You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Project Topics: KanishkDocument1 pageProject Topics: KanishkRahul SharmaNo ratings yet

- Corporate Tax Planning PDFDocument130 pagesCorporate Tax Planning PDFRahul SharmaNo ratings yet

- Taxation Project Sem VDocument21 pagesTaxation Project Sem VRahul SharmaNo ratings yet

- Reservation in IndiaDocument11 pagesReservation in IndiaRahul Sharma100% (1)

- Corporate Tax: by V Surya Narayana Raju, Assistant Professor of Law, HNLU, VishakapatanamDocument12 pagesCorporate Tax: by V Surya Narayana Raju, Assistant Professor of Law, HNLU, VishakapatanamRahul SharmaNo ratings yet

- Data Protection Laws: International Prospective: Hidayatullah National Law University Naya Raipur, C.GDocument28 pagesData Protection Laws: International Prospective: Hidayatullah National Law University Naya Raipur, C.GRahul SharmaNo ratings yet

- Role and Fuctions of Securities and Exchange Board of India: A Project OnDocument27 pagesRole and Fuctions of Securities and Exchange Board of India: A Project OnRahul SharmaNo ratings yet

- Expropriation of PropertyDocument4 pagesExpropriation of PropertyRahul SharmaNo ratings yet

- Master of LawsDocument5 pagesMaster of LawsRahul SharmaNo ratings yet

- Rahul Crim FinalDocument29 pagesRahul Crim FinalRahul SharmaNo ratings yet

- Health LawDocument2 pagesHealth LawRahul SharmaNo ratings yet

- Legal Mirror - V1 - I2 PDFDocument296 pagesLegal Mirror - V1 - I2 PDFRahul SharmaNo ratings yet

- Witness Protection SchemeDocument7 pagesWitness Protection SchemeRahul SharmaNo ratings yet

- Manish LRM FinalDocument19 pagesManish LRM FinalRahul SharmaNo ratings yet

- Chanakya National Law University Patna: Human Trafficking in IndiaDocument20 pagesChanakya National Law University Patna: Human Trafficking in IndiaRahul Sharma100% (1)

- New Doc 2020-02-14 10.35.14Document5 pagesNew Doc 2020-02-14 10.35.14Rahul SharmaNo ratings yet

- New Doc 2020-02-14 10.19.25Document18 pagesNew Doc 2020-02-14 10.19.25Rahul SharmaNo ratings yet

- HONOUR KILLING FinalDocument22 pagesHONOUR KILLING FinalRahul SharmaNo ratings yet

- Pca, 1988Document20 pagesPca, 1988Rahul SharmaNo ratings yet

- Banking - Project CompleteDocument22 pagesBanking - Project CompleteRahul SharmaNo ratings yet

- Dcom508 Corporate Tax PlanningDocument5 pagesDcom508 Corporate Tax PlanningRahul SharmaNo ratings yet

- Bhatia International To BALCO: Piloting A Much Needed Course CorrectionDocument16 pagesBhatia International To BALCO: Piloting A Much Needed Course CorrectionRahul SharmaNo ratings yet

- A D: T I A: Hidayatullah National Law UniversityDocument17 pagesA D: T I A: Hidayatullah National Law UniversityRahul SharmaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- TXTN Amendments To Estate Taxes Under The Train Law November 7Document4 pagesTXTN Amendments To Estate Taxes Under The Train Law November 7Margz CafifgeNo ratings yet

- Richard 2019Document29 pagesRichard 2019Richard MoszynskiNo ratings yet

- Broadband Bill Feb-24Document2 pagesBroadband Bill Feb-24shuja147No ratings yet

- Determination of Retention Fees For Dev-Asstd HL Accts and Transfer or Reg Fees For Retail HL AcctsDocument2 pagesDetermination of Retention Fees For Dev-Asstd HL Accts and Transfer or Reg Fees For Retail HL AcctsJonniel De GuzmanNo ratings yet

- Adobe Scan Feb 08, 2024Document1 pageAdobe Scan Feb 08, 2024mdo.sc1No ratings yet

