You might also like

- An MBA in a Book: Everything You Need to Know to Master Business - In One Book!From EverandAn MBA in a Book: Everything You Need to Know to Master Business - In One Book!No ratings yet

- IENG4318 Project Management - W2 - 2Document16 pagesIENG4318 Project Management - W2 - 2wira_rediNo ratings yet

- End of Chapter Exercises - AnswersDocument4 pagesEnd of Chapter Exercises - AnswersYvonneNo ratings yet

- Other Investment Criteria and Free Cash Flows in Finance: Capital Budgeting DecisionsDocument48 pagesOther Investment Criteria and Free Cash Flows in Finance: Capital Budgeting DecisionsAbdullah MujahidNo ratings yet

- What Project Will You Sugggest To The Management and Why?Document8 pagesWhat Project Will You Sugggest To The Management and Why?Tin Bernadette DominicoNo ratings yet

- Net Present Value: First Principles of FinanceDocument14 pagesNet Present Value: First Principles of FinanceandresugiNo ratings yet

- Energy - 1 IntroductionDocument16 pagesEnergy - 1 IntroductionMostafa Ayman Mohammed NageebNo ratings yet

- Chapter Ten: Making Capital Investment DecisionDocument34 pagesChapter Ten: Making Capital Investment DecisionRehman LaljiNo ratings yet

- Reading 7: Discounted Cash Flow ApplicationsDocument17 pagesReading 7: Discounted Cash Flow ApplicationsAndy Thibault-MilksNo ratings yet

- Ch11 ShowDocument63 pagesCh11 ShowMahmoud AbdullahNo ratings yet

- NPV Formula EXAMPLEDocument13 pagesNPV Formula EXAMPLEVongayi KuchekwaNo ratings yet

- Review For Midterm (Project Mana) 102021Document37 pagesReview For Midterm (Project Mana) 102021Tam MinhNo ratings yet

- Capital Budgeting TechniquesDocument26 pagesCapital Budgeting TechniquesSyedMohammadHashaamPirzadaNo ratings yet

- Topic 1-PV, FV, Annunities, Perpetuities - No SolutionsDocument47 pagesTopic 1-PV, FV, Annunities, Perpetuities - No SolutionsJorge Alberto HerreraNo ratings yet

- Up Chapter 6-7 (1) - 2 (Compatibility Mode)Document39 pagesUp Chapter 6-7 (1) - 2 (Compatibility Mode)EftaNo ratings yet

- Managerial Economics (Chapter 14)Document28 pagesManagerial Economics (Chapter 14)api-3703724100% (1)

- BFW2140 Lecture Week 2: Corporate Financial Mathematics IDocument33 pagesBFW2140 Lecture Week 2: Corporate Financial Mathematics Iaa TANNo ratings yet

- Financial Management 4Document41 pagesFinancial Management 4geachew mihiretu0% (1)

- MS 602 - Lec - Capital BudgetingDocument52 pagesMS 602 - Lec - Capital BudgetingGEORGENo ratings yet

- Team Project 2: Chapter 8: Investment Decision Rules Fundamentals of Capital BudgetingDocument61 pagesTeam Project 2: Chapter 8: Investment Decision Rules Fundamentals of Capital BudgetingБекФорд ЗакNo ratings yet

- 7330 Lecture 02.1 Capital Budgeting Complications F10Document37 pages7330 Lecture 02.1 Capital Budgeting Complications F10parnamunnaNo ratings yet

- Discounted Cash Flow ValuationDocument35 pagesDiscounted Cash Flow ValuationRemonNo ratings yet

- Capital and Financial Markets ExplainedDocument41 pagesCapital and Financial Markets ExplainedArgha MondalNo ratings yet

- Cash Flow Estimation and Risk Analysis: by Dr. Yi ZhangDocument35 pagesCash Flow Estimation and Risk Analysis: by Dr. Yi ZhangBibi KathNo ratings yet

- S4. Capital BudgetingDocument36 pagesS4. Capital BudgetingGenesis mia Albornoz ochoaNo ratings yet

- Cash Flows and Other Topics in Capital BudgetingDocument63 pagesCash Flows and Other Topics in Capital BudgetingShaina Rosewell M. VillarazoNo ratings yet

- Lecture 27 Rate of Return AnalysisDocument32 pagesLecture 27 Rate of Return AnalysisDevyansh GuptaNo ratings yet

- Capital Budgeting: Project Selection Exercise Performed by The Business EnterpriseDocument20 pagesCapital Budgeting: Project Selection Exercise Performed by The Business EnterpriseNeha UpadhyayNo ratings yet

- FIN3001 Present Value RecapDocument26 pagesFIN3001 Present Value RecapManton YeungNo ratings yet

- Chapter 8 Net Present Value and Other Investment CriteriaDocument33 pagesChapter 8 Net Present Value and Other Investment CriteriaPaul Adrian BalascanNo ratings yet

