You might also like

- CEILI Study Guide (Eng)Document46 pagesCEILI Study Guide (Eng)liksyarnahNo ratings yet

- Introduction To Investment & SecurityDocument38 pagesIntroduction To Investment & Securitygitesh100% (1)

- Overview of NTPC Finance FunctionDocument17 pagesOverview of NTPC Finance FunctionSamNo ratings yet

- Employment ContractDocument2 pagesEmployment ContractLoucienne Leigh Diestro100% (1)

- How An Insurance Ornganisation WorksDocument10 pagesHow An Insurance Ornganisation Workssumit kumar goelNo ratings yet

- How An Insurance Ornganisation WorksDocument10 pagesHow An Insurance Ornganisation WorksKshitij KumarNo ratings yet

- Wealth Management Paper SolutionDocument11 pagesWealth Management Paper SolutionRahul SharmaNo ratings yet

- Asset Liability Management in Insurance: Submitted byDocument44 pagesAsset Liability Management in Insurance: Submitted bymasteranshulNo ratings yet

- Meaning and Nature of InvestmentDocument43 pagesMeaning and Nature of InvestmentVaishnavi GelliNo ratings yet

- L1 R48 HY NotesDocument4 pagesL1 R48 HY Notesayesha ansariNo ratings yet

- BCF 411-Asset Management - Pension Funds.Document3 pagesBCF 411-Asset Management - Pension Funds.Ken BiiNo ratings yet

- Capital Structure Issues: V. VI. V.1 Mergers and Acquisitions Definition and DifferencesDocument26 pagesCapital Structure Issues: V. VI. V.1 Mergers and Acquisitions Definition and Differenceskelvin pogiNo ratings yet

- Presentation 2Document23 pagesPresentation 2adeoghariaNo ratings yet

- Kim - Sbi Equity Hybrid FundDocument24 pagesKim - Sbi Equity Hybrid FundbbaalluuNo ratings yet

- Debt Securitization in IndiaDocument16 pagesDebt Securitization in Indiasaurabhm590No ratings yet

- Task Number 2: S.W.O.T. Analysis and Product Note of Various Asset ClassesDocument11 pagesTask Number 2: S.W.O.T. Analysis and Product Note of Various Asset ClassesChristin MathewNo ratings yet

- Mutual Fund-PresentationDocument31 pagesMutual Fund-Presentationraju100% (12)

- Corporate FinanceDocument66 pagesCorporate FinanceRobin SrivastavaNo ratings yet

- Proposal: Analysis of The Preference Level of Investors in Mutual Fund in AhmedabadDocument19 pagesProposal: Analysis of The Preference Level of Investors in Mutual Fund in AhmedabadAshutosh MishraNo ratings yet

- Capital Structure & Leverages - MarkedDocument16 pagesCapital Structure & Leverages - MarkedSundeep MogantiNo ratings yet

- Aif Taxation Regulatory FlyerDocument6 pagesAif Taxation Regulatory FlyerAmit SharmaNo ratings yet

- English For Financial Markets2Document72 pagesEnglish For Financial Markets2Zijian ZHUNo ratings yet

- 19UD57 Financial ManagementDocument19 pages19UD57 Financial Management19UD57 Vijay Ananth PNo ratings yet

- CF (Collected)Document76 pagesCF (Collected)Akhi Junior JMNo ratings yet

- English For Financial MarketsDocument74 pagesEnglish For Financial MarketsTRANNo ratings yet

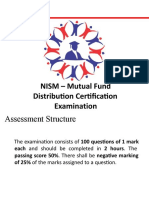

- NISM - Mutual Fund Distribution Certification ExaminationDocument169 pagesNISM - Mutual Fund Distribution Certification ExaminationPMNo ratings yet

- Chapter 3 InvestmentDocument46 pagesChapter 3 InvestmentmeenNo ratings yet

- Learning Objectives: Financial SystemDocument10 pagesLearning Objectives: Financial SystemVinita ThoratNo ratings yet

- Module IDocument52 pagesModule IBelugaNo ratings yet

- CF (Collected)Document92 pagesCF (Collected)Akhi Junior JMNo ratings yet

- 1.) Introduction and Rationale of Topic Chosen: 1.1) Mutual Fund - The ConceptDocument65 pages1.) Introduction and Rationale of Topic Chosen: 1.1) Mutual Fund - The ConceptMicro Solution IndiaNo ratings yet