- Payslip 202403Document1 pagePayslip 202403rashidah hajariNo ratings yet

- Sharad J Taank ITR 2021-2022Document3 pagesSharad J Taank ITR 2021-2022sharad.taankNo ratings yet

- Yanet CollegeDocument3 pagesYanet CollegeBiniam Hunegnaw BitewNo ratings yet

- Transaction Report For Juan Pablo Rodriguez Virasoro Date Range Filter CustomerDocument1 pageTransaction Report For Juan Pablo Rodriguez Virasoro Date Range Filter CustomerJuan VirazoroNo ratings yet

- Tax InvoiceDocument1 pageTax Invoiceaqib sofiNo ratings yet

- Quicknotes - Partnership, Estate, - TrustDocument7 pagesQuicknotes - Partnership, Estate, - TrustTwish BarriosNo ratings yet

- Canapi - 04 Quiz 1Document2 pagesCanapi - 04 Quiz 1sora fpsNo ratings yet

- Computer Application ExcelDocument1 pageComputer Application ExcelAmirah NatasyaNo ratings yet

- (Solution) Take Home Assignment 3 (2023S)Document3 pages(Solution) Take Home Assignment 3 (2023S)何健珩No ratings yet

- BTZmcnRBN2taSnE0QmlvbTF0MnNsZz09 InvoiceDocument2 pagesBTZmcnRBN2taSnE0QmlvbTF0MnNsZz09 InvoiceGurvinder SinghNo ratings yet

- VAT-problems-key by Andrew Gil AmbrayDocument10 pagesVAT-problems-key by Andrew Gil AmbrayMark Gelo WinchesterNo ratings yet

- House Tax Assessment Details PDFDocument1 pageHouse Tax Assessment Details PDFSatyaNo ratings yet

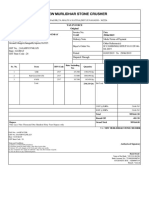

- New Murlidhar Stone Crusher: Tax Invoice OriginalDocument1 pageNew Murlidhar Stone Crusher: Tax Invoice OriginalrajendranrajendranNo ratings yet

- 5% and 1% Stamp Duty ExemptionDocument2 pages5% and 1% Stamp Duty ExemptionAbhinand S VijayNo ratings yet

- Veronica Sanchez Vs CirDocument3 pagesVeronica Sanchez Vs CirArthur John Garraton0% (1)

- GST Bill-128 ORRISDocument1 pageGST Bill-128 ORRISMANJEET YADAVNo ratings yet

- 16 Account Showing CNCDocument2 pages16 Account Showing CNCAngel RamírezNo ratings yet

- Itr-V: (Please See Rule 12 of The Income-Tax Rules, 1962)Document1 pageItr-V: (Please See Rule 12 of The Income-Tax Rules, 1962)deepakNo ratings yet

- Multiple Choice - Problems Part 1: A. Percentage TaxDocument8 pagesMultiple Choice - Problems Part 1: A. Percentage TaxheyheyNo ratings yet

- Acceptance Payment Form Estate Tax AmnestyDocument1 pageAcceptance Payment Form Estate Tax AmnestyAlvin III SiapianNo ratings yet

- CIR V Enron Subic Power CorporationDocument1 pageCIR V Enron Subic Power CorporationiciamadarangNo ratings yet

- Contoh Soal Laporan Arus KasDocument2 pagesContoh Soal Laporan Arus KasRidwanNo ratings yet

- Special Journals (Purchase) : Exercise 5.7Document12 pagesSpecial Journals (Purchase) : Exercise 5.7Claudette ClementeNo ratings yet

- Deutsche Bank V CIR DigestDocument2 pagesDeutsche Bank V CIR DigestJImlan Sahipa IsmaelNo ratings yet

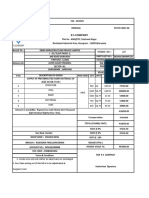

- Tax Invoice: United Squares PVT - Ltd. (Mumbai)Document1 pageTax Invoice: United Squares PVT - Ltd. (Mumbai)AthahNo ratings yet