You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- Break Even AnalysisDocument12 pagesBreak Even AnalysisnamanNo ratings yet

- Acn 4Document3 pagesAcn 4Navidul IslamNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- Illustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesDocument4 pagesIllustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesGabriel BelmonteNo ratings yet

- Break Even Point For Chart A Single Product: RecapitulationDocument3 pagesBreak Even Point For Chart A Single Product: Recapitulationhusse fokNo ratings yet

- Chapter 22Document14 pagesChapter 22Nguyên BảoNo ratings yet

- ExerciseDocument7 pagesExercisekarthikNo ratings yet

- DR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingDocument6 pagesDR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingSaumya JainNo ratings yet

- Absorption Costing QuestionsDocument6 pagesAbsorption Costing Questions田淼No ratings yet

- Practical Problems & Solutions Class Work Upto IL.10Document20 pagesPractical Problems & Solutions Class Work Upto IL.10Dhanishta PramodNo ratings yet

- Master Minds CA/CWA & MEC/CEC marginal costing solutionsDocument14 pagesMaster Minds CA/CWA & MEC/CEC marginal costing solutionsHaresh KNo ratings yet

- 15 Marginal Costing PDFDocument14 pages15 Marginal Costing PDFSupriyoNo ratings yet

- Chapter # 8 Exercise & Problems - AnswersDocument8 pagesChapter # 8 Exercise & Problems - AnswersZia UddinNo ratings yet

- Belva Athaya Alzena - 1401194459 - LATIHAN LAB OMDocument6 pagesBelva Athaya Alzena - 1401194459 - LATIHAN LAB OMBelva Athaya AlzenaNo ratings yet

- Denton Company Income Statement Periode 1 - July, 2020Document4 pagesDenton Company Income Statement Periode 1 - July, 2020Farrell FerenceNo ratings yet

- Week3 With SolutionsDocument8 pagesWeek3 With SolutionsAaliya & FaizNo ratings yet

- Unit -4Document26 pagesUnit -4MOHAIDEEN THARIQ MNo ratings yet

- Assign 6 Chapter 8 Operating and Financial Leverage Cabrera 2019-2020Document12 pagesAssign 6 Chapter 8 Operating and Financial Leverage Cabrera 2019-2020mhikeedelantar100% (1)

- PRACTICAL CASES 28 and 29Document5 pagesPRACTICAL CASES 28 and 29loliNo ratings yet

- Examples FMA - 5Document10 pagesExamples FMA - 5DaddyNo ratings yet

- Problem 2-14 Product Cost Sunk Cost Direct LaborDocument8 pagesProblem 2-14 Product Cost Sunk Cost Direct LaborarijitmajeeNo ratings yet

- CAC - COMPUTATIONS analysisDocument9 pagesCAC - COMPUTATIONS analysisrochelle lagmayNo ratings yet

- Mcom QP Amd 40 MarksDocument2 pagesMcom QP Amd 40 Marksirfanahmed.dbaNo ratings yet

- CVP ANALYSIS BREAK-EVEN POINT MULTI-PRODUCTDocument40 pagesCVP ANALYSIS BREAK-EVEN POINT MULTI-PRODUCTRajguru JavalagaddiNo ratings yet

- Accounts Assignment 104Document6 pagesAccounts Assignment 104busybeefreedomNo ratings yet

- MBA 2020 Cost Management Session 6Document42 pagesMBA 2020 Cost Management Session 6Abhishek BaruaNo ratings yet

- TUT 3 - Relevant Information&decision MakingDocument10 pagesTUT 3 - Relevant Information&decision MakingKim Chi LeNo ratings yet

- ACCA F5 Class NotesDocument177 pagesACCA F5 Class NotesAzeezNo ratings yet

- MGT Acc 2019 SolutionDocument9 pagesMGT Acc 2019 SolutionSayeed AhmadNo ratings yet

- MGT Acc 2019 SolutionDocument9 pagesMGT Acc 2019 SolutionSayeed AhmadNo ratings yet

- Cost-Volume-Profit (CVP) Analysis Template: Strictly ConfidentialDocument4 pagesCost-Volume-Profit (CVP) Analysis Template: Strictly Confidentialterhua11100% (1)

