You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Fed Securities Laws - Rule OutlineDocument30 pagesFed Securities Laws - Rule OutlineVirginia Crowson100% (12)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Presentation On Types of CompaniesDocument21 pagesPresentation On Types of Companiesansh rao100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- HBR Case Study Blackstone and The Sale oDocument3 pagesHBR Case Study Blackstone and The Sale oRishav Agarwal50% (2)

- Elementary - Stop & Check - 1Document6 pagesElementary - Stop & Check - 1Nursultan100% (2)

- The Accounting Cycle:: Accruals and DeferralsDocument41 pagesThe Accounting Cycle:: Accruals and DeferralsNursultanNo ratings yet

- Williams 08Document63 pagesWilliams 08NursultanNo ratings yet

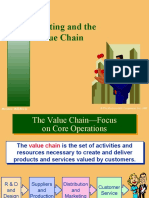

- Costing and The Value Chain: Mcgraw-Hill/IrwinDocument36 pagesCosting and The Value Chain: Mcgraw-Hill/IrwinNursultanNo ratings yet

- Global Business and Accounting: Mcgraw-Hill/IrwinDocument23 pagesGlobal Business and Accounting: Mcgraw-Hill/IrwinNursultanNo ratings yet

- FAR Practice MCQDocument17 pagesFAR Practice MCQBea PahuyoNo ratings yet

- Cgble Paper MCQ'S - 1Document30 pagesCgble Paper MCQ'S - 1sibtain samsungNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesDocument40 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesMuhammad AzamNo ratings yet

- Bronson Corporation 2017 Income Statement (In Mllions)Document4 pagesBronson Corporation 2017 Income Statement (In Mllions)Dianne CastroNo ratings yet

- Oriflame CompanyDocument3 pagesOriflame CompanyAlexandru AlexandraNo ratings yet

- FA Assignment For BBADocument5 pagesFA Assignment For BBArahul krishnaNo ratings yet

- 2020 BValuation ReportDocument440 pages2020 BValuation Reportraj28_999No ratings yet

- Amalgmation of CompanyDocument83 pagesAmalgmation of CompanySuryaNo ratings yet

- Module 1 - Cash and Cash EquivalentsDocument13 pagesModule 1 - Cash and Cash EquivalentsAlliah Mae RaizNo ratings yet

- Deutsche Bank Pitchbook AmTrust Why DB Pitchbook PDFDocument18 pagesDeutsche Bank Pitchbook AmTrust Why DB Pitchbook PDFRajat GoyalNo ratings yet

- Orlando Manufacturing Company Makes Camping Equipment Selected Account Balances ListedDocument1 pageOrlando Manufacturing Company Makes Camping Equipment Selected Account Balances ListedMiroslav GegoskiNo ratings yet

- Far Module 21 27Document61 pagesFar Module 21 27ryanNo ratings yet

- Essentials of Investments (BKM 5 Ed.) Answers To Selected Problems - Lecture 6Document3 pagesEssentials of Investments (BKM 5 Ed.) Answers To Selected Problems - Lecture 6Kunal KumudNo ratings yet

- Nabil Bank - Financials - 18-19Document127 pagesNabil Bank - Financials - 18-19shree salj dugda utpadakNo ratings yet

- Eminence Capital Men's WarehouseDocument2 pagesEminence Capital Men's WarehouseCanadianValueNo ratings yet

- Chapter 7Document11 pagesChapter 7Minh TúNo ratings yet

- UnauditedDocument30 pagesUnauditedSanjay KumarNo ratings yet

- Maintenance Charge Summary: Billing Period: Up To MarDocument5 pagesMaintenance Charge Summary: Billing Period: Up To MarSadman SayadNo ratings yet

- A141 Tutorial 5 Bkal1013Document8 pagesA141 Tutorial 5 Bkal1013Cyrilraincream0% (1)

- Audit Working Paper (Contoh)Document65 pagesAudit Working Paper (Contoh)Trick1 HahaNo ratings yet

- Statement of Financial Position (Reviewer)Document6 pagesStatement of Financial Position (Reviewer)ChinNo ratings yet

- LVMH Consolidated Statements PDFDocument74 pagesLVMH Consolidated Statements PDFThomasNo ratings yet

- Documento - MX Carlyn Cpa Encode PDFDocument10 pagesDocumento - MX Carlyn Cpa Encode PDFKeeiiiyyttt JoieNo ratings yet

- Question 3Document3 pagesQuestion 3Muhd AkmalNo ratings yet

- Complete Book 12Document9 pagesComplete Book 12Fidelia JabantoNo ratings yet

- RED Academy: LedgerDocument6 pagesRED Academy: LedgerDila Ram PaudelNo ratings yet

- FM Unit 3Document9 pagesFM Unit 3ashraf hussainNo ratings yet