- SAPM Ist UnitDocument13 pagesSAPM Ist UnitJaideep SharmaNo ratings yet

- 01 Financial Management - A Brief OverviewDocument22 pages01 Financial Management - A Brief OverviewVishal SinghNo ratings yet

- Project Report On Stock ExchangeDocument42 pagesProject Report On Stock ExchangeGuri BenipalNo ratings yet

- Content For Bridge CourseDocument43 pagesContent For Bridge CourseAlinaNo ratings yet

- Security Analysis and InvestmentDocument37 pagesSecurity Analysis and InvestmentAvayant Kumar SinghNo ratings yet

- Kim - Sbi Contra FundDocument24 pagesKim - Sbi Contra FundSharleneNo ratings yet

- Investment and Portfolio ManagementDocument28 pagesInvestment and Portfolio ManagementpadmNo ratings yet

- IPM - Unit-1 - Introduction To InvestmentDocument22 pagesIPM - Unit-1 - Introduction To InvestmentManshi AhirNo ratings yet

- 5 Reasons Why SBI BAFDocument3 pages5 Reasons Why SBI BAFRajdip HazraNo ratings yet

- SapmDocument35 pagesSapmparag_85No ratings yet

- Sources of FinanceDocument17 pagesSources of FinanceNikita ParidaNo ratings yet

- Prudent Investing: Invest in Mirae Asset Prudence Fund (MAPF)Document2 pagesPrudent Investing: Invest in Mirae Asset Prudence Fund (MAPF)api-349453187No ratings yet

- Why Mutual Fund April 10Document29 pagesWhy Mutual Fund April 10Malvika JhaNo ratings yet

- Assignment Financial Institutes and Markets 24 11 2018Document7 pagesAssignment Financial Institutes and Markets 24 11 2018devang asherNo ratings yet

- Draft Risk Based Capital Adequacy1Document16 pagesDraft Risk Based Capital Adequacy1ANGELLAH OTIENONo ratings yet

- Ammetlife - Ceilli (Eng) - Mas 2014Document159 pagesAmmetlife - Ceilli (Eng) - Mas 2014Suthakar SubramaniamNo ratings yet

- What Is A Mutual Fund?Document8 pagesWhat Is A Mutual Fund?Devansh Jignesh ShahNo ratings yet

- AMFI Training-Advisors' Module: A Joint Venture With Standard Life InvestmentsDocument125 pagesAMFI Training-Advisors' Module: A Joint Venture With Standard Life InvestmentsgautisinghNo ratings yet

- FM Module 4 Capital Structure of A CompanyDocument6 pagesFM Module 4 Capital Structure of A CompanyJeevan RobinNo ratings yet

- Anisation of The Financial SystemDocument31 pagesAnisation of The Financial SystemNiharika SinghNo ratings yet

- Mutual Funds: Sheenu Arora Jasmeet KaurDocument28 pagesMutual Funds: Sheenu Arora Jasmeet KaurSheenu AroraNo ratings yet

- "It Is Not Wise To Put All Eggs Into One Basket": Was Probably in The Minds of Those WhoDocument34 pages"It Is Not Wise To Put All Eggs Into One Basket": Was Probably in The Minds of Those Whoprasannabb7452No ratings yet

- Fundamentals of Financial Management: R.P. RustagiDocument16 pagesFundamentals of Financial Management: R.P. Rustagiimranrog11No ratings yet

- Investment Law EvolutionDocument39 pagesInvestment Law EvolutionAdarsh RanjanNo ratings yet

- IntermediaryDocument5 pagesIntermediarybtsvt1307 phNo ratings yet

- Alternative Investment (Real Estate)Document23 pagesAlternative Investment (Real Estate)Lami Moses AdekolaNo ratings yet

- Chapter1 PDFDocument10 pagesChapter1 PDFFarapple24No ratings yet

- Institute of Bankers of Sri Lanka: D 07 Investment BankingDocument18 pagesInstitute of Bankers of Sri Lanka: D 07 Investment BankingSuvindu DulhanNo ratings yet