- Chapter-9: Cost-Volume-Profit Analysis (CVP)Document54 pagesChapter-9: Cost-Volume-Profit Analysis (CVP)selamawitNo ratings yet

- Accounting Chapter 06 Full SolutionDocument15 pagesAccounting Chapter 06 Full SolutionAsadullahil GalibNo ratings yet

- Chapter S7: Example S3: Breakeven AnalysisDocument1 pageChapter S7: Example S3: Breakeven AnalysisJonathan GutierrezNo ratings yet

- CVP AnalysisDocument40 pagesCVP Analysissbjafri0No ratings yet

- Cost Accounting & Financial Management Solved Paper Nov 2009, Chartered AccountancyDocument16 pagesCost Accounting & Financial Management Solved Paper Nov 2009, Chartered AccountancyAnkit2020No ratings yet

- Break-Even Occurs Between The Production Volume Interval of 20,000 To 30,000Document6 pagesBreak-Even Occurs Between The Production Volume Interval of 20,000 To 30,000kripsNo ratings yet

- Jawaban No 4Document2 pagesJawaban No 4diaheka1712No ratings yet

- CVP Analysis 2 Amp Ratios ExcelDocument53 pagesCVP Analysis 2 Amp Ratios ExcelSoahNo ratings yet

- Module 3 Practice Problems(2)Document13 pagesModule 3 Practice Problems(2)Liza Mae MirandaNo ratings yet

- Salvage Value Useful Life Accumulated YearsDocument10 pagesSalvage Value Useful Life Accumulated Yearsmiljane perdizoNo ratings yet

- Activity 11Document3 pagesActivity 11UchayyaNo ratings yet

- Solutions Chapter 5Document13 pagesSolutions Chapter 5Laila Al Suwaidi100% (2)

- Capital Investment/Net Present Value: Interest Rate DataDocument9 pagesCapital Investment/Net Present Value: Interest Rate DataWILLAM FABIAN PASTUÑA CAISAGUANONo ratings yet

- Lemon trader's profit and P/V ratio calculationDocument109 pagesLemon trader's profit and P/V ratio calculationARPIT GILRANo ratings yet

- I-CVP Analysis For Break-Even PlanningDocument10 pagesI-CVP Analysis For Break-Even PlanningNeshia May BariquitNo ratings yet

- 4 and 5Document3 pages4 and 5Mela carlonNo ratings yet

- Business P4 Act1Document5 pagesBusiness P4 Act1AlejandroNo ratings yet

- Cost Management Anudeep Velagapudi PGDM6 1967Document9 pagesCost Management Anudeep Velagapudi PGDM6 1967Harsh Vardhan SinghNo ratings yet

- Midterms MADocument10 pagesMidterms MAJustz LimNo ratings yet

- Basic Finantial PlanDocument1 pageBasic Finantial Plansher lyyNo ratings yet

- Chapter 4 PDFDocument33 pagesChapter 4 PDFAdda KadhilaNo ratings yet

- M03Document4 pagesM03Anne Thea AtienzaNo ratings yet

- 20123400024Document7 pages20123400024Phạm Công KiênNo ratings yet

- Problem 1: Cost Volume Profit RelationshipsDocument22 pagesProblem 1: Cost Volume Profit RelationshipsNamir RafiqNo ratings yet

- Sba SemDocument9 pagesSba SemChelsa Mae AntonioNo ratings yet

- Course Code: ACT 201 Course Title: Cost & Management Accounting Section: 2Document4 pagesCourse Code: ACT 201 Course Title: Cost & Management Accounting Section: 2Wild GhostNo ratings yet

- Charlote Rep. FINANCIAL RISK MANAGEMENTDocument18 pagesCharlote Rep. FINANCIAL RISK MANAGEMENTJeanette FormenteraNo ratings yet

- Cpa Exam Blueprints Effective Jan 2019 PDFDocument101 pagesCpa Exam Blueprints Effective Jan 2019 PDFPaul GeorgeNo ratings yet

- Children Holy TrinityDocument214 pagesChildren Holy TrinityJeanette FormenteraNo ratings yet

- Chapter 2.1 ClassificationofRocksDocument32 pagesChapter 2.1 ClassificationofRocksJeanette FormenteraNo ratings yet

- Midt - Chapter9Bianca M&ADocument44 pagesMidt - Chapter9Bianca M&AJeanette FormenteraNo ratings yet

- SUN, ENG., 1st Sunday of Advent, Nov. 30, 2014Document161 pagesSUN, ENG., 1st Sunday of Advent, Nov. 30, 2014Jeanette FormenteraNo ratings yet

- SUN, TAG, 23rd Sunday in Ordinary Time, St. JamesDocument219 pagesSUN, TAG, 23rd Sunday in Ordinary Time, St. JamesJeanette FormenteraNo ratings yet

- Chap.6 Bianca Rep. FinMan2 - Long Term InvestmentsDocument60 pagesChap.6 Bianca Rep. FinMan2 - Long Term InvestmentsJeanette FormenteraNo ratings yet

- Cause and Effect EssayDocument23 pagesCause and Effect EssayJeanette FormenteraNo ratings yet

- St. James SUN, 14th Sunday in OT July 5, 2015Document222 pagesSt. James SUN, 14th Sunday in OT July 5, 2015Jeanette FormenteraNo ratings yet

- Sr. Jen MAS Chap.25Document22 pagesSr. Jen MAS Chap.25Jeanette FormenteraNo ratings yet

- Chap. 4 COST OF CAPITALDocument35 pagesChap. 4 COST OF CAPITALJeanette FormenteraNo ratings yet

- Parts of The Mass PowerpointDocument34 pagesParts of The Mass PowerpointJeanette Formentera100% (1)

- All Souls Day 2Document187 pagesAll Souls Day 2Jeanette FormenteraNo ratings yet

- Feast of St. Clare Mass HighlightsDocument80 pagesFeast of St. Clare Mass HighlightsJeanette FormenteraNo ratings yet

- 29th SunDocument221 pages29th SunJeanette FormenteraNo ratings yet

- 1st SunDocument224 pages1st SunJeanette FormenteraNo ratings yet

- Chap.5 FINANCIAL ASSET ValuationDocument39 pagesChap.5 FINANCIAL ASSET ValuationJeanette FormenteraNo ratings yet

- FIRST COMMUNION 2020.pptx UpdatedDocument170 pagesFIRST COMMUNION 2020.pptx UpdatedJeanette FormenteraNo ratings yet

- FIRST COMMUNION 2020.pptx UpdatedDocument170 pagesFIRST COMMUNION 2020.pptx UpdatedJeanette FormenteraNo ratings yet

- LogicDocument76 pagesLogicAurangzeb ChaudharyNo ratings yet

- College Christmas Party GamesDocument5 pagesCollege Christmas Party GamesJeanette FormenteraNo ratings yet

- A philosophical basis for valuationDocument87 pagesA philosophical basis for valuationaugustoNo ratings yet

- Chap.5 FINANCIAL ASSET ValuationDocument39 pagesChap.5 FINANCIAL ASSET ValuationJeanette FormenteraNo ratings yet

- Gr.1 Report Hedging Foreign CurrencyDocument54 pagesGr.1 Report Hedging Foreign CurrencyJeanette FormenteraNo ratings yet

- Jose Rizal ReportDocument73 pagesJose Rizal ReportJeanette FormenteraNo ratings yet

- Liturgy and Liturgical SeasonDocument40 pagesLiturgy and Liturgical SeasonJeanette FormenteraNo ratings yet

- Palestine During The Time of Jesus (Sea of Galilee, Jordan River, Jerusalem)Document23 pagesPalestine During The Time of Jesus (Sea of Galilee, Jordan River, Jerusalem)Jeanette FormenteraNo ratings yet

- 1st Part Group 2 Report Comparison & ContrastDocument22 pages1st Part Group 2 Report Comparison & ContrastJeanette FormenteraNo ratings yet

- Life Insurance ProductsDocument43 pagesLife Insurance ProductsinvaapNo ratings yet

- Tugas Komputer AkuntansiDocument4 pagesTugas Komputer AkuntansiDwi RanggaNo ratings yet

