You might also like

- FABM2 Full ModuleDocument201 pagesFABM2 Full ModuleSumma Comms Laude100% (3)

- FABM 2 Statement of Financial PositionDocument20 pagesFABM 2 Statement of Financial PositionVictoria Manalaysay100% (1)

- Statement of Financial PositionDocument50 pagesStatement of Financial PositionSheilaMarieAnnMagcalas67% (3)

- 2016 14 PPT Acctg1 Adjusting EntriesDocument20 pages2016 14 PPT Acctg1 Adjusting Entriesash wu100% (3)

- Fabm 11: Module 08 (Q4-Week 2-5) : Complete Accounting Cycle For A Merchandising Business - PeriodicDocument12 pagesFabm 11: Module 08 (Q4-Week 2-5) : Complete Accounting Cycle For A Merchandising Business - PeriodicChristian Zebua100% (4)

- Module in Fabm 1: Department of Education Schools Division of Pasay CityDocument6 pagesModule in Fabm 1: Department of Education Schools Division of Pasay CityAngelica Mae SuñasNo ratings yet

- FABM2 - Q1 - Module 5 Analysis and Interpretation of Financial Statements - Docx Ver 3Document37 pagesFABM2 - Q1 - Module 5 Analysis and Interpretation of Financial Statements - Docx Ver 3Leo C. BarroroNo ratings yet

- FABM2 Module 2 Statement of Comprehensive IncomeDocument7 pagesFABM2 Module 2 Statement of Comprehensive IncomeRaidenhile mae Vicente100% (2)

- ABM-FABM2-12 - Q1 - W2 - Mod2 Online PDFDocument8 pagesABM-FABM2-12 - Q1 - W2 - Mod2 Online PDFchristine100% (1)

- Statement of Comprehensive IncomeDocument26 pagesStatement of Comprehensive IncomerachelNo ratings yet

- FABM2 ReviewerDocument7 pagesFABM2 ReviewerMakmak NoblezaNo ratings yet

- Preparing SCI for Service and Merchandising BusinessesDocument9 pagesPreparing SCI for Service and Merchandising BusinessesChristian Zebua100% (1)

- FABM 2 Module 2 SCI SCOE PDFDocument10 pagesFABM 2 Module 2 SCI SCOE PDFJOHN PAUL LAGAO100% (4)

- Cieverose College, Inc.: Fundamentals of Accountancy, Business and Management 2Document10 pagesCieverose College, Inc.: Fundamentals of Accountancy, Business and Management 2Venus Frias-Antonio100% (1)

- FABM2 Module 04 (Q1-W5)Document5 pagesFABM2 Module 04 (Q1-W5)Christian Zebua100% (1)

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDocument12 pagesThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- WR SFP Using Report and Account FormDocument10 pagesWR SFP Using Report and Account FormJohn Fort Edwin AmoraNo ratings yet

- Drill ABMDocument1 pageDrill ABMGeorge Gonzales78% (23)

- Abm Accountancy Lesson 1Document23 pagesAbm Accountancy Lesson 1Felixberto Dominic Bermudez Eruela55% (20)

- Statement of Changes in Equity - Practice ExercisesDocument2 pagesStatement of Changes in Equity - Practice ExercisesEvangeline Gicale25% (8)

- FABM2 Quarter 1 Module and WorksheetsDocument27 pagesFABM2 Quarter 1 Module and WorksheetsHeart polvos100% (1)

- FABM2Document32 pagesFABM2Ylena AllejeNo ratings yet

- Math 11 Fabm1 Abm Q2-Week 7Document14 pagesMath 11 Fabm1 Abm Q2-Week 7Mut Ya50% (2)

- Chapter2 Statement of Comprehensive IncomeDocument46 pagesChapter2 Statement of Comprehensive IncomeRonald De La Rama100% (1)

- Books of Accounts: Journals and LedgersDocument11 pagesBooks of Accounts: Journals and LedgersRD Suarez83% (6)

- Module 3 (Q1) FABM 2Document20 pagesModule 3 (Q1) FABM 2Charlo Sabater67% (9)

- CashflowDocument6 pagesCashflowAizia Sarceda Guzman71% (7)

- ABM Fundamentals of ABM 1 Module 11 Accounting Cycle of A Merchandising BusinessDocument16 pagesABM Fundamentals of ABM 1 Module 11 Accounting Cycle of A Merchandising BusinessMariel Santos60% (5)

- FABM - Horizontal & Vertical AnalysisDocument22 pagesFABM - Horizontal & Vertical Analysiswendell john mediana0% (1)

