pagesL.B and TaxationHasnain RazaNo ratings yet

- Income Tax - 4 NewDocument42 pagesIncome Tax - 4 Newrehan87100% (2)

- 7th Term - Legal Frameworks of ConstructionDocument79 pages7th Term - Legal Frameworks of ConstructionShreedharNo ratings yet

- Income Tax Law and It's Computation Sandeep KumarDocument33 pagesIncome Tax Law and It's Computation Sandeep KumarThe PaletteNo ratings yet

- Direct and Indirect Tax: Submitted byDocument41 pagesDirect and Indirect Tax: Submitted bylakshyaNo ratings yet

- Nature and Concept: OF IncomeDocument193 pagesNature and Concept: OF IncomeFranchise AlienNo ratings yet

- 4 17113 Taxation II 2013Document181 pages4 17113 Taxation II 2013Sudhanshu DubeyNo ratings yet

- BBA - ITLP - Unit - 1 (Part - 1)Document47 pagesBBA - ITLP - Unit - 1 (Part - 1)Ishvinder Singh KalraNo ratings yet

- Income and Tax AuthorityDocument21 pagesIncome and Tax AuthorityRatul HaqueNo ratings yet

- Indian Taxation SystemDocument15 pagesIndian Taxation SystemassatputeNo ratings yet

- Direct Tax CodeDocument10 pagesDirect Tax Codejgaurav80No ratings yet

- Corporate Income Taxes and Tax RatesDocument38 pagesCorporate Income Taxes and Tax RatesShaheen ShahNo ratings yet

- U 5 TaxDocument23 pagesU 5 TaxfsafwfNo ratings yet

- INCOME TAX ReviewDocument54 pagesINCOME TAX ReviewKeepy FamadorNo ratings yet

- Income Tax in India - Wikipedia, The Free EncyclopediaDocument10 pagesIncome Tax in India - Wikipedia, The Free EncyclopediakandurimaruthiNo ratings yet

- TaxDocument4 pagesTaximoymitoNo ratings yet

- Direct TaxesDocument139 pagesDirect TaxesjahnavibodapatiNo ratings yet

- 24 Income Tax GuideDocument7 pages24 Income Tax GuidePiyush KumarNo ratings yet

- Taxes: Tax StructureDocument14 pagesTaxes: Tax StructurePradeep NairNo ratings yet

- Corporate Tax Planning: Unit IDocument20 pagesCorporate Tax Planning: Unit ILavanya KasettyNo ratings yet

- Tax Theory GuideDocument14 pagesTax Theory GuideBrair Mugishabrair2No ratings yet

- Income Tax SynopsisDocument24 pagesIncome Tax SynopsisSupreet KaurNo ratings yet

- Project Topic: Income Tax Systems in Pakistan, India & UKDocument53 pagesProject Topic: Income Tax Systems in Pakistan, India & UKAfzal RocksxNo ratings yet

- Tax CLASS NOTESDocument17 pagesTax CLASS NOTESAks SinhaNo ratings yet

- ItlpDocument14 pagesItlpA_saravanavelNo ratings yet

- Basic Concepts of Taxation03Document26 pagesBasic Concepts of Taxation03Jan Mohammad BalochNo ratings yet

- Module 2Document54 pagesModule 2Aryaman BhauwalaNo ratings yet

- Hari Income Tax Department - Do CXDocument12 pagesHari Income Tax Department - Do CXNelluri Surendhar ChowdaryNo ratings yet

- Worksheet 5 q2 TaxationDocument15 pagesWorksheet 5 q2 TaxationAllan TaripeNo ratings yet

- Income TaxDocument156 pagesIncome TaxApoorv90% (10)

- E Filing Income Tax Return OnlineDocument45 pagesE Filing Income Tax Return OnlineAyush MishraNo ratings yet

- Lecture 1 - Introduction To Income TaxDocument27 pagesLecture 1 - Introduction To Income TaxMimi kupiNo ratings yet

- 2012 Lesson 20 Withholding TaxDocument16 pages2012 Lesson 20 Withholding TaxDan MichaelNo ratings yet

- The Conceptual Basis of Personal Income Tax, Classification of Income, Tax RatesDocument29 pagesThe Conceptual Basis of Personal Income Tax, Classification of Income, Tax RatesgunayNo ratings yet

- SEMINAR ON TAXATION-PACSB-Part2Document66 pagesSEMINAR ON TAXATION-PACSB-Part2Sherbs SolisNo ratings yet

- Introduction To Income TaxDocument80 pagesIntroduction To Income Taxkana lahotiNo ratings yet

- Definition of Income Tax: FinanceDocument10 pagesDefinition of Income Tax: FinanceStXvrNo ratings yet