- Year Project X Project Y 0 $ (10,000) $ (10,000) 1 $6,500 $3,500 2 $3,000 $3,500 3 $3,000 $3,500 4 $1,000 $3,500Document3 pagesYear Project X Project Y 0 $ (10,000) $ (10,000) 1 $6,500 $3,500 2 $3,000 $3,500 3 $3,000 $3,500 4 $1,000 $3,500Idris100% (1)

- Valuation of BondsDocument46 pagesValuation of BondsRajesh K. PedhaviNo ratings yet

- Time Value of MoneyDocument15 pagesTime Value of MoneyJann Aldrin PulaNo ratings yet

- Chapter 7Document39 pagesChapter 7Indriati ArisaNo ratings yet

- Long-Term Investment DecisionsDocument28 pagesLong-Term Investment DecisionsJonathan LimNo ratings yet

- Cash Flow Brigham SolutionDocument14 pagesCash Flow Brigham SolutionShahid Mehmood100% (4)

- Slides FM s4s5Document31 pagesSlides FM s4s5Amartya KumarNo ratings yet

- Investment Decision CriteriaDocument44 pagesInvestment Decision CriteriaThu Võ ThịNo ratings yet

- More On Capital BudgetingDocument56 pagesMore On Capital BudgetingnewaznahianNo ratings yet

- Profitability AnalysisDocument24 pagesProfitability AnalysisAnonymous 1P14SXhUNo ratings yet

- Chapter 05 Net Present Value and Other Investment Rules PDFDocument35 pagesChapter 05 Net Present Value and Other Investment Rules PDFWan Maulana AkbarNo ratings yet

- AFM QB 2024 - FinalDocument621 pagesAFM QB 2024 - Final74ef8465d65d1bNo ratings yet

- Financial Analysis of ProjectsDocument61 pagesFinancial Analysis of ProjectsMohamed MustefaNo ratings yet

- Please help John Shell to evaluate these two projects using payback period method. Which project should he chooseDocument42 pagesPlease help John Shell to evaluate these two projects using payback period method. Which project should he chooseLoureine Patricia SumualNo ratings yet

- Capital Budgeting Techniques AnalysisDocument33 pagesCapital Budgeting Techniques Analysistahir khanNo ratings yet

- Topic3 InvestmentRulesDocument41 pagesTopic3 InvestmentRulesБота ОмароваNo ratings yet

- Chapter 5 Present Worth AnalysisDocument82 pagesChapter 5 Present Worth Analysisيوسف محمدNo ratings yet

- NPV Comparison of Investment OptionsDocument4 pagesNPV Comparison of Investment OptionsБота ОмароваNo ratings yet

- Session 14-Capital Budgeting and RiskDocument22 pagesSession 14-Capital Budgeting and RiskNANCY BANSALNo ratings yet

- Cash Flow PDFDocument37 pagesCash Flow PDFGiri SukumarNo ratings yet

- Capital BudgetingDocument67 pagesCapital BudgetingAhmad VohraNo ratings yet

- Lecture Notes T01Document9 pagesLecture Notes T01Learning PointNo ratings yet

- Cash Flow and Capital BudgetingDocument37 pagesCash Flow and Capital BudgetingASIFNo ratings yet

- Time Value of MoneyDocument43 pagesTime Value of Moneym.gerryNo ratings yet

- Time Value of Money and Capital Budgeting Techniques: By: Waqas Siddique SammaDocument84 pagesTime Value of Money and Capital Budgeting Techniques: By: Waqas Siddique SammaWaqas Siddique SammaNo ratings yet

- lpv13 6 RDocument18 pageslpv13 6 RPhan Hải YếnNo ratings yet

- Chapter Two: Consumption, Investment and Capital BudgetingDocument28 pagesChapter Two: Consumption, Investment and Capital Budgetingejara gelmechaNo ratings yet

- Ins3007 S4 SVDocument32 pagesIns3007 S4 SVnguyễnthùy dươngNo ratings yet

- WORK 1004: Foundations of Management: Lecture 4 - Management and TeamworkDocument21 pagesWORK 1004: Foundations of Management: Lecture 4 - Management and Teamworkharshit guptaNo ratings yet

- Vehicle Routing Problems - HandoutDocument10 pagesVehicle Routing Problems - Handoutharshit guptaNo ratings yet

- WORK 1004 Foundations of Management: Week 1 - IntroductionDocument60 pagesWORK 1004 Foundations of Management: Week 1 - Introductionharshit guptaNo ratings yet

- Lecture 1 - Best LT InvestmentDocument26 pagesLecture 1 - Best LT Investmentharshit guptaNo ratings yet

- WORK 1004 Foundations of Management: Lecture 6 - Managerial Planning and Decision-MakingDocument52 pagesWORK 1004 Foundations of Management: Lecture 6 - Managerial Planning and Decision-Makingharshit guptaNo ratings yet

- Live Weekly Class 3 - COMM121 - PortalDocument5 pagesLive Weekly Class 3 - COMM121 - Portalharshit guptaNo ratings yet

