You might also like

- Accounting CycleDocument18 pagesAccounting CycleLeslie Sparks100% (8)

- Plant QRQC FormDocument1 pagePlant QRQC FormJordi Palomar100% (5)

- Applied Economics Week 3-4Document10 pagesApplied Economics Week 3-4MOST SUBSCRIBER WITHOUT A VIDEO100% (1)

- Applied Economics Periodical ExamDocument5 pagesApplied Economics Periodical ExamFrancaise Agnes Mascariña100% (1)

- LUYONG - 3rd Monthly Test Draft - FABM 1Document4 pagesLUYONG - 3rd Monthly Test Draft - FABM 1Jonavi LuyongNo ratings yet

- Basic Analysis of Demand and Supply 1Document6 pagesBasic Analysis of Demand and Supply 1Jasmine GarciaNo ratings yet

- Computer Vision With Python Cookbook PDFDocument208 pagesComputer Vision With Python Cookbook PDFNevin DeshpandeNo ratings yet

- Abm 1Document3 pagesAbm 1Dindin Oromedlav LoricaNo ratings yet

- (Applied Econ.) Module 4. - Introduction To Applied EconomicsDocument5 pages(Applied Econ.) Module 4. - Introduction To Applied Economicsrowena marambaNo ratings yet

- BusinessMath LAS Q1 Wk3Document10 pagesBusinessMath LAS Q1 Wk3Janna GunioNo ratings yet

- Applied Economics SHSDocument42 pagesApplied Economics SHSIgnatians Santa Rosa0% (1)

- Business Finance Final ExamDocument4 pagesBusiness Finance Final ExamLee Dumalaga CarinanNo ratings yet

- Grade 11 Business Math Sample Questions PDFDocument8 pagesGrade 11 Business Math Sample Questions PDFCherie LeeNo ratings yet

- Applied Economics Power PointDocument213 pagesApplied Economics Power Pointjonathan malasigNo ratings yet

- Applied EconomicsDocument5 pagesApplied EconomicsMhayAnne Perez88% (17)

- 1 Introduction To Applied EconomicsDocument23 pages1 Introduction To Applied EconomicsJonard OrcinoNo ratings yet

- ABM 2 SummativeDocument3 pagesABM 2 SummativeDindin Oromedlav LoricaNo ratings yet

- Applied Economics in Relation To Philippine Economic ProblemsDocument15 pagesApplied Economics in Relation To Philippine Economic ProblemsAnaliza PascuaNo ratings yet

- Donation CasesDocument65 pagesDonation CasesJoan OlanteNo ratings yet

- Business Math Module 2Document17 pagesBusiness Math Module 2Rojane L. Alcantara100% (1)

- Regularisation of Unauthorised ConstructionDocument29 pagesRegularisation of Unauthorised ConstructionNagaraj KumbleNo ratings yet

- 2 Economics As An Applied ScienceDocument11 pages2 Economics As An Applied Sciencerommel legaspi100% (2)

- Pretest On AppliedDocument2 pagesPretest On AppliedmanilynNo ratings yet

- Applied Economics Module 6Document6 pagesApplied Economics Module 6Shaine TamposNo ratings yet

- Accountancy, Business and Management Summative Test (2 Quarter)Document3 pagesAccountancy, Business and Management Summative Test (2 Quarter)Alvin Echano Asanza100% (1)

- Cavity Wall Insulation in Existing Housing PDFDocument10 pagesCavity Wall Insulation in Existing Housing PDFCharles ThompsonNo ratings yet

- Applied Economics Module 1Document25 pagesApplied Economics Module 1Soobin ChoiNo ratings yet

- Abm 1 QuestionairesDocument4 pagesAbm 1 QuestionairesDindin Oromedlav LoricaNo ratings yet

- 2nd Quarterly Long Test in Applied EconomicsDocument2 pages2nd Quarterly Long Test in Applied EconomicsKim Lawrence R. BalaragNo ratings yet

- Grade 12 Exam 4q Applied Economics Last 1Document3 pagesGrade 12 Exam 4q Applied Economics Last 1Paul Paguia100% (1)

- Applied Economics 1st Quarter TestDocument2 pagesApplied Economics 1st Quarter TestdhorheeneNo ratings yet

- Applied Economics NotesDocument5 pagesApplied Economics NotesKhixel Jane PabroNo ratings yet

- For KnowledgeDocument4 pagesFor KnowledgeDeepak SashidharanNo ratings yet

- ABM-APPLIED-ECONOMICS-12 Q1 W1 Mod1 PDFDocument18 pagesABM-APPLIED-ECONOMICS-12 Q1 W1 Mod1 PDFNiel Ian100% (2)

