You might also like

- STT-ExplosiveProfitGuide v1c PDFDocument23 pagesSTT-ExplosiveProfitGuide v1c PDFIoannis Michelis100% (2)

- Eyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsDocument5 pagesEyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsSofía MargaritaNo ratings yet

- Freefincal - Prudent DIY Investing!Document11 pagesFreefincal - Prudent DIY Investing!Ta WexNo ratings yet

- Engineering Economics Reviewer Part 2 PDFDocument99 pagesEngineering Economics Reviewer Part 2 PDFagricultural and biosystems engineeringNo ratings yet

- Preference Share FormatDocument2 pagesPreference Share Formatankitstupid75% (4)

- Problems of The Depository System in IndiaDocument4 pagesProblems of The Depository System in IndiaAkash Gupta100% (1)

- Final Accounts ProblemsDocument7 pagesFinal Accounts ProblemsTushar SahuNo ratings yet

- Finance Chapter 1 True False QuestionsDocument4 pagesFinance Chapter 1 True False QuestionsThuyển ThuyểnNo ratings yet

- Lahore School of Economics Financial Management II Cash Flow Estimation and Risk Analysis - 2Document2 pagesLahore School of Economics Financial Management II Cash Flow Estimation and Risk Analysis - 2IIBRAHIM 245No ratings yet

- PG Diploma in Securities - Introduction to Capital Markets & Securities Law MCQsDocument9 pagesPG Diploma in Securities - Introduction to Capital Markets & Securities Law MCQsAnandNo ratings yet

- IT Act Provides Legal Framework for Cyber CrimesDocument26 pagesIT Act Provides Legal Framework for Cyber CrimesPriyanka Arora60% (5)

- Bill Market SchemesDocument2 pagesBill Market SchemesLeslie DsouzaNo ratings yet

- Regulatory Framework For Banking in IndiaDocument12 pagesRegulatory Framework For Banking in IndiaSidhant NaikNo ratings yet

- The Securities Contracts (Regulation) Act, 1956Document10 pagesThe Securities Contracts (Regulation) Act, 1956Akshay Aggarwal100% (1)

- Allowances and Minmum Wage ActDocument22 pagesAllowances and Minmum Wage ActjinujithNo ratings yet

- Case Record - NLIU - Justice Tankha MootDocument35 pagesCase Record - NLIU - Justice Tankha MootAmritya SinghNo ratings yet

- Rs 50 Stamp Paper TCS Service AgreementDocument4 pagesRs 50 Stamp Paper TCS Service AgreementAbhishek VijayanNo ratings yet

- Structure of RBIDocument3 pagesStructure of RBI9536909268No ratings yet

- Summary of Accounting EntriesDocument7 pagesSummary of Accounting EntriesABINASHNo ratings yet

- Tata Group of Companies: Interview Date: - 18 April 2015Document5 pagesTata Group of Companies: Interview Date: - 18 April 2015Naveen100% (1)

- Drafting & Pleading: (Question Bank)Document49 pagesDrafting & Pleading: (Question Bank)Gaurav KumarNo ratings yet

- Important Questions in Securities Laws For Cs Executive Group 2Document83 pagesImportant Questions in Securities Laws For Cs Executive Group 2debanka100% (2)

- Ag Gold Loan FormatDocument22 pagesAg Gold Loan Formatmevrick_guy100% (1)

- Ghana Cocoa Export RegulationsDocument5 pagesGhana Cocoa Export RegulationsRichard Jazzi Addo100% (1)

- Mohammed Bin Rashid Al Maktoum - WikipediaDocument37 pagesMohammed Bin Rashid Al Maktoum - WikipediaJeel VoraNo ratings yet

- Foreign Collaboration TypesDocument7 pagesForeign Collaboration Typesrahulravi4uNo ratings yet

- House Rental Agreement FormatDocument4 pagesHouse Rental Agreement FormatsravanNo ratings yet

- AUTHORIZATION LETTER-Exports - Authorisation - KYC-FEDEXDocument1 pageAUTHORIZATION LETTER-Exports - Authorisation - KYC-FEDEXMarta MierzejewskaNo ratings yet

- Start-Up GrantDocument9 pagesStart-Up GrantyoungtimerNo ratings yet

- Final PPT Reforms in Financial SystemDocument25 pagesFinal PPT Reforms in Financial SystemUSDavidNo ratings yet

- Concept and Types of Foreign CollobarationsDocument6 pagesConcept and Types of Foreign CollobarationsYash PunjabiNo ratings yet

- Investment Management NotesDocument40 pagesInvestment Management NotesSiddharth Ingle100% (1)

- Residential Status Problems 2021-2022-1Document5 pagesResidential Status Problems 2021-2022-120-UCO-517 AJAY KELVIN ANo ratings yet

- An Introduction To Client CounselingDocument26 pagesAn Introduction To Client CounselingshzubaidahNo ratings yet