- FABM 2 - Midterm ExamDocument6 pagesFABM 2 - Midterm ExamJessica Esmeña100% (1)

- Abm - Income and Business TaxationDocument44 pagesAbm - Income and Business Taxationmeg100% (1)

- ppt2aCCOUNTING LESSON 3Document17 pagesppt2aCCOUNTING LESSON 3Rojane L. Alcantara100% (1)

- FABM 2 Module 3 SFPDocument7 pagesFABM 2 Module 3 SFPJOHN PAUL LAGAO50% (2)

- Learning Module: Community Colleges of The PhilippinesDocument41 pagesLearning Module: Community Colleges of The PhilippinesGianina De LeonNo ratings yet

- Fabm2 Q1Document149 pagesFabm2 Q1Gladys Angela Valdemoro50% (4)

- FABM 2 Module 4 SCFDocument10 pagesFABM 2 Module 4 SCFJOHN PAUL LAGAO100% (3)

- Basic Documents and Transactions Related To Banks DepositsDocument3 pagesBasic Documents and Transactions Related To Banks DepositsAngelica Omilla50% (2)

- Branches of AccountingDocument14 pagesBranches of AccountingSharif ShaikNo ratings yet

- ABM - Specialized Subject: Fundamentals of Accountancy, Business and Management 1Document14 pagesABM - Specialized Subject: Fundamentals of Accountancy, Business and Management 1Jupiter Whiteside100% (6)

- ABM Fundamentals of ABM 1 Module 12 Accounting Cycle of A Merchandising BusinessDocument16 pagesABM Fundamentals of ABM 1 Module 12 Accounting Cycle of A Merchandising BusinessMariel Santos67% (3)

- SCI for Service and Merchandising BusinessesDocument11 pagesSCI for Service and Merchandising BusinessesMylene SantiagoNo ratings yet

- Change in Equity SCEDocument3 pagesChange in Equity SCEAizia Sarceda Guzman100% (2)

- Statement of Changes in Equity (SCE)Document72 pagesStatement of Changes in Equity (SCE)GSOCION LOUSELLE LALAINE D.100% (1)

- Fabm2 Module 3Document18 pagesFabm2 Module 3Rea Mariz Jordan50% (2)

- Module 6 - Fabm2-MergedDocument37 pagesModule 6 - Fabm2-MergedJaazaniah S. PavilionNo ratings yet

- Fabm 2 Module 1Document14 pagesFabm 2 Module 1Marilyn Nelmida TamayoNo ratings yet

- FABM2 Module 05 (Q1-W6)Document12 pagesFABM2 Module 05 (Q1-W6)Christian ZebuaNo ratings yet

- FABM2 Q1 Mod2 Statement-Of-Comprehensive-Income v2Document24 pagesFABM2 Q1 Mod2 Statement-Of-Comprehensive-Income v2Neil Trezley Sunico BalajadiaNo ratings yet

- Journal and LedgersDocument3 pagesJournal and LedgersRhea Ramirez55% (11)

- Personal SCI StatementDocument24 pagesPersonal SCI StatementMylene Santiago100% (2)

- Fundamentals of Accountancy Business and Management 1: Learning Activity Sheet Posting To The LedgerDocument18 pagesFundamentals of Accountancy Business and Management 1: Learning Activity Sheet Posting To The Ledgerwhat's up mga kaibiganNo ratings yet

- Fundamentals of Accountancy, Business and Management 2: Quarter 1-Module 5Document28 pagesFundamentals of Accountancy, Business and Management 2: Quarter 1-Module 5Leigh Guittap100% (2)

- FABM2 Summative Test # 4Document2 pagesFABM2 Summative Test # 4randy magbudhi67% (3)

- Fundamentals of Accountancy, Business and Management 1 (First Quarter)Document80 pagesFundamentals of Accountancy, Business and Management 1 (First Quarter)Bernard Baruiz100% (1)

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae Sasutil100% (1)

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNo ratings yet

- The Accounting EquationDocument5 pagesThe Accounting EquationHuskyNo ratings yet

- Lu4 - State AccountingDocument32 pagesLu4 - State AccountingGrace AtencioNo ratings yet

- FABM1 Module C2Document11 pagesFABM1 Module C2Nathan CapsaNo ratings yet

- Lesson 1 Statement of Financial PositionDocument22 pagesLesson 1 Statement of Financial PositionMylene SantiagoNo ratings yet