- Applied Economics-Chapter 1Document57 pagesApplied Economics-Chapter 1Trixie Ruvi AlmiñeNo ratings yet

- DIRECTION: Read The Statement Carefully and Choose The Answer That Best Described The Statement. Write Your Answer in Your Answer SheetDocument3 pagesDIRECTION: Read The Statement Carefully and Choose The Answer That Best Described The Statement. Write Your Answer in Your Answer SheetGenelita B. PomasinNo ratings yet

- Applied Economics ExamDocument3 pagesApplied Economics ExamLee Dumalaga CarinanNo ratings yet

- Acctg Module 1 QuarterDocument22 pagesAcctg Module 1 QuarterAlthea Escarpe MartinezNo ratings yet

- 3rd Quarter Performance Task 2020 - 2021 AE 3-2Document2 pages3rd Quarter Performance Task 2020 - 2021 AE 3-2Jolly Roy BersalunaNo ratings yet

- Applied Eco ExamDocument5 pagesApplied Eco ExamJoan Ong-BayaniNo ratings yet

- Abm Test PaperDocument3 pagesAbm Test PaperNoel BanzuelaNo ratings yet

- Lesson 2 Applied EconomicsDocument2 pagesLesson 2 Applied EconomicsMarilyn DizonNo ratings yet

- Business Math Module 11Document9 pagesBusiness Math Module 11James Earl AbainzaNo ratings yet

- Economics Definition For A Progressive PhilippinesDocument19 pagesEconomics Definition For A Progressive PhilippinesJeff RamosNo ratings yet

- SUMTEST CHAPTER 1 (Student Copy)Document3 pagesSUMTEST CHAPTER 1 (Student Copy)Ann Cuartero SanchezNo ratings yet

- First Quarter ExamDocument3 pagesFirst Quarter ExamRaul CabantingNo ratings yet

- Chapter 2 - Applied EconomicsDocument4 pagesChapter 2 - Applied EconomicsMaleeha AhmadNo ratings yet

- Appendix D Answers To Odd-Numbered Section ExercisesDocument48 pagesAppendix D Answers To Odd-Numbered Section ExercisesBishop Panta0% (1)

- APPLIED ECONOMICS WorksheetDocument3 pagesAPPLIED ECONOMICS WorksheetgjakfjaNo ratings yet

- Grade 11 Sample Performance Task 478946 7Document13 pagesGrade 11 Sample Performance Task 478946 7api-235457167No ratings yet

- Lesson 1 Business EthicsDocument10 pagesLesson 1 Business EthicsSherren Marie Nala100% (1)

- Applied Economics Topics 1Document5 pagesApplied Economics Topics 1Raymund PatricioNo ratings yet

- Principles of Marketing: Carmona Senior High SchoolDocument8 pagesPrinciples of Marketing: Carmona Senior High SchoolKierstin Kyle RiegoNo ratings yet

- ABM11 Business Math Q1 W1 MODULE1Document13 pagesABM11 Business Math Q1 W1 MODULE1Ian BoneoNo ratings yet

- Introduction To Applied Economics: Slides Prepared by Leigh LimDocument25 pagesIntroduction To Applied Economics: Slides Prepared by Leigh LimJhun Ely Bhoy CampomanesNo ratings yet

- APPLIED ECONOMICS MODULE Sources: Applied Economics by Roman D. Leano Jr. and Applied Economics by DIWA Prepared By: Ms. Jocel Rose B. NgabitDocument3 pagesAPPLIED ECONOMICS MODULE Sources: Applied Economics by Roman D. Leano Jr. and Applied Economics by DIWA Prepared By: Ms. Jocel Rose B. Ngabitna2than-1No ratings yet

- Economics 6 Sept-2Document61 pagesEconomics 6 Sept-2Tavnish SinghNo ratings yet

- Applied EconomicsDocument22 pagesApplied EconomicsCiara ManangoNo ratings yet

- Lec01 Econ104 Introduction To Microeconomics 2019Document66 pagesLec01 Econ104 Introduction To Microeconomics 2019Peace PanasheNo ratings yet

- Introduction To Economics: Jerrold P. ElloDocument16 pagesIntroduction To Economics: Jerrold P. ElloJezreeljeanne Largo CaparosoNo ratings yet

- Managerial EconomicsDocument182 pagesManagerial Economicsmurali_aNo ratings yet

- Principles of EconomicsDocument34 pagesPrinciples of Economicssudiptaeg6645No ratings yet

- Week 1 Introduction To MicroeconomicsDocument39 pagesWeek 1 Introduction To Microeconomicstissot63No ratings yet

