You might also like

- Valuation ProblemsDocument2 pagesValuation ProblemsashviniNo ratings yet

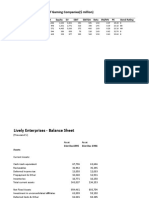

- Lively EnterprisesDocument5 pagesLively EnterprisesashviniNo ratings yet

- PVR Model - Data FileDocument17 pagesPVR Model - Data FileashviniNo ratings yet

- PVR Model - Data FileDocument17 pagesPVR Model - Data FileashviniNo ratings yet

- Adv Pack Historical DataDocument8 pagesAdv Pack Historical DataAnisha MathurNo ratings yet

- BHARTIARTL BObachuDocument4 pagesBHARTIARTL BObachuashviniNo ratings yet

- Fixed IncomeDocument2 pagesFixed IncomeashviniNo ratings yet

- ValuationDocument20 pagesValuationashviniNo ratings yet

- ValuationDocument20 pagesValuationashviniNo ratings yet

- Roles Functions Of: & SebiDocument61 pagesRoles Functions Of: & SebiashviniNo ratings yet

- Random VariablesDocument23 pagesRandom VariablesashviniNo ratings yet

- Random Variables PDFDocument23 pagesRandom Variables PDFashviniNo ratings yet

- Separation of Ownership and ManagementDocument2 pagesSeparation of Ownership and ManagementashviniNo ratings yet

- Quarterly Report Airtel Africa Q4 FY19Document55 pagesQuarterly Report Airtel Africa Q4 FY19ashviniNo ratings yet

- VectorDocument18 pagesVectorashviniNo ratings yet

- IB - Kenya FinalDocument14 pagesIB - Kenya FinalashviniNo ratings yet

- IB - Kenya Final PDFDocument14 pagesIB - Kenya Final PDFashviniNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 11 PJBUMI Digital Data Specialist DR NOOR AZLIZADocument7 pages11 PJBUMI Digital Data Specialist DR NOOR AZLIZAApexs GroupNo ratings yet

- AN6001-G16 Optical Line Terminal Equipment Product Overview Version ADocument74 pagesAN6001-G16 Optical Line Terminal Equipment Product Overview Version AAdriano CostaNo ratings yet

- Back WagesDocument24 pagesBack WagesfaisalfarizNo ratings yet

- Deutz Common RailDocument20 pagesDeutz Common RailAminadav100% (3)

- UntitledDocument2 pagesUntitledRoger GutierrezNo ratings yet

- CDS11412 M142 Toyota GR Yaris Plug-In ECU KitDocument19 pagesCDS11412 M142 Toyota GR Yaris Plug-In ECU KitVitor SegniniNo ratings yet

- Provisional DismissalDocument1 pageProvisional DismissalMyra CoronadoNo ratings yet

- Order of Nine Angles: RealityDocument20 pagesOrder of Nine Angles: RealityBrett StevensNo ratings yet

- Glyn Marston, Town Crier - Barry McQueen and Dept. Mayor - Tony LeeDocument1 pageGlyn Marston, Town Crier - Barry McQueen and Dept. Mayor - Tony LeeJake HoosonNo ratings yet

- The Confederation or Fraternity of Initiates (1941)Document82 pagesThe Confederation or Fraternity of Initiates (1941)Clymer777100% (1)

- Spaces For Conflict and ControversiesDocument5 pagesSpaces For Conflict and ControversiesVistalNo ratings yet

- Jeoparty Fraud Week 2022 EditableDocument65 pagesJeoparty Fraud Week 2022 EditableRhea SimoneNo ratings yet

- Team 12 Moot CourtDocument19 pagesTeam 12 Moot CourtShailesh PandeyNo ratings yet

- Periodic Table & PeriodicityDocument22 pagesPeriodic Table & PeriodicityMike hunkNo ratings yet

- The Syllable: The Pulse' or Motor' Theory of Syllable Production Proposed by The Psychologist RDocument6 pagesThe Syllable: The Pulse' or Motor' Theory of Syllable Production Proposed by The Psychologist RBianca Ciutea100% (1)

- Lifetime Prediction of Fiber Optic Cable MaterialsDocument10 pagesLifetime Prediction of Fiber Optic Cable Materialsabinadi123No ratings yet

- 47 Vocabulary Worksheets, Answers at End - Higher GradesDocument51 pages47 Vocabulary Worksheets, Answers at End - Higher GradesAya Osman 7KNo ratings yet

- WWW - Nswkendo IaidoDocument1 pageWWW - Nswkendo IaidoAshley AndersonNo ratings yet

- Molly On The Shore by Percy Grainger Unit StudyDocument5 pagesMolly On The Shore by Percy Grainger Unit Studyapi-659613441No ratings yet

- Eva Karene Romero (Auth.) - Film and Democracy in Paraguay-Palgrave Macmillan (2016)Document178 pagesEva Karene Romero (Auth.) - Film and Democracy in Paraguay-Palgrave Macmillan (2016)Gabriel O'HaraNo ratings yet

- Myocardial Concept MappingDocument34 pagesMyocardial Concept MappingTHIRD YEARNo ratings yet

- Ag Advace Check 8-30Document1 pageAg Advace Check 8-30AceNo ratings yet

- Social Studies 5th Grade Georgia StandardsDocument6 pagesSocial Studies 5th Grade Georgia Standardsapi-366462849No ratings yet

- 130004-1991-Maceda v. Energy Regulatory BoardDocument14 pages130004-1991-Maceda v. Energy Regulatory BoardChristian VillarNo ratings yet

- Cyber Ethics IssuesDocument8 pagesCyber Ethics IssuesThanmiso LongzaNo ratings yet

- Nota 4to Parcial ADocument8 pagesNota 4to Parcial AJenni Andrino VeNo ratings yet

- Principles of Marketing: Quarter 1 - Module 6: Marketing ResearchDocument17 pagesPrinciples of Marketing: Quarter 1 - Module 6: Marketing ResearchAmber Dela Cruz100% (1)

- Coaching Manual RTC 8Document1 pageCoaching Manual RTC 8You fitNo ratings yet

- SBFpart 2Document12 pagesSBFpart 2Asadulla KhanNo ratings yet

- Justice at Salem Reexamining The Witch Trials!!!!Document140 pagesJustice at Salem Reexamining The Witch Trials!!!!miarym1980No ratings yet