- Stock Yard Agreement TermsDocument18 pagesStock Yard Agreement TermsSalman QureshiNo ratings yet

- PIL For Match Fixing-1Document49 pagesPIL For Match Fixing-1harsh0987636fbbjnNo ratings yet

- Abstract:: Protection of Investors in IndiaDocument23 pagesAbstract:: Protection of Investors in IndiaAbhimanyu SinghNo ratings yet

- Stock ExchangeDocument20 pagesStock ExchangeManish SolankiNo ratings yet

- CRB ScamDocument8 pagesCRB ScamSubodh MayekarNo ratings yet

- Rental Agreement FormatDocument3 pagesRental Agreement FormatJothiramkumar VenugopalNo ratings yet

- SMCCF Investment Management AgreementDocument67 pagesSMCCF Investment Management Agreemented_nycNo ratings yet

- SAMPLE Format of Customs Clearance Authorisation Letter: On Importing Customer Name LetterheadDocument1 pageSAMPLE Format of Customs Clearance Authorisation Letter: On Importing Customer Name LetterheadshifaNo ratings yet

- Documents Property VerificationDocument2 pagesDocuments Property Verificationgiri_placidNo ratings yet

- Paying BankerDocument18 pagesPaying Bankersagarg94gmailcom90% (10)

- Building Construction Agreement Format in MalayalamDocument15 pagesBuilding Construction Agreement Format in Malayalamachusmohan100% (1)

- IB PPT On IMFDocument22 pagesIB PPT On IMFAtul YadavNo ratings yet

- MRTP ACT - Monopolies and Restrictive Trade Practices ACT-1969Document9 pagesMRTP ACT - Monopolies and Restrictive Trade Practices ACT-1969Gopalakrishnan SivaramNo ratings yet

- What is a Stock Exchange? A Guide to Understanding Stock MarketsDocument50 pagesWhat is a Stock Exchange? A Guide to Understanding Stock Marketsaloo+gubhiNo ratings yet

- Stock Exchange & Its RegulationsDocument35 pagesStock Exchange & Its RegulationsSmita Jhankar100% (1)

- Contempt Case - FORMATDocument2 pagesContempt Case - FORMATAnjani Reddy MuvvaNo ratings yet

- Salient Features o The Insurance ActDocument15 pagesSalient Features o The Insurance Actchandni babunuNo ratings yet

- Trust Deed FormatDocument12 pagesTrust Deed Formatprashant kapilNo ratings yet

- @ProCA - Inter Contract Act RTP Question BankDocument6 pages@ProCA - Inter Contract Act RTP Question BankMr. indigoNo ratings yet

- Unit 5 Financial Planning and Tax ManagementDocument18 pagesUnit 5 Financial Planning and Tax ManagementnoroNo ratings yet

- Understand Badla System, Carry Forward Mechanism for StocksDocument11 pagesUnderstand Badla System, Carry Forward Mechanism for StocksCT SunilkumarNo ratings yet

- Rent Agreement FormatDocument3 pagesRent Agreement Formatbbaskar0% (1)

- State Control On Export and Import of GoodsDocument10 pagesState Control On Export and Import of GoodsAmudha MonyNo ratings yet

- Index: S. No. Title No. Remark SDocument17 pagesIndex: S. No. Title No. Remark SSiddhi PatwaNo ratings yet

- Stock Market - SEBI Regulations: From Navdeep Singh 10808865 RS1806b38Document22 pagesStock Market - SEBI Regulations: From Navdeep Singh 10808865 RS1806b38kaler21No ratings yet

- SEBIDocument24 pagesSEBIYashviNo ratings yet

- Venu FMSDocument37 pagesVenu FMSVenu GopalNo ratings yet

- 2 MBL KA Jun16 78838Document14 pages2 MBL KA Jun16 78838Shrikant BudholiaNo ratings yet

- Amrit Pai Sushil Ingle Anand LihinarDocument14 pagesAmrit Pai Sushil Ingle Anand Lihinaranand_lihinarNo ratings yet

- BIRLA Sun LifeDocument18 pagesBIRLA Sun LifeAbhishek KoriNo ratings yet

- Securities and Exchange Board of IndiaDocument57 pagesSecurities and Exchange Board of IndiaTanay Kumar SinghNo ratings yet

- SEBI Regulations Explained in 40 CharactersDocument19 pagesSEBI Regulations Explained in 40 CharactersMurugesh KumarNo ratings yet

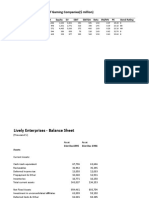

- Lively EnterprisesDocument5 pagesLively EnterprisesashviniNo ratings yet

- Valuation ProblemsDocument2 pagesValuation ProblemsashviniNo ratings yet

- PVR Model - Data FileDocument17 pagesPVR Model - Data FileashviniNo ratings yet

- PVR Model - Data FileDocument17 pagesPVR Model - Data FileashviniNo ratings yet