- Introduction To Finance: Blair RobertsonDocument37 pagesIntroduction To Finance: Blair Robertsonharshit guptaNo ratings yet

- Finance Class Overview and Market InsightsDocument14 pagesFinance Class Overview and Market Insightsharshit guptaNo ratings yet

- Live Weekly Class 3 - COMM121 - PortalDocument5 pagesLive Weekly Class 3 - COMM121 - Portalharshit guptaNo ratings yet

- Introduction To Finance: Blair RobertsonDocument32 pagesIntroduction To Finance: Blair Robertsonharshit guptaNo ratings yet

- REFLECTION-PAPER-BA233N-forex MarketDocument6 pagesREFLECTION-PAPER-BA233N-forex MarketJoya Labao Macario-BalquinNo ratings yet

- Tutorial 3 AnswersDocument7 pagesTutorial 3 AnswersFEI FEINo ratings yet

- Lee HW2Document7 pagesLee HW2Cheska LeeNo ratings yet

- Fin625 Assignment - Securitization Process and PartiesDocument3 pagesFin625 Assignment - Securitization Process and PartiesEntertainment StatusNo ratings yet

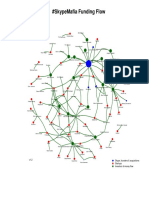

- SkypeMafia Funding Flow ChartDocument1 pageSkypeMafia Funding Flow ChartMarius Cristian IspasNo ratings yet

- CB Insights 2020 AI 100 Startups: Company Sector Focus AreaDocument12 pagesCB Insights 2020 AI 100 Startups: Company Sector Focus AreaAnishNo ratings yet

- Accountancy Notes PDF Class 12 Chapter 2Document4 pagesAccountancy Notes PDF Class 12 Chapter 2Miss Palak.kNo ratings yet

- Allied Bank's Objectives and OverviewDocument69 pagesAllied Bank's Objectives and OverviewAdil MuradNo ratings yet

- Class 10 History CH 4Document8 pagesClass 10 History CH 4Jeff BejosNo ratings yet

- Aes Case SolutionDocument3 pagesAes Case SolutionXimenaLopezCifuentes100% (1)

- The Knowledge ToolboxDocument13 pagesThe Knowledge ToolboxJoham GutierrezNo ratings yet

- TATA Motors Fundamental AnalysisDocument17 pagesTATA Motors Fundamental AnalysisMitali AgrawalNo ratings yet

- August 25, 2022 (Spec. Trans.)Document4 pagesAugust 25, 2022 (Spec. Trans.)The Brain Dump PHNo ratings yet

- Annual Turkish Ma Review January 2017 FinalDocument36 pagesAnnual Turkish Ma Review January 2017 FinalOsman Murat TütüncüNo ratings yet

- Apple Stock BuybackDocument2 pagesApple Stock BuybackalimithaNo ratings yet

- Financing in StartupDocument5 pagesFinancing in StartupKaran Raj DeoNo ratings yet

- The FVA - Forward Volatility AgreementDocument9 pagesThe FVA - Forward Volatility Agreementshih_kaichih100% (1)

- 2.4 Ishares Product List PDFDocument12 pages2.4 Ishares Product List PDFVijay YadavNo ratings yet

- Financial Statement Spreading - Pre Process ManualDocument2 pagesFinancial Statement Spreading - Pre Process ManualChandan Kumar ShawNo ratings yet

- Itc Subsidiaries 2011 CompleteDocument199 pagesItc Subsidiaries 2011 Completevisheshkotha3009No ratings yet

- Dang Nhu VanDocument30 pagesDang Nhu Vananonymousninjat100% (1)

- Diluted EPS NotesDocument7 pagesDiluted EPS NotesArchana DevdasNo ratings yet

- SecuritisationDocument11 pagesSecuritisationSailesh RoutNo ratings yet

- Bond Retirement Prior To Maturity A. Illustration 1 - Straight LineDocument27 pagesBond Retirement Prior To Maturity A. Illustration 1 - Straight Linephoebelyn acdogNo ratings yet

- Financial Management Assignment on HCL TechnologiesDocument21 pagesFinancial Management Assignment on HCL TechnologiesSudeepNo ratings yet

- BDA Advises Hyster-Yale On Agreement To Acquire 75% of Zhejiang Maximal Forklift Truck, ChinaDocument3 pagesBDA Advises Hyster-Yale On Agreement To Acquire 75% of Zhejiang Maximal Forklift Truck, ChinaPR.comNo ratings yet

- Rahman.S, Askari.H: An Economic Islamicity IndexDocument39 pagesRahman.S, Askari.H: An Economic Islamicity IndexShahzeb AtiqNo ratings yet

- Credit Suisse Global Investment Returns Yearbook 2022 Summary EditionDocument50 pagesCredit Suisse Global Investment Returns Yearbook 2022 Summary EditionRanty100% (1)

- Cricket BallDocument37 pagesCricket BallSanjaylalkiyaNo ratings yet