You might also like

- The Twin Balance Sheet Problem: Submitted To Prof. S Shekhar Singh Prof. Chander MohanDocument19 pagesThe Twin Balance Sheet Problem: Submitted To Prof. S Shekhar Singh Prof. Chander MohanHarshit GoyalNo ratings yet

- A Blueprint for Prosperity: Market-based Alternatives to the Obama Blueprint for ChangeFrom EverandA Blueprint for Prosperity: Market-based Alternatives to the Obama Blueprint for ChangeNo ratings yet

- Rising Npas: Where Has All The Money Gone?: Ashok K LahiriDocument3 pagesRising Npas: Where Has All The Money Gone?: Ashok K LahiritatatssNo ratings yet

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesFrom EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesNo ratings yet

- Magnitude of Npas in Public Sector BanksDocument10 pagesMagnitude of Npas in Public Sector BanksMahesh PandeyNo ratings yet

- Banking Loans & NpaDocument22 pagesBanking Loans & NpamanjuNo ratings yet

- Key IssuesDocument7 pagesKey IssuesDhruv MehtaNo ratings yet

- Consolidated PPT Foundation 06.04.23Document764 pagesConsolidated PPT Foundation 06.04.23Tanay BansalNo ratings yet

- Twin Balance Effect AnalysisDocument23 pagesTwin Balance Effect AnalysisSumit kumarNo ratings yet

- BES171 Financial Inclusion1 Jandhan Small Savings SchemesDocument29 pagesBES171 Financial Inclusion1 Jandhan Small Savings Schemesroy lexterNo ratings yet

- Uday Kotak Letter PDFDocument3 pagesUday Kotak Letter PDFGurjeevNo ratings yet

- Mrunal EconomyDocument19 pagesMrunal EconomyJeevan KumarNo ratings yet

- Bhopal Branch of CIRC of ICAI: This Ediition SpecialDocument26 pagesBhopal Branch of CIRC of ICAI: This Ediition SpecialShrikrishna DwivediNo ratings yet

- Rajans Take On NPA CrisisDocument9 pagesRajans Take On NPA CrisisAkashNo ratings yet

- Class Lecture 17 To 20Document47 pagesClass Lecture 17 To 20Tanay BansalNo ratings yet

- CH-2 - NPAs, Its Emergence and EffectsDocument7 pagesCH-2 - NPAs, Its Emergence and EffectsNirjhar DuttaNo ratings yet

- Bes172 p4 Blackmoney 2 Demonetization Soil RateDocument40 pagesBes172 p4 Blackmoney 2 Demonetization Soil Rateroy lexterNo ratings yet

- Can The BRICS New Development Bank Compete With The World Bank and The IMFDocument6 pagesCan The BRICS New Development Bank Compete With The World Bank and The IMFThomas HafenNo ratings yet

- Non Performing AssetsDocument8 pagesNon Performing Assetsbhattcomputer3015No ratings yet

- MSVN - VN Banks - March Update - VCB in Focus - ThanhDocument45 pagesMSVN - VN Banks - March Update - VCB in Focus - ThanhphatNo ratings yet

- NPAs Cleaner of Banks or Killer of Indian Economy I NPA Account SettlementDocument2 pagesNPAs Cleaner of Banks or Killer of Indian Economy I NPA Account SettlementArshad ShaikhNo ratings yet

- Causes of NPADocument7 pagesCauses of NPAsggovardhan0% (1)

- NPA Management in Public Sector BanksDocument3 pagesNPA Management in Public Sector BanksBharath Kumar JNo ratings yet

- Axis Bank ProjectDocument11 pagesAxis Bank ProjectKuNaL HaJaReNo ratings yet

- Unit - 4:: Banking SystemDocument14 pagesUnit - 4:: Banking SystemsonuNo ratings yet

- Increased Importance of Credit Appraisal Process in Today'S Banking LandscapeDocument5 pagesIncreased Importance of Credit Appraisal Process in Today'S Banking LandscapeNishanth NichuNo ratings yet

- BES171 03 E-Payment-challanges REFORMS Mains AnswerwritingDocument56 pagesBES171 03 E-Payment-challanges REFORMS Mains AnswerwritingJayshree ChauhanNo ratings yet

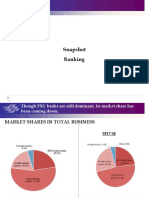

- Snapshot BankingDocument7 pagesSnapshot BankingAmit RajNo ratings yet

- 5 6089339537744461990 PDFDocument120 pages5 6089339537744461990 PDFGaurav SumanNo ratings yet

- Interest Rate Risk: Get QuoteDocument5 pagesInterest Rate Risk: Get Quoterini08No ratings yet

- BES171 00 Gist of Eco Survey 14 ChaptersDocument30 pagesBES171 00 Gist of Eco Survey 14 Chaptersjainrahul2910No ratings yet

