You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Security Market Operations BookDocument282 pagesSecurity Market Operations BookAbhishek AnandNo ratings yet

- HDFC Core BankingDocument32 pagesHDFC Core Bankingakashshah1069100% (1)

- Reserve Bank of IndiaDocument11 pagesReserve Bank of IndiaHarshSuryavanshiNo ratings yet

- Standerd ChartedDocument58 pagesStanderd ChartedashishgargNo ratings yet

- Managing Assets and Liabilities of Urban Co-op BanksDocument70 pagesManaging Assets and Liabilities of Urban Co-op BanksAbhiroop Bhattacharjee100% (1)

- New Generation Banking in IndiaDocument9 pagesNew Generation Banking in IndiaGanesh TiwariNo ratings yet

- Retail Banking (With Special Reference To Icici Bank)Document32 pagesRetail Banking (With Special Reference To Icici Bank)Varun PuriNo ratings yet

- RBI Functions: 1. Monopoly of Note IssueDocument5 pagesRBI Functions: 1. Monopoly of Note Issueshivam shandilyaNo ratings yet

- Pricing of Financial Products and Services Offered by BankDocument42 pagesPricing of Financial Products and Services Offered by BankSmitaNo ratings yet

- Role of Rbi in Indian Banking System 2022Document22 pagesRole of Rbi in Indian Banking System 2022ayushNo ratings yet

- Retail Banking of Allahabad BankDocument50 pagesRetail Banking of Allahabad Bankaru161112No ratings yet

- Union Bank of IndiaDocument33 pagesUnion Bank of Indiaraghavan swaminathanNo ratings yet

- KYC New ProjectDocument42 pagesKYC New ProjectNisha RathoreNo ratings yet

- Ind As 1Document64 pagesInd As 1vijaykumartaxNo ratings yet

- RBI Functions List: Traditional, Developmental, SupervisoryDocument25 pagesRBI Functions List: Traditional, Developmental, Supervisorygeethark12100% (1)

- Performance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalDocument72 pagesPerformance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalSatish P.Goyal71% (17)

- Introduction and Functions of Nationalized BankDocument10 pagesIntroduction and Functions of Nationalized BankPrashant MunnolliNo ratings yet

- NBFC NotesDocument2 pagesNBFC NotesHemavathy Gunaseelan100% (1)

- Radhika Growth of Banking SectorDocument36 pagesRadhika Growth of Banking SectorPranav ViraNo ratings yet

- For HDFC BankDocument31 pagesFor HDFC BankShalu Sushil Bansal80% (5)

- BankingDocument49 pagesBankingRitu BhatiyaNo ratings yet

- Bank of Maharashtra PDFDocument76 pagesBank of Maharashtra PDFPRATIK BhosaleNo ratings yet

- Bank of Boroda RajibDocument131 pagesBank of Boroda Rajibutpalbagchi100% (5)

- Unit 7 Merchant BankingDocument14 pagesUnit 7 Merchant BankingSravani RajuNo ratings yet

- Core Banking System - A Smarter Way of BankingDocument8 pagesCore Banking System - A Smarter Way of Bankingbudi.hw748No ratings yet

- Major Functions of International BankingDocument7 pagesMajor Functions of International BankingSandra Clem SandyNo ratings yet

- HDFC Bank Digital Services PDFDocument13 pagesHDFC Bank Digital Services PDFhtNo ratings yet

- Project On Audit of BankDocument71 pagesProject On Audit of BankSimran Sachdev0% (2)

- Reserve Bank of India (Rbi)Document27 pagesReserve Bank of India (Rbi)monika0827100% (1)

- Projects On Bank AuditDocument95 pagesProjects On Bank Auditloveaute1575% (4)

- Credit Risk ManagementDocument13 pagesCredit Risk ManagementVallabh UtpatNo ratings yet

- Union BankDocument4 pagesUnion Bankanandsingh1783No ratings yet

- Commercial Banking System and Role of RBI - Assignment June 2021Document6 pagesCommercial Banking System and Role of RBI - Assignment June 2021sadiaNo ratings yet

