You might also like

- Pathoma LectureDocument385 pagesPathoma LectureMustafa Thaier Al-Karaghouli91% (22)

- Bank Statement Template 27Document2 pagesBank Statement Template 27mohamed elmakhzni100% (1)

- Tax Equity and Canons ExplainedDocument25 pagesTax Equity and Canons ExplainedyebegashetNo ratings yet

- Slides VAT 2Document24 pagesSlides VAT 2yebegashetNo ratings yet

- Data Extract From World Development IndicatorsDocument21 pagesData Extract From World Development IndicatorspappiadityaNo ratings yet

- Countingup Statement 2023 07Document1 pageCountingup Statement 2023 07SophiaNo ratings yet

- Wise & Co., Inc. vs. Meer G.R. No. 48231. June 30, 1947Document3 pagesWise & Co., Inc. vs. Meer G.R. No. 48231. June 30, 1947Natasha MilitarNo ratings yet

- Chapter 19 - Taxes On Consumption and Wealth: by RashmiDocument39 pagesChapter 19 - Taxes On Consumption and Wealth: by RashmirashmimgrNo ratings yet

- Chapter 19 - Taxes On Consumption and Wealth: Public EconomicsDocument39 pagesChapter 19 - Taxes On Consumption and Wealth: Public Economics9211420420No ratings yet

- Taxation: Definition and Explanation Miss Rabia Asad Iqra University IslamabadDocument18 pagesTaxation: Definition and Explanation Miss Rabia Asad Iqra University IslamabadSaif Ur RehmanNo ratings yet

- Lecture 2 - Taxation and Public SpendingDocument34 pagesLecture 2 - Taxation and Public SpendingAmelia BaileyNo ratings yet

- Sher QTYhistoryDocument45 pagesSher QTYhistorySherwIn BeltRanNo ratings yet

- Taxation and Government Intervention: Mark Jayson C. Agarin Dyrick Marl M. Mata Sherwin N. BeltranqtyDocument45 pagesTaxation and Government Intervention: Mark Jayson C. Agarin Dyrick Marl M. Mata Sherwin N. BeltranqtySherwIn BeltRanNo ratings yet

- Lecture Notes - PEconomics IIDocument112 pagesLecture Notes - PEconomics IIAmelia BaileyNo ratings yet

- 01 Chap 14 RosenDocument64 pages01 Chap 14 RosenSagar ChowdhuryNo ratings yet

- Chapter Three: General Overview of TaxationDocument68 pagesChapter Three: General Overview of TaxationWagner AdugnaNo ratings yet

- SESSION 11 and 12 Edited (2)Document15 pagesSESSION 11 and 12 Edited (2)moyaseenali13No ratings yet

- Comparative Taxation: Some Basic PointsDocument17 pagesComparative Taxation: Some Basic Pointshaidersh05No ratings yet

- Taxation Efficiency and International TradeDocument14 pagesTaxation Efficiency and International TradeSamia Irshad ullahNo ratings yet

- Taxation and Government Intervention On The BusinessDocument33 pagesTaxation and Government Intervention On The Businessjosh mukwendaNo ratings yet

- Public Finance Reporting. 1.2Document44 pagesPublic Finance Reporting. 1.2Axel Jhon FabayosNo ratings yet

- Fiscal PolicyDocument16 pagesFiscal PolicymoosasuphiNo ratings yet

- Corporate Tax Rates Guide: An Overview of Global Tax SystemsDocument56 pagesCorporate Tax Rates Guide: An Overview of Global Tax SystemsKundan PrasadNo ratings yet

- IntroductionDocument30 pagesIntroductionSeifu BekeleNo ratings yet

- Chapter 3 Taxation OverviewDocument24 pagesChapter 3 Taxation OvervieweNo ratings yet

- Malaysian Taxation System: An OverviewDocument13 pagesMalaysian Taxation System: An OverviewSelva Bavani SelwaduraiNo ratings yet