- Edited NpaDocument22 pagesEdited NpaRushil ShahNo ratings yet

- Are Non - Performing Assets Gloomy or Greedy From Indian Perspective?Document9 pagesAre Non - Performing Assets Gloomy or Greedy From Indian Perspective?Mohit JainNo ratings yet

- Power Corporation of Canada Appoints New President & CEODocument1 pagePower Corporation of Canada Appoints New President & CEOGenieNo ratings yet

- 9777-Article Text-19152-1-10-20210824Document11 pages9777-Article Text-19152-1-10-20210824taggkarthooNo ratings yet

- Ibps Po Pre Practice Set Vijay Tripathi PDFDocument131 pagesIbps Po Pre Practice Set Vijay Tripathi PDFDuvva VenkateshNo ratings yet

- ICICI Securities NBFC Sector UpdateDocument7 pagesICICI Securities NBFC Sector UpdateDivy JainNo ratings yet

- FINM3006 Notes On Past Exams: 2016 Test 1Document77 pagesFINM3006 Notes On Past Exams: 2016 Test 1Navya VinnyNo ratings yet

- McKinsey Global Payments Map 2017Document24 pagesMcKinsey Global Payments Map 2017Senka AnđelkovićNo ratings yet

- Comparitive Analysis of Public and Private Sector Banks NPA-KotakDocument6 pagesComparitive Analysis of Public and Private Sector Banks NPA-KotakMohmmedKhayyumNo ratings yet

- FMI Updates 2021 MainsDocument13 pagesFMI Updates 2021 MainsGarima LohiaNo ratings yet

- Soumik Sen 12PGDM055 Section ADocument15 pagesSoumik Sen 12PGDM055 Section ASoumik SenNo ratings yet

- Parliamentary Note - Raghuram RajanDocument17 pagesParliamentary Note - Raghuram RajanThe Wire100% (22)

- Paper 1 PDFDocument3 pagesPaper 1 PDFWashim Alam50CNo ratings yet

- MARCH 2017: A Shankar IAS Academy InitiativeDocument30 pagesMARCH 2017: A Shankar IAS Academy InitiativeLaxmi Prasad IndiaNo ratings yet

- Privatisation: A Bad Solution For India's Banking ProblemsDocument4 pagesPrivatisation: A Bad Solution For India's Banking ProblemsMohammad yunusNo ratings yet

- Paper 3 TheoryDocument90 pagesPaper 3 TheoryAditya SuriNo ratings yet

- Paper 3Document90 pagesPaper 3NIVAAYA VlogsNo ratings yet

- 19 09 2021 Handwritten NotesDocument19 pages19 09 2021 Handwritten Notespraveen thadiNo ratings yet

- Shri Ramswaroop Memorial College of Engineering and ManagementDocument8 pagesShri Ramswaroop Memorial College of Engineering and ManagementPriya SinghNo ratings yet

- Banking Transactions, Digital PaymentDocument56 pagesBanking Transactions, Digital PaymentrudicoolousNo ratings yet

- Federal Bank LTD.: PCG ResearchDocument11 pagesFederal Bank LTD.: PCG Researcharun_algoNo ratings yet

- Yes BankDocument56 pagesYes BankPrabhjot kaurNo ratings yet

- Final Report-NPA - PRINT OUT3Document74 pagesFinal Report-NPA - PRINT OUT3shovit singh0% (2)

- Descriptive Answer Writing Lyst6832Document54 pagesDescriptive Answer Writing Lyst6832hanovesNo ratings yet

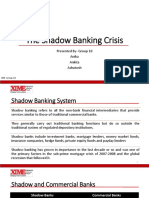

- The Shadow Banking CrisisDocument22 pagesThe Shadow Banking CrisisAnika goelNo ratings yet

- Term Paper On One BankDocument4 pagesTerm Paper On One Bankafmzubsbdcfffg100% (1)

- Tata Hungary 2024 04 08Document4 pagesTata Hungary 2024 04 08rudicoolousNo ratings yet

- Economy Survey: Who Prepares? How? Why Imp For Exam? Gist of 14 ChaptersDocument61 pagesEconomy Survey: Who Prepares? How? Why Imp For Exam? Gist of 14 ChaptersrudicoolousNo ratings yet

- Banking Transactions, Digital PaymentDocument56 pagesBanking Transactions, Digital PaymentrudicoolousNo ratings yet

- Post Demonetization - Bank Money & Digital PaymentDocument79 pagesPost Demonetization - Bank Money & Digital PaymentrudicoolousNo ratings yet

- India's Soft and Hard Power Strategy in Foreign PolicyDocument5 pagesIndia's Soft and Hard Power Strategy in Foreign Policyrudicoolous100% (1)