- Adv Pack Historical DataDocument8 pagesAdv Pack Historical DataAnisha MathurNo ratings yet

- Fixed IncomeDocument2 pagesFixed IncomeashviniNo ratings yet

- Indian Shadow Banking SystemDocument8 pagesIndian Shadow Banking SystemashviniNo ratings yet

- BHARTIARTL BObachuDocument4 pagesBHARTIARTL BObachuashviniNo ratings yet

- Installed capacity cash flow analysisDocument20 pagesInstalled capacity cash flow analysisashviniNo ratings yet

- Quarterly Report Airtel Africa Q4 FY19Document55 pagesQuarterly Report Airtel Africa Q4 FY19ashviniNo ratings yet

- Installed capacity cash flow analysisDocument20 pagesInstalled capacity cash flow analysisashviniNo ratings yet

- Random Variables PDFDocument23 pagesRandom Variables PDFashviniNo ratings yet

- Random VariablesDocument23 pagesRandom VariablesashviniNo ratings yet

- Separation of Ownership and ManagementDocument2 pagesSeparation of Ownership and ManagementashviniNo ratings yet

- Eigen Values and Eigen Vectors ExplainedDocument18 pagesEigen Values and Eigen Vectors ExplainedashviniNo ratings yet

- IB - Kenya Final PDFDocument14 pagesIB - Kenya Final PDFashviniNo ratings yet

- IB - Kenya FinalDocument14 pagesIB - Kenya FinalashviniNo ratings yet

- Amazing AFL1Document8 pagesAmazing AFL1Investor InvestorNo ratings yet

- Below Are Balance Sheet, Income Statement, Statement of Cash Flows, and Selected Notes To The Financial StatementsDocument14 pagesBelow Are Balance Sheet, Income Statement, Statement of Cash Flows, and Selected Notes To The Financial StatementsQueen ValleNo ratings yet

- Damodaran - Discounted Cash Flow ValuationDocument198 pagesDamodaran - Discounted Cash Flow ValuationYến NhiNo ratings yet

- FOREX - Trading With Clouds - Ichimoku PDFDocument5 pagesFOREX - Trading With Clouds - Ichimoku PDFfmicrosoft9164No ratings yet

- KV1 Jaipur FMM Class 11 Syllabus BreakdownDocument2 pagesKV1 Jaipur FMM Class 11 Syllabus Breakdownanupamasia@gmail.comNo ratings yet

- Peachtree GuideDocument36 pagesPeachtree GuideGUDATA ABARANo ratings yet

- Business Research MethodologyDocument12 pagesBusiness Research MethodologykarthikkrishnagokulNo ratings yet

- Portfolio Management PDFDocument27 pagesPortfolio Management PDFdwkr giriNo ratings yet

- CBSE Class 11 Accountancy - Journal EntriesDocument1 pageCBSE Class 11 Accountancy - Journal EntriesIbt Malda0% (1)

- MGPLc3 Daily HistoryDocument10 pagesMGPLc3 Daily HistoryNaman KalraNo ratings yet

- Hotel Jargon BusterDocument5 pagesHotel Jargon BusterNovia CareraNo ratings yet

- Independent Advisor Opinion VF - tcm387-622591Document26 pagesIndependent Advisor Opinion VF - tcm387-622591Valamunis DomingoNo ratings yet

- Stock Market Game (SMG)Document15 pagesStock Market Game (SMG)MarcusLamarWalkerNo ratings yet

- Phase 2 - 420 & 445Document60 pagesPhase 2 - 420 & 445SNo ratings yet

- Intraday Index Options Trading by Degree Gann Number System BuyingDocument51 pagesIntraday Index Options Trading by Degree Gann Number System BuyingRohit Solanki100% (2)

- Lesson 1 (Week 1) - Financial Assets at Fair Value and Investment in BondsDocument14 pagesLesson 1 (Week 1) - Financial Assets at Fair Value and Investment in BondsMonica MonicaNo ratings yet

- SOLUTIONS Monetary Policy Practice QuestionsDocument8 pagesSOLUTIONS Monetary Policy Practice QuestionsJaime SánchezNo ratings yet

- 23014Document114 pages23014Anshul MishraNo ratings yet

- Final Project Report On Religare SecuritiesDocument57 pagesFinal Project Report On Religare Securitiessunytomar1950% (6)

- Simulasi CashflowDocument24 pagesSimulasi CashflowDeviSulistiaNo ratings yet

- Chola: Enter A Better LifeDocument281 pagesChola: Enter A Better LifePRITAM PALNo ratings yet

- Quiz - Dissolution and Liquidation (Answers)Document8 pagesQuiz - Dissolution and Liquidation (Answers)peter pakerNo ratings yet

- DCF & Relative Valuation of Reliance EnergyDocument96 pagesDCF & Relative Valuation of Reliance EnergySovit JaiswalNo ratings yet