- POs Pre Joining Study Material PDFDocument152 pagesPOs Pre Joining Study Material PDFKushagra Pratap SinghNo ratings yet

- BUS 206 - Ethical TestDocument5 pagesBUS 206 - Ethical TestAngela PerrymanNo ratings yet

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- Wording CGLDocument16 pagesWording CGLabielcahyaNo ratings yet

- A Guide To Claims - FIDIC Red Book 1999Document14 pagesA Guide To Claims - FIDIC Red Book 1999Ibrahim MohdNo ratings yet

- BMO0272 Week 2 Workshop SlidesDocument21 pagesBMO0272 Week 2 Workshop Slideskenechi lightNo ratings yet

- Adobe Scan 23 Nov 2021Document19 pagesAdobe Scan 23 Nov 2021xabaandiswa8No ratings yet

- Fixed Asset and Depreciation Schedule: Instructions: InputsDocument5 pagesFixed Asset and Depreciation Schedule: Instructions: InputsPatrick GhariosNo ratings yet

- Randstad Workmonitor 2023Document90 pagesRandstad Workmonitor 2023Ariella HotasiNo ratings yet

- Program Conducted by Institute Related To IPR, Entrepreneurship / Start-Ups & InnovationDocument26 pagesProgram Conducted by Institute Related To IPR, Entrepreneurship / Start-Ups & InnovationDaisy Arora KhuranaNo ratings yet

- Electronic Banking and Employees' Job Security in Lafia Nasarawa State, Nigeria Taiwo Olusegun AdelaniDocument19 pagesElectronic Banking and Employees' Job Security in Lafia Nasarawa State, Nigeria Taiwo Olusegun AdelaniNayab AkhtarNo ratings yet

- QozievDocument2 pagesQozievolegdanyleiko2No ratings yet

- Limits, Alternatives, and Choices: Mcgraw-Hill/IrwinDocument30 pagesLimits, Alternatives, and Choices: Mcgraw-Hill/IrwinWafaFarrukhNo ratings yet

- Beware Shape-Shifting Scammers in The PandemicDocument2 pagesBeware Shape-Shifting Scammers in The PandemicRichardNo ratings yet

- Title Business Partner Number Bus Part Cat Business Partner Role Category Business Partner GroupingDocument16 pagesTitle Business Partner Number Bus Part Cat Business Partner Role Category Business Partner GroupingRanjeet KumarNo ratings yet

- Group 6Document4 pagesGroup 6999660% (3)

- Do It Yourself?: Business PlanDocument4 pagesDo It Yourself?: Business PlansuryaramdegalaNo ratings yet

- Paper 4 Jeff BezosDocument5 pagesPaper 4 Jeff Bezosapi-535584932100% (1)

- Surendra Gupta Refuse To Pay NSELDocument2 pagesSurendra Gupta Refuse To Pay NSELBhoomiPatelNo ratings yet

- Ch5 MSA-Making-the-Franchise-Decision-WorkbookDocument95 pagesCh5 MSA-Making-the-Franchise-Decision-Workbookนายชัยสิทธิ์ เพชรรังษีNo ratings yet

- Orient Paper Mills, Amlai (Prop. Orient Paper & Industries Limited)Document1 pageOrient Paper Mills, Amlai (Prop. Orient Paper & Industries Limited)Ravi Shankar ChakravortyNo ratings yet

- Lochan Gowda 007 (5)Document97 pagesLochan Gowda 007 (5)Preethi dsNo ratings yet

- 1.5.6 Resultados Del Test de Estilo de EmprendedorDocument5 pages1.5.6 Resultados Del Test de Estilo de EmprendedorGFranco BlancasNo ratings yet

- 10 Golden Rules of Pricing ConversationsDocument3 pages10 Golden Rules of Pricing ConversationsPete Majkowski100% (1)

- Kroll Restructuring AdministrationDocument2 pagesKroll Restructuring AdministrationMarNo ratings yet

- Afm Module 3 - IDocument26 pagesAfm Module 3 - IABOOBAKKERNo ratings yet

- What Is ChangeDocument3 pagesWhat Is ChangeCalonneFrNo ratings yet

- Iffco at A GlanceDocument74 pagesIffco at A Glancelokesharya1No ratings yet