You might also like

- Module IIDocument36 pagesModule IIYash UpasaniNo ratings yet

- Managerial Decision-Making in Perfectly Competitive MarketsDocument10 pagesManagerial Decision-Making in Perfectly Competitive Marketsjetro mark gonzalesNo ratings yet

- Pricing: Pricing Considerations and ApproachesDocument15 pagesPricing: Pricing Considerations and ApproachesALINo ratings yet

- Eco Project FinalDocument36 pagesEco Project FinalSakshamNo ratings yet

- Price Unit 2Document11 pagesPrice Unit 2MathiosNo ratings yet

- Unit 4 Economics Market Structure.Document68 pagesUnit 4 Economics Market Structure.Devyani ChettriNo ratings yet

- Assignment 3: Course Title: ECO101Document4 pagesAssignment 3: Course Title: ECO101Rashik AhmedNo ratings yet

- Rup Ratan Pine 01552438118: Economics For Managers Course No: 401Document32 pagesRup Ratan Pine 01552438118: Economics For Managers Course No: 401rifath rafiqNo ratings yet

- Chapter 7 Market StructuresDocument33 pagesChapter 7 Market StructuresAtikah RawiNo ratings yet

- ECO-501 All Question Ans For Mid Term Exam: Q. Define The Direct Tax and Indirect Tax & Give The Proper ExampleDocument7 pagesECO-501 All Question Ans For Mid Term Exam: Q. Define The Direct Tax and Indirect Tax & Give The Proper ExampleAsim HowladerNo ratings yet

- Lesson 11-Market StructuresDocument72 pagesLesson 11-Market StructuresDaniel VenturaNo ratings yet

- Monopolistic and Oligopoly Competition PDFDocument28 pagesMonopolistic and Oligopoly Competition PDFJennifer CarliseNo ratings yet

- 3 Pricing Approaches for Maximizing ProfitsDocument7 pages3 Pricing Approaches for Maximizing ProfitsErick AloyceNo ratings yet

- Pricing Methods ExplainedDocument15 pagesPricing Methods ExplainedmussaiyibNo ratings yet

- Chapter 8 - MonopolyDocument8 pagesChapter 8 - MonopolyEdgar SabusapNo ratings yet

- Chap V Market StructureDocument36 pagesChap V Market StructureDaniel YirdawNo ratings yet

- Colander Ch11 Perfect CompetitionDocument84 pagesColander Ch11 Perfect CompetitionVishal JoshiNo ratings yet

- Econ202 ch21Document37 pagesEcon202 ch21Kenny LohNo ratings yet

- Break Even Analysis ExplainedDocument9 pagesBreak Even Analysis Explainedsachin vermaNo ratings yet

- 6Document9 pages6abadi gebru100% (1)

- Princples - Pricing MethodsDocument16 pagesPrincples - Pricing Methodsmusonza murwiraNo ratings yet

- Team Member's: Varun Aggarwal Jyoti Chauhan Shashank Rana Preeti Pawaria Rahul Yadav Vijay Kundra Nitin Kumar Sapna RanaDocument75 pagesTeam Member's: Varun Aggarwal Jyoti Chauhan Shashank Rana Preeti Pawaria Rahul Yadav Vijay Kundra Nitin Kumar Sapna Ranagoyal_khushbu88No ratings yet

- Theory of Production and Costs ExplainedDocument5 pagesTheory of Production and Costs Explainedmochi antiniolosNo ratings yet

- Lesson Number: 10 Topic: Pure Competition: Course Code and Title: BACR2 Basic MicroeconomicsDocument10 pagesLesson Number: 10 Topic: Pure Competition: Course Code and Title: BACR2 Basic MicroeconomicsVirgie OrtizNo ratings yet

- Business Economics Assignment AnalysisDocument6 pagesBusiness Economics Assignment AnalysisChetan GoyalNo ratings yet

- Maximizing Profits in Different Market StructuresDocument28 pagesMaximizing Profits in Different Market StructuresAngela WaganNo ratings yet

- Lesson Number: 11 Topic: Monopoly: Course Code and Title: BACR2 Basic MicroeconomicsDocument13 pagesLesson Number: 11 Topic: Monopoly: Course Code and Title: BACR2 Basic MicroeconomicsVirgie OrtizNo ratings yet

- Perfect Competition Profit MacDocument51 pagesPerfect Competition Profit MacSmurf AccountNo ratings yet

- Unit 8-Revenue Analysis and Pricing PoliciesDocument17 pagesUnit 8-Revenue Analysis and Pricing PoliciesGayl Ignacio TolentinoNo ratings yet

- Sales and Marketing PlanDocument10 pagesSales and Marketing PlanHuong Tran NgocNo ratings yet

- Business EconomicsDocument9 pagesBusiness Economicsasaurav566No ratings yet

- Market Structure TypesDocument11 pagesMarket Structure TypesKyla BarbosaNo ratings yet

- Pricing 1Document19 pagesPricing 1İlker ToktasNo ratings yet

- Name: Zahid Bin Ali ID: 2019110000010 Section: 1 Course Code: MKT101 Course Name: Principles of MarketingDocument8 pagesName: Zahid Bin Ali ID: 2019110000010 Section: 1 Course Code: MKT101 Course Name: Principles of MarketingZahiD UniXNo ratings yet

- Pure CompetitionDocument7 pagesPure CompetitionEricka TorresNo ratings yet

- Why Is Perfect Competition Normally Regarded As BeingDocument6 pagesWhy Is Perfect Competition Normally Regarded As BeingMuhammad Asim Hafeez ThindNo ratings yet

- Pricing in FashionDocument21 pagesPricing in FashionarushiparasharNo ratings yet

- PRICING TACTICS LECTUREDocument24 pagesPRICING TACTICS LECTUREAgnes Meilina SinagaNo ratings yet

- Market StructuresDocument18 pagesMarket Structuresengr_rpcurbanoNo ratings yet

- MARKET STRUCTURES, COMPETITION TYPES, AND BARRIERSDocument18 pagesMARKET STRUCTURES, COMPETITION TYPES, AND BARRIERSSwing SeniorNo ratings yet

- Pricing MethodsDocument36 pagesPricing MethodsKennethEdizaNo ratings yet

- BUSINESS ECONOMICS SEMESTER I INTERNAL ASSIGNMENTDocument8 pagesBUSINESS ECONOMICS SEMESTER I INTERNAL ASSIGNMENTmeetNo ratings yet

- Group Report. Perfect CompetitionDocument31 pagesGroup Report. Perfect CompetitionMary Ann Manalo PanopioNo ratings yet

- Smart Pricing Strategies: March 2001Document5 pagesSmart Pricing Strategies: March 2001Mahesh NayakNo ratings yet

- Pricing Strategy: Internal Factors in Pricing A ProductDocument5 pagesPricing Strategy: Internal Factors in Pricing A Productainsyasya 98No ratings yet

- MARKETSTRUCTUREDocument14 pagesMARKETSTRUCTUREjh342703No ratings yet

- ECON 150 Course IntroductionDocument31 pagesECON 150 Course IntroductionRajshree DewooNo ratings yet

- Chapter Five Analysis of Market StructureDocument11 pagesChapter Five Analysis of Market Structurehayelom nigusNo ratings yet

- Eco Welfare & Pricing in MarketsDocument17 pagesEco Welfare & Pricing in Marketsveera reddyNo ratings yet

- Cost-oriented pricing journal articleDocument12 pagesCost-oriented pricing journal articlepall12100% (1)

- 7 Pricing DecisionsDocument14 pages7 Pricing DecisionsZenCamandangNo ratings yet

- MARKET STRUCURE PPTDocument43 pagesMARKET STRUCURE PPTGEORGENo ratings yet

- Unit - 3 EEFMDocument32 pagesUnit - 3 EEFMAppasani Manishankar100% (1)

- Pricing EconomicsDocument59 pagesPricing EconomicsJai JohnNo ratings yet

- Economics Tutorial 7Document30 pagesEconomics Tutorial 7LI SIEN CHEW100% (1)

- Typology of Market StructureDocument25 pagesTypology of Market StructureShane Angela Pajabera100% (1)

- ECON611 - Perfect Competition and Welfare AnalysisDocument24 pagesECON611 - Perfect Competition and Welfare Analysisshadrick malamaNo ratings yet

- Marketing Managers Guide to Financial ConceptsDocument18 pagesMarketing Managers Guide to Financial ConceptsShoaib Ud DinNo ratings yet

- The Market Makers (Review and Analysis of Spluber's Book)From EverandThe Market Makers (Review and Analysis of Spluber's Book)No ratings yet

- Economics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsFrom EverandEconomics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsNo ratings yet

- Lesson 3: Market Integration: The Rise of The Global CorporationDocument17 pagesLesson 3: Market Integration: The Rise of The Global CorporationAngelica VailocesNo ratings yet

- States The Relationship Between Inputs and Outputs: Inputs Land Rent Labour Wages CapitalDocument4 pagesStates The Relationship Between Inputs and Outputs: Inputs Land Rent Labour Wages CapitalAngelica VailocesNo ratings yet

- OligopolyDocument41 pagesOligopolyAbhishek FanseNo ratings yet

- MonopolyDocument17 pagesMonopolyelio chemeNo ratings yet

- Perfect Competition: By: Cherryzza Mae B. DumasigDocument9 pagesPerfect Competition: By: Cherryzza Mae B. DumasigAngelica VailocesNo ratings yet

- MONOPOLISTIC COMPETITION AND PROFIT MAXIMIZATIONDocument13 pagesMONOPOLISTIC COMPETITION AND PROFIT MAXIMIZATIONAngelica VailocesNo ratings yet

- Perfect Competition: By: Cherryzza Mae B. DumasigDocument9 pagesPerfect Competition: By: Cherryzza Mae B. DumasigAngelica VailocesNo ratings yet

- Film MeaningDocument1 pageFilm MeaningAngelica VailocesNo ratings yet

- Notes. Value of OneDocument1 pageNotes. Value of OneAngelica VailocesNo ratings yet

- Group 7 and Group 8Document1 pageGroup 7 and Group 8Angelica VailocesNo ratings yet

- MBCG863D International Logistics and Supply Chain Management EbookDocument170 pagesMBCG863D International Logistics and Supply Chain Management Ebookajeet sharmaNo ratings yet

- Rapport de Departement B2CDocument9 pagesRapport de Departement B2Cali mouddenNo ratings yet

- E-1/E-2 Visa Application RequirementsDocument4 pagesE-1/E-2 Visa Application RequirementsmasNo ratings yet

- Factors That Affect Cost of Good SoldDocument22 pagesFactors That Affect Cost of Good SoldJoan TiqueNo ratings yet

- Essay About MonopolyDocument15 pagesEssay About MonopolyNguyễn Lan HươngNo ratings yet

- Key Account Manager-Apatinska PivaraDocument1 pageKey Account Manager-Apatinska PivaraGajo VankaNo ratings yet

- Chapter Eleven: Pricing in RetailingDocument30 pagesChapter Eleven: Pricing in RetailingJanny SaffNo ratings yet

- Contract of Sale NotesDocument6 pagesContract of Sale NotesKuveri Kvr TjirasoNo ratings yet

- Chapter 15 MCQ on MonopolyDocument4 pagesChapter 15 MCQ on Monopolycik siti100% (1)

- Formulas! 0 Current Assets Current Liabilities: Working CapitalDocument9 pagesFormulas! 0 Current Assets Current Liabilities: Working CapitalMajoy BantocNo ratings yet

- Business Plan: (Aquarium Shop) : Prepared ForDocument23 pagesBusiness Plan: (Aquarium Shop) : Prepared ForshuhaibNo ratings yet

- Consignment AgreementDocument4 pagesConsignment Agreementerikha_aranetaNo ratings yet

- CFO Director Financial in United Arab Emirates Resume N RadhakrishnanDocument6 pagesCFO Director Financial in United Arab Emirates Resume N RadhakrishnanNRadhakrishnan1No ratings yet

- The Ambipur Brand: Powered byDocument11 pagesThe Ambipur Brand: Powered byvishalrathore_knit75% (4)

- DMart Case Emerald 2 Sept 2020Document13 pagesDMart Case Emerald 2 Sept 2020Himani ConnectNo ratings yet

- Manufacturing Account and Income Statement for Manufacturing BusinessesDocument27 pagesManufacturing Account and Income Statement for Manufacturing Businessesking brothersNo ratings yet

- Scheduling (Be Specific) : (A) A Retail Store ManagerDocument2 pagesScheduling (Be Specific) : (A) A Retail Store ManagerThư Võ100% (1)

- Darshan - Sunteck Real Estate UpdatedDocument12 pagesDarshan - Sunteck Real Estate Updateddarshan shettyNo ratings yet

- Tata CementDocument70 pagesTata Cementramansuthar100% (2)

- Strategic ManagementDocument52 pagesStrategic ManagementAnonymous cyZVcDeNo ratings yet

- BIR Form No. 2550MDocument2 pagesBIR Form No. 2550Mmijareschabelita2No ratings yet

- 1 Revisi Business PlanDocument14 pages1 Revisi Business PlanDina FradaniNo ratings yet

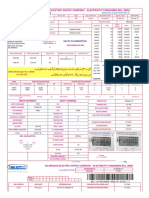

- Iesco Online Bill JulyDocument1 pageIesco Online Bill JulySyed Hadi Hussain ShahNo ratings yet

- Entrepreneorship and Small BusinessDocument14 pagesEntrepreneorship and Small BusinessВалерияNo ratings yet

- Cracking Case Interview: Profitability FrameworksDocument58 pagesCracking Case Interview: Profitability Frameworkscharan rana100% (2)

- BUS-670 M4 Costco Case AnalysisDocument9 pagesBUS-670 M4 Costco Case AnalysisCakeDshopNo ratings yet

- The Hershey Company: Abdullah, Esnaira A. Pantia, Patrik Oliver E. Pasaol, Devvie Mae ADocument18 pagesThe Hershey Company: Abdullah, Esnaira A. Pantia, Patrik Oliver E. Pasaol, Devvie Mae APatrik Oliver PantiaNo ratings yet

- Amazon GrinderDocument2 pagesAmazon GrinderAshok Kumar PanigrahiNo ratings yet

- Indirect Taxation Paper for MBA Exam with Questions on Composition SchemeDocument3 pagesIndirect Taxation Paper for MBA Exam with Questions on Composition SchemeShubham NamdevNo ratings yet

- Tax Invoice DetailsDocument1 pageTax Invoice Detailsmamillapalli sri harshaNo ratings yet