- 01 Important DefinitionsDocument7 pages01 Important DefinitionsmijjinNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- 2019-0443 - Osorio, Pauline - II-12 - ACED 18 - Reinforcement 4Document3 pages2019-0443 - Osorio, Pauline - II-12 - ACED 18 - Reinforcement 4Keddy GorospeNo ratings yet

- Income Taxation Outline and CasesDocument7 pagesIncome Taxation Outline and CasesChicklet ArponNo ratings yet

- Excel Practice Problems PDFDocument6 pagesExcel Practice Problems PDFAnand HaraniNo ratings yet

- (Batch:PCB2) Mrunal's Economy Pillar#2B: Budget Revenue 15 FC, Black Money, Subsidies Page 273Document44 pages(Batch:PCB2) Mrunal's Economy Pillar#2B: Budget Revenue 15 FC, Black Money, Subsidies Page 273lakshay singlaNo ratings yet

- Taxation Suggested SolutionsDocument3 pagesTaxation Suggested SolutionsSteven Mark MananguNo ratings yet

- Solutions For GST Question BankDocument55 pagesSolutions For GST Question BankVarun VardhanNo ratings yet

- JB Depo - Shutteing Centering Material QuoteDocument5 pagesJB Depo - Shutteing Centering Material Quoteanamika.advaitNo ratings yet

- Cir VS PLDTDocument1 pageCir VS PLDTKling KingNo ratings yet

- CIR V. TRANSITIONS OPTICAL PHILIPPINES, INC. (G.R. No. 227544, November 22, 2017)Document2 pagesCIR V. TRANSITIONS OPTICAL PHILIPPINES, INC. (G.R. No. 227544, November 22, 2017)Digna LausNo ratings yet

- CATOS InvoiceDocument2 pagesCATOS InvoicesowntharyagbmNo ratings yet

- 2014-15 Douglas County Secured Assessment RollDocument97 pages2014-15 Douglas County Secured Assessment RollcvalleytimesNo ratings yet

- Court of Tax AppealsDocument47 pagesCourt of Tax AppealsLady Paul SyNo ratings yet

- Amendments To IFRS 2 'Share-Based Payment'Document1 pageAmendments To IFRS 2 'Share-Based Payment'Rizshelle D. AlarconNo ratings yet

- Nput Vat On Mixed TransactionsDocument15 pagesNput Vat On Mixed TransactionsBSACCBLK1COLEEN CALUGAYNo ratings yet

- Ram Pal SinghDocument1 pageRam Pal SinghSACHIN MATHURNo ratings yet

- BOC Tax ComputationDocument2 pagesBOC Tax ComputationRom100% (1)

- 3.3 Exercise Key AnswerDocument2 pages3.3 Exercise Key AnswerKHAkadsbdhsgNo ratings yet

- Hilado vs. CIRDocument1 pageHilado vs. CIRAlan GultiaNo ratings yet

- Prudential SurrenderDocument5 pagesPrudential SurrenderBriltex IndustriesNo ratings yet

- Nippon Express vs. CIR 185666Document1 pageNippon Express vs. CIR 185666magenNo ratings yet

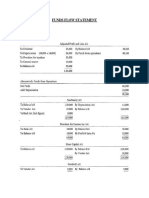

- Funds Flow Statement: Numerical 1Document4 pagesFunds Flow Statement: Numerical 1Neelu AhluwaliaNo ratings yet

- Obillos, Jr. vs. Cir - 139 Scra 436Document4 pagesObillos, Jr. vs. Cir - 139 Scra 436Ygh E SargeNo ratings yet

- Payslip August 2021Document2 pagesPayslip August 2021Sidharth Chettri100% (1)

- 26.hilado Vs CIRDocument4 pages26.hilado Vs CIRClyde KitongNo ratings yet

- Tax Residence TutorialDocument11 pagesTax Residence TutorialHazlina HusseinNo ratings yet

- A3 - Trading-Settlement-Guidelines-Manila-Electric-Company-Fixed-Rate-Putable-Bonds-Due-2020-and-2025Document2 pagesA3 - Trading-Settlement-Guidelines-Manila-Electric-Company-Fixed-Rate-Putable-Bonds-Due-2020-and-2025Pia Shannen OdinNo ratings yet

- Accounting For Income TaxationDocument8 pagesAccounting For Income Taxationangelian bagadiongNo ratings yet

- Income TaxationDocument28 pagesIncome TaxationHi HelloNo ratings yet

- (See Rule 11, 11E) Electronic Return Under The Maharashtra State Tax On Professions, Trades, Callings and Employments Act, 1975Document3 pages(See Rule 11, 11E) Electronic Return Under The Maharashtra State Tax On Professions, Trades, Callings and Employments Act, 1975Gabbar SinghNo ratings yet

- Daftar Akun PT AlamandaDocument4 pagesDaftar Akun PT AlamandaWigit Marseto AdjiNo ratings yet