- Emrah Abi̇ 2 101,1Document2 pagesEmrah Abi̇ 2 101,1İbrahim KocakNo ratings yet

- List of Licensed Private and Public Hospital 2011Document7 pagesList of Licensed Private and Public Hospital 2011TJ NgNo ratings yet

- 1RV18CV019 PPT InternDocument36 pages1RV18CV019 PPT InternAVIRAL ROYNo ratings yet

- Examiner's report on recording financial transactions examDocument3 pagesExaminer's report on recording financial transactions examAbdul SamadNo ratings yet

- 11th Accountancy Full Study Material English Medium 2023-24Document64 pages11th Accountancy Full Study Material English Medium 2023-24osama guyzz100% (1)

- S.NO. Particulars Page No.: - I 1.1 1 1.2 2 1.3 2 1.4 3 1.5 3 1.6 3 - Ii 2.1 Risk Management 4Document2 pagesS.NO. Particulars Page No.: - I 1.1 1 1.2 2 1.3 2 1.4 3 1.5 3 1.6 3 - Ii 2.1 Risk Management 4danishNo ratings yet

- Safetynet Credit Facility An Explanation of Your Running Account Credit AgreementDocument8 pagesSafetynet Credit Facility An Explanation of Your Running Account Credit AgreementLiliana IonNo ratings yet

- Interview Project 1 Comm1010Document2 pagesInterview Project 1 Comm1010api-272079841No ratings yet

- Provisional Pass Certificate ApplicationDocument1 pageProvisional Pass Certificate ApplicationPRATYAY DASNo ratings yet

- Flipkart MH Resort PPT by Rupam RoyDocument8 pagesFlipkart MH Resort PPT by Rupam RoyPuja ShawNo ratings yet

- Risk Management in Life InsuranceDocument75 pagesRisk Management in Life InsurancePuja Singh80% (5)

- Kotler Pom15 Im 12Document28 pagesKotler Pom15 Im 12Muhammad Umair100% (1)

- ACCA Examination Payment Portal: Purchase ReceiptDocument3 pagesACCA Examination Payment Portal: Purchase ReceiptAKSHAJ PRAKASHNo ratings yet

- Community Pharmacy ManagementDocument29 pagesCommunity Pharmacy ManagementAnushka Mani tripathiNo ratings yet

- PW 7 Fblex ZKDSPHQMDocument15 pagesPW 7 Fblex ZKDSPHQMReepak PoddarNo ratings yet

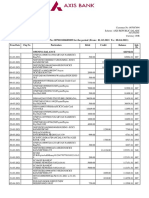

- Statement of Axis Account No:007010100685009 For The Period (From: 01-03-2021 To: 08-04-2021)Document3 pagesStatement of Axis Account No:007010100685009 For The Period (From: 01-03-2021 To: 08-04-2021)LakshayNo ratings yet

- Job Description AsmDocument3 pagesJob Description Asmrajnish guptaNo ratings yet

- Demand Letter Ms LeonyDocument2 pagesDemand Letter Ms Leonyfe garcia macasaetNo ratings yet

- Elevator Advertising SeattleDocument14 pagesElevator Advertising SeattleTAMTeamNo ratings yet

- Ibm 1004 ProjectDocument4 pagesIbm 1004 ProjectJitender SinghNo ratings yet

- Auditing Expenditure Cycle TestsDocument22 pagesAuditing Expenditure Cycle Testsmacmac29No ratings yet

- ManuSecure Brochure - Full - 2023Document17 pagesManuSecure Brochure - Full - 2023L JayNo ratings yet

- Letter of Intimation - STUDENT SECTIONDocument1 pageLetter of Intimation - STUDENT SECTIONHims GovaniNo ratings yet

- Banking SystemDocument2 pagesBanking Systemagus pratamaNo ratings yet

- Importance of Healthcare Information SystemsDocument18 pagesImportance of Healthcare Information SystemsJeneng KuNo ratings yet

- Importance of Reservation Department For The GuestsDocument14 pagesImportance of Reservation Department For The Guestssoundarya ReddyNo ratings yet

- Equb, Idir, Banks, InsurancesDocument3 pagesEqub, Idir, Banks, InsurancessccrNo ratings yet

- MAS 1 Activity Based CostingDocument2 pagesMAS 1 Activity Based CostingRoselle CabañeroNo ratings yet

- Rewards and Benefits AnnexureDocument2 pagesRewards and Benefits Annexureriteshh05No ratings yet

- Momshies Counter StatementDocument3 pagesMomshies Counter StatementKarl Jason Dolar CominNo ratings yet