- Corporate Taxation: Bachelor of Accounts and Finance CT 307Document32 pagesCorporate Taxation: Bachelor of Accounts and Finance CT 307YashKoNo ratings yet

- Taxation: Compulsory Transfer of Money From Individuals, Groups or Institutions To The Government Indirect BenefitsDocument21 pagesTaxation: Compulsory Transfer of Money From Individuals, Groups or Institutions To The Government Indirect BenefitsDavid AntwiNo ratings yet

- Chapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013Document32 pagesChapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013melsun007No ratings yet

- Introduction To Business TaxesDocument40 pagesIntroduction To Business TaxesLenil SanchezNo ratings yet

- Screenshot 2022-11-01 at 10.51.07 AMDocument75 pagesScreenshot 2022-11-01 at 10.51.07 AMsNo ratings yet

- CH 1Document14 pagesCH 1Taha Wael QandeelNo ratings yet

- 1 Introduction To Tax Law and PracticeDocument47 pages1 Introduction To Tax Law and PracticePanashe MachekepfuNo ratings yet

- Part II Tax Systems and TaxesDocument86 pagesPart II Tax Systems and Taxesjohn accaNo ratings yet

- Types of Taxes and The Jurisdictions That Use ThemDocument21 pagesTypes of Taxes and The Jurisdictions That Use ThemheobenicerNo ratings yet

- Prog: Bscac Level: 2.2: Year: 2016Document137 pagesProg: Bscac Level: 2.2: Year: 2016Zic Zac100% (1)

- Understanding the Economic Effects of TaxesDocument41 pagesUnderstanding the Economic Effects of TaxesAhmed MahmoudNo ratings yet

- 17.01.2020, 2. S.V.Kasi Visweswara Rao Sir, Joint Commissioner (ST), Introduction and Evolution of Indirect Taxation in IndiaDocument30 pages17.01.2020, 2. S.V.Kasi Visweswara Rao Sir, Joint Commissioner (ST), Introduction and Evolution of Indirect Taxation in IndiaMANAN KOTHARINo ratings yet

- Taxation: Concept, Nature and Characteristics of Taxation and TaxesDocument11 pagesTaxation: Concept, Nature and Characteristics of Taxation and TaxesMohammad FaizanNo ratings yet

- Group 6 Tax AssignmentDocument16 pagesGroup 6 Tax AssignmentFolake DavisNo ratings yet

- Introduction To Value Added Tax - VatDocument16 pagesIntroduction To Value Added Tax - VatAnand SubramanianNo ratings yet

- PDF Document 2Document7 pagesPDF Document 2Nafas NafasNo ratings yet

- Vat PresentationDocument7 pagesVat PresentationVarun KatochNo ratings yet

- FP (Taxation) Supplementary NotesDocument34 pagesFP (Taxation) Supplementary NotesAmy LiuNo ratings yet

- Unit 3 - Revenue ManagementDocument79 pagesUnit 3 - Revenue ManagementKimberly AsanteNo ratings yet

- Taxation LawDocument94 pagesTaxation LawspandanaNo ratings yet

- Public Finance CH 2Document30 pagesPublic Finance CH 2kussia toramaNo ratings yet

- Theme 8 - Taxation and Tax Theory: Public EconomicsDocument75 pagesTheme 8 - Taxation and Tax Theory: Public EconomicskumarbcomcaNo ratings yet

- Tax Law and Practice 1: AC405Document20 pagesTax Law and Practice 1: AC405ernest libertyNo ratings yet

- Global Tax ManagementDocument28 pagesGlobal Tax ManagementMai LiênNo ratings yet

- Lecture-1-An Overview of TaxationDocument14 pagesLecture-1-An Overview of TaxationJaved AnwarNo ratings yet

- TAXATION: GOVERNMENT REVENUE SOURCEDocument30 pagesTAXATION: GOVERNMENT REVENUE SOURCEKaneki KenNo ratings yet

- Taxation Science Introduction Lession 1Document17 pagesTaxation Science Introduction Lession 1chandyNo ratings yet

