0% found this document useful (0 votes)

154 views14 pagesTRA Code of Ethics Overview

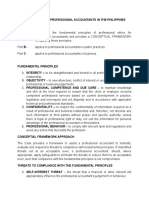

The document outlines the Code of Ethics for Professional Accountants. It discusses the importance of integrity, objectivity, professional competence, confidentiality, and professional behavior. It also identifies threats to compliance like self-interest, self-review, advocacy, familiarity, and intimidation threats. The code establishes a framework to identify threats, evaluate their significance, and apply safeguards to reduce threats or eliminate non-compliance with fundamental principles.

Uploaded by

Clarise Satentes AquinoCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

154 views14 pagesTRA Code of Ethics Overview

The document outlines the Code of Ethics for Professional Accountants. It discusses the importance of integrity, objectivity, professional competence, confidentiality, and professional behavior. It also identifies threats to compliance like self-interest, self-review, advocacy, familiarity, and intimidation threats. The code establishes a framework to identify threats, evaluate their significance, and apply safeguards to reduce threats or eliminate non-compliance with fundamental principles.

Uploaded by

Clarise Satentes AquinoCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd