You might also like

- MGNT ScienceDocument45 pagesMGNT ScienceJezrel May SarvidaNo ratings yet

- Hillier Chapter 01Document30 pagesHillier Chapter 01Maybelle BernalNo ratings yet

- Introduction To Management Science: With SpreadsheetsDocument45 pagesIntroduction To Management Science: With SpreadsheetsJaycel Yam-Yam VerancesNo ratings yet

- Advance Decision Models: Trimester - 4Document28 pagesAdvance Decision Models: Trimester - 4Ajeet SinghNo ratings yet

- Introduction To Management ScienceDocument64 pagesIntroduction To Management ScienceRithesh KNo ratings yet

- Introduction To Management ScienceDocument38 pagesIntroduction To Management ScienceRithesh KNo ratings yet

- SO1 e Chap 11Document55 pagesSO1 e Chap 11Rithesh KNo ratings yet

- Introduction To Management Science: Linear Programming: Sensitivity Analysis and DualityDocument38 pagesIntroduction To Management Science: Linear Programming: Sensitivity Analysis and DualityLuvish MahajanNo ratings yet

- Chapter 1 Introduction OrganizationDocument24 pagesChapter 1 Introduction OrganizationJanile AlinanNo ratings yet

- Introduction To Management ScienceDocument46 pagesIntroduction To Management ScienceRithesh KNo ratings yet

- Project Management Chapter 1 Gray N LarsonDocument12 pagesProject Management Chapter 1 Gray N LarsonDendy Wibisono94% (18)

- Chapter 1Document20 pagesChapter 1Hany OktafianiNo ratings yet

- Chap-1-Modern Project ManagementDocument29 pagesChap-1-Modern Project ManagementSarah SahabdeenNo ratings yet

- Project Management by Gray and Larson (5) Visit Us at Management - Umakant.infoDocument33 pagesProject Management by Gray and Larson (5) Visit Us at Management - Umakant.infowelcome2jungleNo ratings yet

- Mcgraw-Hill/Irwin © 2003 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument26 pagesMcgraw-Hill/Irwin © 2003 The Mcgraw-Hill Companies, Inc., All Rights ReservedNurista Adenia WulandariNo ratings yet

- The Dynamics of People and Organizations: Mcgraw-Hill/Irwin © 2002 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument13 pagesThe Dynamics of People and Organizations: Mcgraw-Hill/Irwin © 2002 The Mcgraw-Hill Companies, Inc., All Rights ReservedFariyaHossainNo ratings yet

- Introduction To Strategic ManagementDocument28 pagesIntroduction To Strategic ManagementLilian LuchavezNo ratings yet

- Chap 008Document33 pagesChap 008Albert KurniawanNo ratings yet

- Decision Making: Dr. T.Srinivas RaoDocument61 pagesDecision Making: Dr. T.Srinivas RaoPushpa Latha MNo ratings yet

- MM ZG 523 / QMJ ZG 523 Project ManagementDocument52 pagesMM ZG 523 / QMJ ZG 523 Project Managementravindranath raoNo ratings yet

- Brs mdm3 ch01Document20 pagesBrs mdm3 ch01QuyênNo ratings yet

- Management ScienceDocument26 pagesManagement SciencePurushothama Reddy100% (1)

- Lecture 2Document50 pagesLecture 2fexiko9727No ratings yet

- 04 ForecastingDocument41 pages04 ForecastingShaneen Angelique MoralesNo ratings yet

- EE2211 Lecture 7Document43 pagesEE2211 Lecture 7Tze Long GanNo ratings yet

- Lecture 2 Strategy Ion and CultureDocument53 pagesLecture 2 Strategy Ion and CulturefrageursNo ratings yet

- CH 2 1Document35 pagesCH 2 1Desu Mekonnen100% (1)

- 9 Analisis Strategi Dan PilihanDocument54 pages9 Analisis Strategi Dan PilihanAngel Franda PutriNo ratings yet

- Powerful & Accurate Agile Es4ma4on: The Key To Unlocking PredictabilityDocument21 pagesPowerful & Accurate Agile Es4ma4on: The Key To Unlocking PredictabilityatilabayatNo ratings yet

- Chap 005Document26 pagesChap 005Hard workerNo ratings yet

- Performance Improvement Project ChecklistDocument10 pagesPerformance Improvement Project ChecklistJeffreyReyesNo ratings yet

- IE327 Lab BookDocument66 pagesIE327 Lab Bookjeffery Zeledon0% (2)

- Mcgraw-Hill/Irwin © 2006 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument19 pagesMcgraw-Hill/Irwin © 2006 The Mcgraw-Hill Companies, Inc., All Rights ReservedDicky Efendi Surya PutraNo ratings yet

- Mcgraw-Hill/Irwin © 2006 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument19 pagesMcgraw-Hill/Irwin © 2006 The Mcgraw-Hill Companies, Inc., All Rights Reservedvarun guptaNo ratings yet

- Mod ADocument29 pagesMod ASani SanjayaNo ratings yet

- Chapter 09Document26 pagesChapter 09donlorenzyyyNo ratings yet

- Chap07 Design of Work SystemsDocument17 pagesChap07 Design of Work SystemsR.ArumugamNo ratings yet

- Linier Programing - Metode GrafisDocument39 pagesLinier Programing - Metode Grafisariel mahardikaNo ratings yet

- Lean Webinar Series: A3 Management - Part IDocument53 pagesLean Webinar Series: A3 Management - Part IRicardo Fernando DenoniNo ratings yet

- Evaluating Work: Job EvaluationDocument42 pagesEvaluating Work: Job EvaluationInzamamul HaqueNo ratings yet

- Modern Project Management (Chapter-1)Document23 pagesModern Project Management (Chapter-1)samirNo ratings yet

- Business Planning With ExcelDocument6 pagesBusiness Planning With ExcelNeelakandan SivathanuNo ratings yet

- Lecture 7 - Overfitting, Bias-Variance Trade Off (DONE!!) PDFDocument42 pagesLecture 7 - Overfitting, Bias-Variance Trade Off (DONE!!) PDFSharelle TewNo ratings yet

- Chap002 Mission, Vision and Social ResponsibilityDocument34 pagesChap002 Mission, Vision and Social ResponsibilityAnkit MaharshiNo ratings yet

- Mansci 1Document25 pagesMansci 1Cillian ReevesNo ratings yet

- Forecasting: Forecast: - A Statement About The Future - Used To Help ManagersDocument36 pagesForecasting: Forecast: - A Statement About The Future - Used To Help ManagersHussain KamalNo ratings yet

- SME NPD Performance Mediated by Business Model InnovationDocument4 pagesSME NPD Performance Mediated by Business Model InnovationEltan TristanNo ratings yet

- StructureDocument48 pagesStructureKUEK BOON KANGNo ratings yet

- Compen 1Document13 pagesCompen 1Amit RathiNo ratings yet

- Special Challenges in Career Management: Mcgraw-Hill/IrwinDocument41 pagesSpecial Challenges in Career Management: Mcgraw-Hill/IrwinSahil GaurNo ratings yet

- ESC101 20239 Lecture 04Document37 pagesESC101 20239 Lecture 04M BNo ratings yet

- Operations Management: - ForecastingDocument97 pagesOperations Management: - ForecastingWuang ChingNo ratings yet

- Case Analysis FormatDocument2 pagesCase Analysis FormatBibiNo ratings yet

- Learning: Theories and Program DesignDocument43 pagesLearning: Theories and Program DesignTerry Luana AmeliasariNo ratings yet

- ch01 - Introduction To Quantitative AnalysisDocument34 pagesch01 - Introduction To Quantitative AnalysisElliyyanMizati100% (8)

- A Lean - Agile Learning Journey For Nokia S30/40 Managers: Module 2: Lean Software Development (Rev 2 22.9.09)Document30 pagesA Lean - Agile Learning Journey For Nokia S30/40 Managers: Module 2: Lean Software Development (Rev 2 22.9.09)AmrNo ratings yet

- Well Accepted and Essential Functions of Management Are Lanning Rganizing Taffing Irecting (Leading/Actuatin G) OntrollingDocument45 pagesWell Accepted and Essential Functions of Management Are Lanning Rganizing Taffing Irecting (Leading/Actuatin G) OntrollingRamachandra TurkaniNo ratings yet

- Innovative Performance Support: Strategies and Practices for Learning in the WorkflowFrom EverandInnovative Performance Support: Strategies and Practices for Learning in the WorkflowRating: 4.5 out of 5 stars4.5/5 (3)

- Cynefin-Framework as a Guide to Agile Leadership: Which Project Management Method for Which Type of Project? - Waterfall, Scrum, Kanban?From EverandCynefin-Framework as a Guide to Agile Leadership: Which Project Management Method for Which Type of Project? - Waterfall, Scrum, Kanban?No ratings yet

- MBL Annual Report FY 2020 21Document143 pagesMBL Annual Report FY 2020 21Rithesh KNo ratings yet

- MBL Annual Report FY 2019 20Document147 pagesMBL Annual Report FY 2019 20Rithesh KNo ratings yet

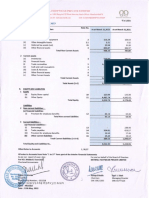

- Financial Statements Metmill 2021 2022Document47 pagesFinancial Statements Metmill 2021 2022Rithesh KNo ratings yet

- Metro Brands AR 2021 22 For Website v2 130822Document290 pagesMetro Brands AR 2021 22 For Website v2 130822Rithesh KNo ratings yet

- MBL Annual Report FY 2018 19Document136 pagesMBL Annual Report FY 2018 19Rithesh KNo ratings yet

- Balancesheet Audit Report F.Y 2020 21Document39 pagesBalancesheet Audit Report F.Y 2020 21Rithesh KNo ratings yet

- Provided, That The Foregoing Restrictions Shall Not Apply To Any Stockholder Election or Determination Pursuant To Section 1 (G) (Iii) of ArticleDocument1 pageProvided, That The Foregoing Restrictions Shall Not Apply To Any Stockholder Election or Determination Pursuant To Section 1 (G) (Iii) of ArticleRithesh KNo ratings yet

- 21 019153 9Document1 page21 019153 9Rithesh KNo ratings yet

- DM On Metro WebsiteDocument1 pageDM On Metro WebsiteRithesh KNo ratings yet

- 21 019153 14Document1 page21 019153 14Rithesh KNo ratings yet

- 21 019153 13Document1 page21 019153 13Rithesh KNo ratings yet

- Officer On This 24th Day of September, 2021Document1 pageOfficer On This 24th Day of September, 2021Rithesh KNo ratings yet

- 21 019153 10Document1 page21 019153 10Rithesh KNo ratings yet

- 21 019153 6Document1 page21 019153 6Rithesh KNo ratings yet

- 21 019153 8Document1 page21 019153 8Rithesh KNo ratings yet

- 21 019153 16Document1 page21 019153 16Rithesh KNo ratings yet

- 21 019153 11Document1 page21 019153 11Rithesh KNo ratings yet

- 21 019153 4Document1 page21 019153 4Rithesh KNo ratings yet

- 21 019153 5Document1 page21 019153 5Rithesh KNo ratings yet

- SignaturesDocument1 pageSignaturesRithesh KNo ratings yet

- 21 019153 12Document1 page21 019153 12Rithesh KNo ratings yet

- Management Control in Multinational Companies: A Systematic Literature ReviewDocument44 pagesManagement Control in Multinational Companies: A Systematic Literature ReviewRithesh KNo ratings yet

- 21 019153 7Document1 page21 019153 7Rithesh KNo ratings yet

- Three-Year Strategic Plan 2015-2018: Strategic Plan Adopted by The Aftd Board of Directors DECEMBER 12, 2014Document21 pagesThree-Year Strategic Plan 2015-2018: Strategic Plan Adopted by The Aftd Board of Directors DECEMBER 12, 2014Rithesh KNo ratings yet

- Amendment and Restatement of Certificate of Incorporation: Item 5.03 Amendments To Articles of Incorporation or BylawsDocument1 pageAmendment and Restatement of Certificate of Incorporation: Item 5.03 Amendments To Articles of Incorporation or BylawsRithesh KNo ratings yet

- Jerome Guillen Leaves TeslaDocument3 pagesJerome Guillen Leaves TeslaMaria MeranoNo ratings yet

- HSRCStratplan 1011 To 12132Document33 pagesHSRCStratplan 1011 To 12132Rithesh KNo ratings yet

- 2018 Annual Report MNE Guidelines ENDocument108 pages2018 Annual Report MNE Guidelines ENmaiariasrNo ratings yet

- Sample Strategic Business PlanDocument33 pagesSample Strategic Business PlanDande Pratama PutraNo ratings yet

- Three-Year Strategic Plan: Spring 2015Document40 pagesThree-Year Strategic Plan: Spring 2015Rithesh KNo ratings yet

- 1 Eli Lilly Case StudyDocument5 pages1 Eli Lilly Case Studytiiworks50% (2)

- GDP Chapters 21 Expenditure Income Real NominalDocument5 pagesGDP Chapters 21 Expenditure Income Real NominalElio BazNo ratings yet