- Taxation Overview: Objectives, Principles and CharacteristicsDocument29 pagesTaxation Overview: Objectives, Principles and CharacteristicsJaved AnwarNo ratings yet

- Topic-1-An Overview of TaxationDocument29 pagesTopic-1-An Overview of TaxationJaved AnwarNo ratings yet

- Tax Incidence and the Efficiency Cost of TaxationDocument79 pagesTax Incidence and the Efficiency Cost of TaxationNeelabh KumarNo ratings yet

- Lecture 1: An Overview of Taxation: Faculty of Management and Tourism Spring 2020Document45 pagesLecture 1: An Overview of Taxation: Faculty of Management and Tourism Spring 2020Thu ThủyNo ratings yet

- Chapter 1 Bttax BanggawanDocument21 pagesChapter 1 Bttax Banggawanlaythejoylunas21No ratings yet

- Taxes-Direct and IndirectDocument11 pagesTaxes-Direct and IndirectTeguade ChekolNo ratings yet

- Definition of Taxation and Its Key ConceptsDocument16 pagesDefinition of Taxation and Its Key ConceptsMd. Rayhanul IslamNo ratings yet

- Chapter 4 Income Tax. PRT 1Document38 pagesChapter 4 Income Tax. PRT 1Girlie Kaye Onongen PagtamaNo ratings yet

- Lec 9 Fiscal Policy TaxationDocument36 pagesLec 9 Fiscal Policy Taxationdua tanveerNo ratings yet

- 5.1 Taxation IssuesDocument21 pages5.1 Taxation IssuesFranco FungoNo ratings yet

- GST Presentation Explains India's Upcoming Tax ReformDocument44 pagesGST Presentation Explains India's Upcoming Tax ReformAlimehdi MukadamNo ratings yet

- Tax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024From EverandTax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024No ratings yet

- Data QuillDocument3 pagesData QuillpappiadityaNo ratings yet

- StubHub, Inc. v. Ticketmaster L.L.C. Et AlDocument3 pagesStubHub, Inc. v. Ticketmaster L.L.C. Et AlpappiadityaNo ratings yet

- Conflict and Conflict ResolutionDocument18 pagesConflict and Conflict ResolutionpappiadityaNo ratings yet

- MKTG522 Course Project V2Document8 pagesMKTG522 Course Project V2pappiadityaNo ratings yet

- Week 6 Case AnalysisDocument6 pagesWeek 6 Case AnalysispappiadityaNo ratings yet

- Case Analysis WeekDocument6 pagesCase Analysis WeekpappiadityaNo ratings yet

- AmazonDocument2 pagesAmazonpappiadityaNo ratings yet

- Week 4 Case AnalysisDocument5 pagesWeek 4 Case AnalysispappiadityaNo ratings yet

- 2017 Financial Wellness Essay CollectionDocument66 pages2017 Financial Wellness Essay CollectionpappiadityaNo ratings yet

- ACCT500 Week 6 Homework RubricDocument3 pagesACCT500 Week 6 Homework RubricpappiadityaNo ratings yet

- ACCT500 - Week 5 Problem SetDocument2 pagesACCT500 - Week 5 Problem SetpappiadityaNo ratings yet

- ACCT500 Week 6 Homework RubricDocument3 pagesACCT500 Week 6 Homework RubricpappiadityaNo ratings yet

- Math 533 Course Project A2Document7 pagesMath 533 Course Project A2Megan W.No ratings yet

- 1.1 - Efficient Studying HandoutDocument12 pages1.1 - Efficient Studying HandoutpappiadityaNo ratings yet

- The Key Principles of Economics: Chapter SummaryDocument16 pagesThe Key Principles of Economics: Chapter SummaryPham Ba DatNo ratings yet

- Changes To USMLE 2014-2015 Handout FINALDocument2 pagesChanges To USMLE 2014-2015 Handout FINALFadHil Zuhri LubisNo ratings yet

- Log Book Daily Work DoneDocument5 pagesLog Book Daily Work DoneGhulam MustufaNo ratings yet