- Performance of Initial Public Offerings (IPOs) in Short Run and in Long Term in Indian Stock MarketDocument27 pagesPerformance of Initial Public Offerings (IPOs) in Short Run and in Long Term in Indian Stock MarketNaina AgrawalNo ratings yet

- Axis Bank LTD - Swot AnalysisDocument9 pagesAxis Bank LTD - Swot AnalysisSwapnil SinhaNo ratings yet

- Banking Sector ReformsDocument27 pagesBanking Sector ReformsArghadeep ChandaNo ratings yet

- Bhavin kkkkkkkkk38Document87 pagesBhavin kkkkkkkkk38Sandip ChovatiyaNo ratings yet

- Roll No.15, Tybbi 2010-11Document101 pagesRoll No.15, Tybbi 2010-11Amey Kolhe67% (3)

- Icici Bank ProjectDocument53 pagesIcici Bank ProjectKhem SinghNo ratings yet

- ICICI Securities IPO NoteDocument7 pagesICICI Securities IPO NoteSachinShingoteNo ratings yet

- Shraddha ProjectDocument70 pagesShraddha ProjectAkshay Harekar50% (2)

- Retail Banking in India - An IntroductionDocument73 pagesRetail Banking in India - An Introductionnatakhatnirmal33% (3)

- A Study On Bank of Maharashtra: Commercial Banking SystemDocument13 pagesA Study On Bank of Maharashtra: Commercial Banking SystemGovind N VNo ratings yet

- Comparing SBI and ICICI Bank internet banking facilitiesDocument7 pagesComparing SBI and ICICI Bank internet banking facilitiesEkta KhoslaNo ratings yet

- HDFC Bank Project Report OverviewDocument66 pagesHDFC Bank Project Report OverviewVarsha ValsanNo ratings yet

- IntershipDocument65 pagesIntershipainashaikhNo ratings yet

- Ratio Analysis ProjectDocument40 pagesRatio Analysis ProjectAnonymous g7uPednINo ratings yet

- Bank of Baroda BankingApplicationDocument45 pagesBank of Baroda BankingApplicationprateekNo ratings yet

- AUDIT BasicDocument10 pagesAUDIT BasicKingo StreamNo ratings yet

- M BankerDocument41 pagesM BankerNishi SinghNo ratings yet

- Merchant Banking: What Is It and What Do They DoDocument38 pagesMerchant Banking: What Is It and What Do They DoSmitha K BNo ratings yet

- How merchant banking is regulated in IndiaDocument3 pagesHow merchant banking is regulated in IndiaAayush NamanNo ratings yet

- Merchant Banking Functions and RegulationsDocument41 pagesMerchant Banking Functions and RegulationsPooja balwaniNo ratings yet

- Merchant BankDocument50 pagesMerchant BankGOVIND JANGIDNo ratings yet

- Merchant Banker LicenseDocument4 pagesMerchant Banker LicenseParas MittalNo ratings yet

- Merchant BankingDocument56 pagesMerchant BankingAkhil RajNo ratings yet

- E - Content On IFRSDocument20 pagesE - Content On IFRSPranit Satyavan NaikNo ratings yet

- EUR Account - Confirmation - Formel D (UK) Limited - 20200729 PDFDocument2 pagesEUR Account - Confirmation - Formel D (UK) Limited - 20200729 PDFGinho LeeNo ratings yet

- Employment Agreement SummaryDocument5 pagesEmployment Agreement SummarysperoNo ratings yet

- Wallstreetjournal 20170930 TheWallStreetJournalDocument54 pagesWallstreetjournal 20170930 TheWallStreetJournalJohn Paul (eschatology101 info)No ratings yet

- Questions. 1. Scarcity: A. Exists... : Question: Microeconomics Multiple Choice Questions. Please Answer All TheDocument14 pagesQuestions. 1. Scarcity: A. Exists... : Question: Microeconomics Multiple Choice Questions. Please Answer All TheRubina Hannure100% (1)