- 04 PM-Tricks - CostDocument27 pages04 PM-Tricks - CostMahmoud HagagNo ratings yet

- Apple EFE, IFE, CPM MatrixDocument3 pagesApple EFE, IFE, CPM MatrixAndrew Knop45% (11)

- Chapter 8 Powerpoint Slides-2Document33 pagesChapter 8 Powerpoint Slides-2Goitsemodimo SennaNo ratings yet

- Tiếng anh tài chính ngân hàng: a.payments b.events c.transactionsDocument5 pagesTiếng anh tài chính ngân hàng: a.payments b.events c.transactionsBích NgọcNo ratings yet

- Sony Betamax Brand Failure: Hitesh BhasinDocument3 pagesSony Betamax Brand Failure: Hitesh Bhasinakash bathamNo ratings yet

- Digital Marketing ProjectDocument55 pagesDigital Marketing Projectsarah IsharatNo ratings yet

- Management Representation LetterDocument3 pagesManagement Representation LetterPreeti mittalNo ratings yet

- ST - Joseph's Degree & PG College Business Law Unit1Document14 pagesST - Joseph's Degree & PG College Business Law Unit1Saud Waheed KhanNo ratings yet

- Push Carts VapeDocument8 pagesPush Carts Vapemuhammad ibrarNo ratings yet

- A Wal-Mart Neighborhood MarketDocument8 pagesA Wal-Mart Neighborhood MarketJagdeep ChughNo ratings yet

- Southwest Airlines Success: A Case Study Analysis: January 2011Document6 pagesSouthwest Airlines Success: A Case Study Analysis: January 2011Fabián RosalesNo ratings yet

- People and Economic Activity - Wine Industry and Case StudyDocument17 pagesPeople and Economic Activity - Wine Industry and Case StudyShane Daly100% (3)

- Ibps Pos Prelims 1 2022Document9 pagesIbps Pos Prelims 1 2022s170252 P.ASHOK sklmNo ratings yet

- Astrologer H. Spencer Lewis (1908)Document1 pageAstrologer H. Spencer Lewis (1908)Clymer777No ratings yet

- Resume of Omar JadallahDocument1 pageResume of Omar JadallahOmar Jamal 5799No ratings yet

- Jam 2023Document35 pagesJam 2023iamphilospher1No ratings yet

- GX Global Powers of Luxury Goods 2023Document78 pagesGX Global Powers of Luxury Goods 2023xen101No ratings yet

- Strategic Human Resource ManagementDocument59 pagesStrategic Human Resource ManagementFrancisquete BNo ratings yet

- Priti Diamond and Gold Jewellery - Dhruvil20200201085Document16 pagesPriti Diamond and Gold Jewellery - Dhruvil20200201085VedantNo ratings yet

- IN Classguide en-GBDocument54 pagesIN Classguide en-GBcatalin9494No ratings yet

- Accounting Cycle: Service BusinessDocument16 pagesAccounting Cycle: Service BusinessMavie PhotographyNo ratings yet

- Which of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Document3 pagesWhich of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Kath LeynesNo ratings yet

- Jipangyi Ice CreamDocument19 pagesJipangyi Ice CreamHANNANo ratings yet

- Principles of Marketing - Quarter 3 - Module 3 (For Print)Document10 pagesPrinciples of Marketing - Quarter 3 - Module 3 (For Print)Stephanie Minor75% (4)

- Tutorial - 1 - 2 - (06.10.2022, 13.10.22) TOPIC: Basic Cost Terms and Concepts, Cost Classification Ex. 1Document3 pagesTutorial - 1 - 2 - (06.10.2022, 13.10.22) TOPIC: Basic Cost Terms and Concepts, Cost Classification Ex. 1Tomas SanzNo ratings yet

- SBI Seeks Insolvency of Western Refrigeration over GuaranteeDocument16 pagesSBI Seeks Insolvency of Western Refrigeration over Guaranteeveer vikramNo ratings yet

- Copia de SustainableFashionandTextilesDesignJourneysbyKateFletcherEarthscan2008Document6 pagesCopia de SustainableFashionandTextilesDesignJourneysbyKateFletcherEarthscan2008martina torresNo ratings yet

- What is Logistics? - An overview of logistics, its key components and significanceDocument20 pagesWhat is Logistics? - An overview of logistics, its key components and significanceAmandeep Singh BediNo ratings yet