- FIDIC: Termination by The Employer Under The Red and Yellow BooksDocument8 pagesFIDIC: Termination by The Employer Under The Red and Yellow BookssaihereNo ratings yet

- Section 137 To 146aDocument11 pagesSection 137 To 146aSher DilNo ratings yet

- John Scott McKay Fraud on the Court McKay & Leong Walnut Creek Attorney J. Scott McKay Collusion-Conspiracy with Court Appointed Receiver Kevin Singer Alleged in Federal Class Action Lawsuit Charging Unauthorized Practice of Law Accessory-Aiding & Abetting by Lawyer Scott McKay - State Bar of California Jayne KimDocument493 pagesJohn Scott McKay Fraud on the Court McKay & Leong Walnut Creek Attorney J. Scott McKay Collusion-Conspiracy with Court Appointed Receiver Kevin Singer Alleged in Federal Class Action Lawsuit Charging Unauthorized Practice of Law Accessory-Aiding & Abetting by Lawyer Scott McKay - State Bar of California Jayne KimCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story Ideas100% (2)

- Financial DistressDocument12 pagesFinancial DistressLakshmiRengarajanNo ratings yet

- Financial Distress ResumeDocument2 pagesFinancial Distress ResumeTika Tety PratiwiNo ratings yet

- Harish Chandra Mishra and Deepak Roshan, JJ.: Equiv Alent Citation: (2020) 77GSTR174 (Jha.)Document10 pagesHarish Chandra Mishra and Deepak Roshan, JJ.: Equiv Alent Citation: (2020) 77GSTR174 (Jha.)nidhidaveNo ratings yet

- Finance Case StudyDocument8 pagesFinance Case StudyEvans MettoNo ratings yet

- PHS 3rd Cir Brief 12.6.10Document57 pagesPHS 3rd Cir Brief 12.6.10Maddie O'DoulNo ratings yet

- Money Recovery SuitDocument6 pagesMoney Recovery SuitShivani Prajapati100% (1)

- BLAW Online QuizzesDocument12 pagesBLAW Online QuizzesNhi Le100% (1)

- Corporate Law CD 2019-2020Document10 pagesCorporate Law CD 2019-2020jannnNo ratings yet

- IOB42986Chennai Circle Public NoticeDocument8 pagesIOB42986Chennai Circle Public Noticegangapuram aravindNo ratings yet

- Predicting The Risk of Corporate FailureDocument330 pagesPredicting The Risk of Corporate FailureAngus SadpetNo ratings yet

- StrtsmanDocument213 pagesStrtsmancarolina1956No ratings yet

- Borders BankruptcyDocument10 pagesBorders BankruptcyJill PiccioneNo ratings yet

- MemorialDocument26 pagesMemorialMandira PrakashNo ratings yet

- The Trade Credit ClearinghouseDocument91 pagesThe Trade Credit ClearinghouseJurica ZRncNo ratings yet

- Central University of South Bihar: School of Law and Governance Contract-IiDocument19 pagesCentral University of South Bihar: School of Law and Governance Contract-IiShashank PathakNo ratings yet

- Aligarh Muslim University Malappuram CentreDocument8 pagesAligarh Muslim University Malappuram CentreÀbdul SamadNo ratings yet

- Cases FRIADocument8 pagesCases FRIAMartel John MiloNo ratings yet

- 1st Edition - NCLAT Judgement SummaryDocument29 pages1st Edition - NCLAT Judgement SummaryAarti singhNo ratings yet

- Involuntary Insolvency: Least Sixty (60) Days or That The Debtor Has Failed Generally To Meet Its LiabilitiesDocument49 pagesInvoluntary Insolvency: Least Sixty (60) Days or That The Debtor Has Failed Generally To Meet Its LiabilitiesDonna DelgadoNo ratings yet

- Loan Recovery StrategyDocument7 pagesLoan Recovery Strategyrecovery cellNo ratings yet

- Bankruptcy Due To Credit Card Debts Young Executives FinanceDocument4 pagesBankruptcy Due To Credit Card Debts Young Executives FinanceSophia RusliNo ratings yet

- Team Code 3Document143 pagesTeam Code 3alam amarNo ratings yet

- Case DigestsDocument107 pagesCase DigestsJohanna ArnaezNo ratings yet

- Giannasca Supp MM As Filed 03-18-2020 2Document78 pagesGiannasca Supp MM As Filed 03-18-2020 2RussinatorNo ratings yet

- DBP v. NLRC, 186 SCRA 841 (1990)Document19 pagesDBP v. NLRC, 186 SCRA 841 (1990)inno KalNo ratings yet

- Final Law Vol-2 PDFDocument326 pagesFinal Law Vol-2 PDFMonty SharmaNo ratings yet

- United States Bankruptcy Court Southern District of New YorkDocument12 pagesUnited States Bankruptcy Court Southern District of New YorkMike McSweeneyNo ratings yet