- Artikel Ksa-Telaah Kritis Adopsi Ifrs Di IndonesiaDocument11 pagesArtikel Ksa-Telaah Kritis Adopsi Ifrs Di Indonesiasuhita whini setyahuniNo ratings yet

- Chelmsford Annual Report 2009Document31 pagesChelmsford Annual Report 2009parkingeconomicsNo ratings yet

- Bhive Workspace Agreement I Magna Yuma Private LimitedI BTM PDFDocument10 pagesBhive Workspace Agreement I Magna Yuma Private LimitedI BTM PDFNidhiNo ratings yet

- IECA ISDA DF Protocol Amendment (11!30!12)Document10 pagesIECA ISDA DF Protocol Amendment (11!30!12)davidooNo ratings yet

- CSL 1040Document2 pagesCSL 1040oscar horacio floresNo ratings yet

- B.A. Ll.b. Ix Semester 2018Document4 pagesB.A. Ll.b. Ix Semester 2018ChaudharybanaNo ratings yet

- Propo1125sal For Legal Compliance Audit - WebconDocument2 pagesPropo1125sal For Legal Compliance Audit - Webconsandip_banerjeeNo ratings yet

- FNSACC624 1 Task 1: Written QuestionsDocument2 pagesFNSACC624 1 Task 1: Written QuestionsnattyNo ratings yet

- ps22 9Document161 pagesps22 9antonyNo ratings yet

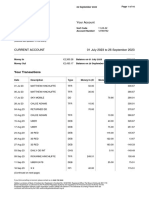

- Halifax Bank StatementDocument1 pageHalifax Bank StatementImraan IqbalNo ratings yet

- Advocates Only Can Argue Before A Statutory Legal AuthorityDocument9 pagesAdvocates Only Can Argue Before A Statutory Legal Authoritysilvernitrate1953No ratings yet

- Patterns of Innovation: A Case Study of US Pharmaceutical IndustryDocument9 pagesPatterns of Innovation: A Case Study of US Pharmaceutical IndustryhanythekingNo ratings yet

- Cheetah Annual Report 2017Document98 pagesCheetah Annual Report 2017安 娜 胡No ratings yet

- CN Can 0000072065Document3 pagesCN Can 0000072065Francisco Riascos GomezNo ratings yet

- Iso 7091-2000Document14 pagesIso 7091-2000Ahmed AliNo ratings yet

- Loc Gov ReviewerDocument47 pagesLoc Gov ReviewerbimbyboNo ratings yet

- Safety Inspector and Engineer Application Form - Rev.Document3 pagesSafety Inspector and Engineer Application Form - Rev.boyett0% (1)

- KYC AML CFT Procedure ManualDocument74 pagesKYC AML CFT Procedure ManualVipul Jain100% (7)

- The Coimbatore City Municipal Corporation Act, 1981Document297 pagesThe Coimbatore City Municipal Corporation Act, 1981Tarun KumarNo ratings yet

- Securities Lending Times Issue 236Document32 pagesSecurities Lending Times Issue 236Securities Lending TimesNo ratings yet

- Traffic Rules and RegulationsDocument11 pagesTraffic Rules and RegulationsRashid AliNo ratings yet

- Bloomberry Resorts and Hotels, Inc. vs. Bureau of Internal RevenueDocument13 pagesBloomberry Resorts and Hotels, Inc. vs. Bureau of Internal Revenuevince005No ratings yet

- HOME Managing A Business Taxes Taxation of Partnership FirmsDocument3 pagesHOME Managing A Business Taxes Taxation of Partnership FirmsKushagradhi DebnathNo ratings yet

- Flight Operation Inspectors ManualDocument210 pagesFlight Operation Inspectors Manualvikash_kumar_thakurNo ratings yet

- Cissp NotesDocument83 pagesCissp NotesRobert Mota HawksNo ratings yet