- A Solution For Indian GST Implementation For Simple Procurement Scenario Using TAXINN - SAP Blogs PDFDocument11 pagesA Solution For Indian GST Implementation For Simple Procurement Scenario Using TAXINN - SAP Blogs PDFPankaj KumarNo ratings yet

- TUA Income Tax Course SyllabusDocument5 pagesTUA Income Tax Course SyllabusFerdinand Caralde Narciso ImportadoNo ratings yet

- CIMB BANK Products and Services PresentationDocument20 pagesCIMB BANK Products and Services PresentationAzwin YusoffNo ratings yet

- Atal Pension Yojana (Apy) - Subscriber Registration FormDocument1 pageAtal Pension Yojana (Apy) - Subscriber Registration FormpraveenaNo ratings yet

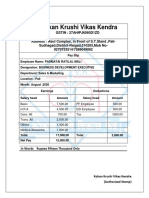

- Kokan Krushi Vikas Kendra pay slips August to October 2020Document3 pagesKokan Krushi Vikas Kendra pay slips August to October 2020DevenNo ratings yet

- Sad (1X20) PDFDocument3 pagesSad (1X20) PDFHarrenNo ratings yet

- 2017Document2 pages2017Trisha AmorantoNo ratings yet

- Transparency Documentation enDocument24 pagesTransparency Documentation enAditya SharmaNo ratings yet

- Deposit Trading Bonus Scheme Terms & ConditionsDocument31 pagesDeposit Trading Bonus Scheme Terms & Conditionsmohammadsameni1No ratings yet

- 1492614489586DTphtGkVh2SIRKEn PDFDocument4 pages1492614489586DTphtGkVh2SIRKEn PDFSaurabh Kumar SharmaNo ratings yet

- CustomerInvoice 1811454087 PDFDocument1 pageCustomerInvoice 1811454087 PDFkrishna kumarNo ratings yet

- ACC 430 Chapter 10Document20 pagesACC 430 Chapter 10vikkiNo ratings yet

- Renewal Premium Acknowledgement: Policy DetailsDocument1 pageRenewal Premium Acknowledgement: Policy DetailsTejpal Singh ShekhawatNo ratings yet

- Bharat Sanchar Nigam Limited: (A Govt. of India Enterprise)Document2 pagesBharat Sanchar Nigam Limited: (A Govt. of India Enterprise)Jinto JacobNo ratings yet

- Please DocuSign Uton Lawrence - PDF Uton LawrDocument5 pagesPlease DocuSign Uton Lawrence - PDF Uton LawrRelax NationNo ratings yet

- TAXXXXDocument2 pagesTAXXXXKeigrah Adelaine Gamban Pangilinan0% (1)

- Choose Australian Super Nomination FormDocument1 pageChoose Australian Super Nomination FormHomerKhanNo ratings yet

- Online Payment - Passport SevaDocument2 pagesOnline Payment - Passport SevaAbdul Hakeem Semar KamaluddinNo ratings yet

- 03 27 21Document18 pages03 27 21버니 모지코No ratings yet

- Chapter 6 Cash OriginalDocument11 pagesChapter 6 Cash OriginalNRKNo ratings yet

- OD115901213625804000Document1 pageOD115901213625804000adiNo ratings yet

- Solved Shonda Owns 1 000 of The 1 500 Shares Outstanding in RookDocument1 pageSolved Shonda Owns 1 000 of The 1 500 Shares Outstanding in RookAnbu jaromiaNo ratings yet

- 5 6073471622155600005 PDFDocument235 pages5 6073471622155600005 PDFRajni GouranaNo ratings yet

- Legal Fees - CKHTDocument2 pagesLegal Fees - CKHTChe TaNo ratings yet

- Essential Characteristics of TaxDocument5 pagesEssential Characteristics of TaxCristel BerindesNo ratings yet

- SIDBI Sammelan 2023Document1 pageSIDBI Sammelan 2023assmexellenceNo ratings yet