- C2 Economics As Social ScienceDocument23 pagesC2 Economics As Social ScienceStephen BulosNo ratings yet

- Definition of Economics:: Two Important Economic Conditions That Necessitate The Study of Economics?Document27 pagesDefinition of Economics:: Two Important Economic Conditions That Necessitate The Study of Economics?Navya NarayanamNo ratings yet

- Introduction To Business Economics: Session I and 2Document21 pagesIntroduction To Business Economics: Session I and 2Vignesh LakshminarayananNo ratings yet

- Intro To Economics 2013Document28 pagesIntro To Economics 2013John Louis PulidoNo ratings yet

- Part B Unit 5: EntrepreneurDocument38 pagesPart B Unit 5: EntrepreneurFire ShettyNo ratings yet

- Technical Product Description Release 2021Document104 pagesTechnical Product Description Release 2021Simón AcevedoNo ratings yet

- Dell IoMemory VSL 3.2.15 Release Notes 2017-11-07Document35 pagesDell IoMemory VSL 3.2.15 Release Notes 2017-11-07gjsmoNo ratings yet

- Measurement (Dee10013) Experiment 6: Title: Introduction To Power Meter (CLO 2)Document6 pagesMeasurement (Dee10013) Experiment 6: Title: Introduction To Power Meter (CLO 2)Mohd IskandarNo ratings yet

- Angew Chem Int Ed - 2022 - Bourguignon - Water Induced Self Blown Non Isocyanate Polyurethane FoamsDocument11 pagesAngew Chem Int Ed - 2022 - Bourguignon - Water Induced Self Blown Non Isocyanate Polyurethane FoamsHouda ElmoulouaNo ratings yet

- Verieye 12.2/megamatcher 12.2 Algorithm Demo: User'S GuideDocument11 pagesVerieye 12.2/megamatcher 12.2 Algorithm Demo: User'S GuideCarloss AlvarezzNo ratings yet

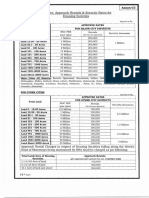

- Annex-C3 NOC Fee, Approach Rentals 86 Security Rates For Housing SocietiesDocument1 pageAnnex-C3 NOC Fee, Approach Rentals 86 Security Rates For Housing SocietiesSaqib RazaNo ratings yet

- D 2119 - 96 - RdixmtktukveDocument4 pagesD 2119 - 96 - RdixmtktukveRaphael CordovaNo ratings yet

- OFDMDocument5 pagesOFDMUsama JavedNo ratings yet

- AnaValid-ProtocSécurité V3.1Document15 pagesAnaValid-ProtocSécurité V3.1nyamsi claude bernardNo ratings yet

- Vector Analysis - Lecture Notes 01 - Vector Algebra-1 - 001Document12 pagesVector Analysis - Lecture Notes 01 - Vector Algebra-1 - 001Hjalmark SanchezNo ratings yet

- Helmets NFPA 1971 EV1 User GuideDocument8 pagesHelmets NFPA 1971 EV1 User GuideForum PompieriiNo ratings yet

- Sieve Shaker OCTAGON 200: General InformationDocument2 pagesSieve Shaker OCTAGON 200: General InformationSupriyo PNo ratings yet

- Stepper Motor Speed Control 1Document8 pagesStepper Motor Speed Control 1Mahesh kumarNo ratings yet

- Teac T-R670Document11 pagesTeac T-R670laoNo ratings yet

- Report of Online Medical StoreDocument26 pagesReport of Online Medical StoreMathanika. MNo ratings yet

- SLHT Business Finance WEEK 910Document7 pagesSLHT Business Finance WEEK 910Ian OcheaNo ratings yet

- Family Identity: A Framework of Identity Interplay in Consumption PracticesDocument21 pagesFamily Identity: A Framework of Identity Interplay in Consumption PracticesshalqmanqkNo ratings yet

- Berchtold Chromophare D-530,540,650,660 - Preinstallation InformationDocument14 pagesBerchtold Chromophare D-530,540,650,660 - Preinstallation InformationMahnaz BakhshiNo ratings yet

- Annual Report 2015Document585 pagesAnnual Report 201517crushNo ratings yet

- Direct VariationDocument1 pageDirect VariationOn-Cool ACNo ratings yet

- Lau Et Al 2015 - ReviewDocument10 pagesLau Et Al 2015 - ReviewJordana KalineNo ratings yet

- Reflection Paper: Importance of Financial Literacy To YouthDocument2 pagesReflection Paper: Importance of Financial Literacy To YouthCRISTEL MAE BARRANCONo ratings yet