You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Grave Secrecy Offshore Money-LaunderingDocument80 pagesGrave Secrecy Offshore Money-LaunderingSergey OrlovNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- (Digest) Manila Prince Hotel v. GSISDocument4 pages(Digest) Manila Prince Hotel v. GSISNN DDLNo ratings yet

- Day Trading Made EasyDocument220 pagesDay Trading Made EasyPhillip Jabu Mamba100% (2)

- Complaint For Recognition of Right of WayDocument6 pagesComplaint For Recognition of Right of WayJOHN JAY LABRADORNo ratings yet

- Vaclav Smil, Energy in 20th CenturyDocument31 pagesVaclav Smil, Energy in 20th Centuryryanghlee100% (1)

- T63 PDFDocument25 pagesT63 PDFÁlvaro Sánchez AbadNo ratings yet

- Omnifocus Trigger ListDocument2 pagesOmnifocus Trigger ListHiinoNo ratings yet

- Section III - Bid Data SheetDocument4 pagesSection III - Bid Data SheetChaitanyavarma DanduNo ratings yet

- 1-8-13 NYCDCC Funds v. O'Dwyer & Bernstien: SUMMONS + COMPLAINTDocument35 pages1-8-13 NYCDCC Funds v. O'Dwyer & Bernstien: SUMMONS + COMPLAINTrally524No ratings yet

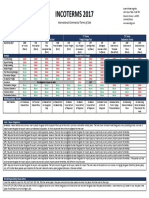

- Incoterms 2017Document1 pageIncoterms 2017iogenrNo ratings yet

- Topic 5 & 6 Current Liabilities, Provisions, and ContingenciesDocument75 pagesTopic 5 & 6 Current Liabilities, Provisions, and ContingenciesReverie SevillaNo ratings yet

- Sigalovada Sutta (Eng+Burmese)Document20 pagesSigalovada Sutta (Eng+Burmese)BuddhaDhammaSangahNo ratings yet

- Israel's Plan For World War Enters High GearDocument7 pagesIsrael's Plan For World War Enters High Gearaayola99No ratings yet

- Diagram 1 Diagram 2 Diagram 3: Answer (B) (I) ................................................Document1 pageDiagram 1 Diagram 2 Diagram 3: Answer (B) (I) ................................................Rana SlimNo ratings yet

- Physical Stock VerificationDocument11 pagesPhysical Stock Verificationsachinjindal4230No ratings yet

- 021-JPL Marketing Promotions v. CA, G.R. No. 151966, July 8, 2005Document5 pages021-JPL Marketing Promotions v. CA, G.R. No. 151966, July 8, 2005Jopan SJNo ratings yet

- General Terms and Conditi Ons of The "World of Winners" Ticket Offers CampaignDocument5 pagesGeneral Terms and Conditi Ons of The "World of Winners" Ticket Offers CampaignapolbusNo ratings yet

- Condiciones Particulares en Ingles Fusion DigitalDocument14 pagesCondiciones Particulares en Ingles Fusion DigitalAdina SobouNo ratings yet

- Bharathiar University, Coimbatore Bharathiar University, Coimbatore - 641 046Document2 pagesBharathiar University, Coimbatore Bharathiar University, Coimbatore - 641 046Rishe SandoshNo ratings yet

- Meralco Bribery CaseDocument61 pagesMeralco Bribery CaseJudge Florentino FloroNo ratings yet

- BANK 311 SlidesDocument18 pagesBANK 311 SlidesMaha AlanjawiNo ratings yet

- Surveying II - Week 2 Intersections: 1.1. Intersection Using Inner AnglesDocument9 pagesSurveying II - Week 2 Intersections: 1.1. Intersection Using Inner Anglesbest essaysNo ratings yet

- Executive Secretary v. Court of Appeals, 429 SCRA 81 (2004) FactsDocument6 pagesExecutive Secretary v. Court of Appeals, 429 SCRA 81 (2004) FactsRica Corsica LazanaNo ratings yet

- Bajaj Finance - Incred EquitiesDocument42 pagesBajaj Finance - Incred Equitieskumar somyaNo ratings yet

- Tarmac Matter Review - FormattedDocument6 pagesTarmac Matter Review - FormattedKellyNo ratings yet

- Dbm-Dilg-Nyc Joint Memoranudm Circular No. 1, Series of 2019Document19 pagesDbm-Dilg-Nyc Joint Memoranudm Circular No. 1, Series of 2019shella.msemNo ratings yet

- Aramex CF Enquiry BookletDocument5 pagesAramex CF Enquiry Bookletriwaj_ghimireNo ratings yet

- Case Study: BracbanklimitedDocument2 pagesCase Study: BracbanklimitedTajkira Hussain SonchitaNo ratings yet

- Mobil Dte Oil Light MsdsDocument13 pagesMobil Dte Oil Light MsdsNaseemNo ratings yet

- Forefront Identity Manager 2010 R2 Licensing DatasheetDocument2 pagesForefront Identity Manager 2010 R2 Licensing DatasheetXander PeruNo ratings yet