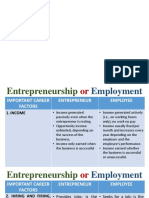

- Choosing Between Entrepreneurship and EmploymentDocument9 pagesChoosing Between Entrepreneurship and EmploymentMa Melissa Nacario SanPedroNo ratings yet

- Income Tax: General Principles: Module No. 4Document4 pagesIncome Tax: General Principles: Module No. 4Jay Lord Floresca100% (1)

- Issued Through Nsureplus Application SoftwareDocument1 pageIssued Through Nsureplus Application SoftwaresureshNo ratings yet

- Vietnam's Exchange Rate Regime Transition Since 1999Document12 pagesVietnam's Exchange Rate Regime Transition Since 1999wikileaks30No ratings yet

- The Global Capitalist Crisis:: Its Origins, Nature and ImpactDocument45 pagesThe Global Capitalist Crisis:: Its Origins, Nature and Impactanmol149No ratings yet

- RFM Corp Annual ReportDocument169 pagesRFM Corp Annual ReportGab RielNo ratings yet

- HH HDocument2 pagesHH HPrashant UpadhyayNo ratings yet

- 1 9th Social Sura Guide 2019 2020 Sample Materials Tamil MediumDocument101 pages1 9th Social Sura Guide 2019 2020 Sample Materials Tamil Mediumn.ananthapadmanabhanNo ratings yet

- Sensitivity AnalysisDocument23 pagesSensitivity AnalysisKamrul Hasan0% (1)

- Getting Paid Math 2.3.9.A1Document3 pagesGetting Paid Math 2.3.9.A1Aethan King AveNo ratings yet

- 2018 March B.com CBCSS Fifth Sem Special Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Document4 pages2018 March B.com CBCSS Fifth Sem Special Accounting Question Paper Goodwill Tuition Centre Thevara 9846710963 9567902805Rainy GoodwillNo ratings yet

- APSFC Application Fee Challan FormDocument1 pageAPSFC Application Fee Challan Formapr12_86No ratings yet

- Contract of Loan Inter AffiliateDocument3 pagesContract of Loan Inter Affiliatealexandro_novora6396No ratings yet

- Unit 1.3 Enterprise, Business Growth and SizeDocument3 pagesUnit 1.3 Enterprise, Business Growth and SizegretNo ratings yet

- Investment Centers and Transfer PricingDocument52 pagesInvestment Centers and Transfer Pricinganup akasheNo ratings yet

- Alert Company S Shareholders Equity Prior To Any of The Following PDFDocument1 pageAlert Company S Shareholders Equity Prior To Any of The Following PDFHassan JanNo ratings yet

- Gurukripa’s Guide to Nov 2014 CA Final SFM ExamDocument12 pagesGurukripa’s Guide to Nov 2014 CA Final SFM ExamShashank SharmaNo ratings yet

- VC Introduction and Players OverviewDocument35 pagesVC Introduction and Players Overviewblake0528100% (1)

- Top Glove Financial AssignmentDocument23 pagesTop Glove Financial Assignmentnigina2lips100% (1)

- Sonali JoshiDocument71 pagesSonali JoshiSonali Joshi100% (1)

- ACCT 101 Chapter 1 HandoutDocument3 pagesACCT 101 Chapter 1 HandoutLlana RoxanneNo ratings yet

- ALGOGENE - A Trend Following Strategy Based On Volatility ApproachDocument7 pagesALGOGENE - A Trend Following Strategy Based On Volatility Approachde deNo ratings yet

- Tano Santos Value Investing MBA Spring 2023 1stversion Term ADocument11 pagesTano Santos Value Investing MBA Spring 2023 1stversion Term AUddeshya GoelNo ratings yet

- New BankDocument13 pagesNew BankVelayudhan SunkaraNo ratings yet

- Case2.Bill MillerDocument3 pagesCase2.Bill Millercalvin100% (1)

- Securities and Exchange Board of IndiaDocument20 pagesSecurities and Exchange Board of IndiaShashank50% (2)

- Chapter 15 Using Management and Accounting InformationDocument22 pagesChapter 15 Using Management and Accounting InformationPete JoempraditwongNo ratings yet

- Investment Banking Deal ProcessDocument25 pagesInvestment Banking Deal Processdkgrinder100% (1)