You might also like

- Other Comprehensive Income - 2022Document2 pagesOther Comprehensive Income - 2022AireyNo ratings yet

- Pretest Post TestDocument40 pagesPretest Post TestAireyNo ratings yet

- IFRS 16 - Sale and LeasebackDocument2 pagesIFRS 16 - Sale and LeasebackAireyNo ratings yet

- Financial Report-1Document1 pageFinancial Report-1AireyNo ratings yet

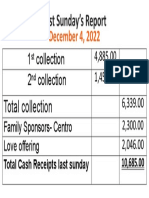

- 2 CollectionDocument1 page2 CollectionAireyNo ratings yet

- Financial ReportDocument1 pageFinancial ReportAireyNo ratings yet

- Theoretical FrameworkDocument6 pagesTheoretical FrameworkAireyNo ratings yet

- John Mark D. Terante Activity 3.1 1. Planting A Garden and Having A Family. 2. SimilarDocument3 pagesJohn Mark D. Terante Activity 3.1 1. Planting A Garden and Having A Family. 2. SimilarAireyNo ratings yet

- Defined Benefit PlanDocument6 pagesDefined Benefit PlanAireyNo ratings yet

- Aireyca Glenn G. Lanaban Bsa-3 WTH 5:15Pm-6:45 PMDocument2 pagesAireyca Glenn G. Lanaban Bsa-3 WTH 5:15Pm-6:45 PMAireyNo ratings yet

- Lanaban, Midterm Government AccountingDocument4 pagesLanaban, Midterm Government AccountingAireyNo ratings yet

- Acquaintance Party: College of Accounting EducationDocument2 pagesAcquaintance Party: College of Accounting EducationAireyNo ratings yet

- Revenue CycleDocument3 pagesRevenue CycleAireyNo ratings yet

- (After Aning Naa Sa Above Na Slide Glenny I Insert Ni:) : Example 1Document3 pages(After Aning Naa Sa Above Na Slide Glenny I Insert Ni:) : Example 1AireyNo ratings yet

- ABM 1 - Module 2 Assessment Name: SectionDocument1 pageABM 1 - Module 2 Assessment Name: SectionAireyNo ratings yet

- Cuses, Issues, Impact-Final OuputDocument2 pagesCuses, Issues, Impact-Final OuputAireyNo ratings yet

- T-Test: T-TEST PAIRS Radial WITH Belted (PAIRED) /CRITERIA CI (.9500) /missing AnalysisDocument2 pagesT-Test: T-TEST PAIRS Radial WITH Belted (PAIRED) /CRITERIA CI (.9500) /missing AnalysisAireyNo ratings yet

- A Vocation For EveryoneDocument2 pagesA Vocation For EveryoneAireyNo ratings yet

- Lanaban, Journal 1 ReflectionDocument2 pagesLanaban, Journal 1 ReflectionAireyNo ratings yet

- San Vicente Ferrer Quasi Parish Statement of Cash Flow For The Fiscal Year Ended August 31, 2019Document2 pagesSan Vicente Ferrer Quasi Parish Statement of Cash Flow For The Fiscal Year Ended August 31, 2019AireyNo ratings yet

- Assumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceDocument4 pagesAssumption College of Nabunturan: Nabunturan, Compostela Valley ProvinceAireyNo ratings yet

- Revised Standard Chart of Accounts For Cooperatives: Account Code Account TitleDocument36 pagesRevised Standard Chart of Accounts For Cooperatives: Account Code Account TitleAireyNo ratings yet

- BUS LAW 103 AssignmentDocument4 pagesBUS LAW 103 AssignmentAireyNo ratings yet

- What Are The Kinds of Bill of Exchange?Document3 pagesWhat Are The Kinds of Bill of Exchange?AireyNo ratings yet

- Cuses, Issues, Impact-Final OuputDocument2 pagesCuses, Issues, Impact-Final OuputAireyNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Unit 1 Introduction To BankingDocument27 pagesUnit 1 Introduction To BankingRandom HeroNo ratings yet

- Apy Chart PDFDocument1 pageApy Chart PDFchannel SNo ratings yet

- Print 18 05 2022Document11 pagesPrint 18 05 2022Roxana SarbuNo ratings yet

- 284 Accounting and The Time Value of Money: Table 6-1 Future Value of 1 (Future Value of A Single Sum) (1Document10 pages284 Accounting and The Time Value of Money: Table 6-1 Future Value of 1 (Future Value of A Single Sum) (1Aswar AswadNo ratings yet

- Personal Financial Management: June 2015Document15 pagesPersonal Financial Management: June 2015Dea AlviorNo ratings yet

- Real Estate Mortgage Investment Conduits (Remics) Reporting InformationDocument63 pagesReal Estate Mortgage Investment Conduits (Remics) Reporting Informationhg202No ratings yet

- Avinash Kumar (Project) .Sem 3rd Final PDFDocument39 pagesAvinash Kumar (Project) .Sem 3rd Final PDFAshish KumarNo ratings yet

- Providers and Their Payment IssuesDocument10 pagesProviders and Their Payment Issuesanon_720977331No ratings yet

- Time Value of MoneyDocument12 pagesTime Value of MoneyAzeem TalibNo ratings yet

- BONDSDocument3 pagesBONDSjdjdbNo ratings yet

- Mary Ashley Kho Yap Amaia Scapes Cagayan de Oro s2 b12l29 Rev1Document1 pageMary Ashley Kho Yap Amaia Scapes Cagayan de Oro s2 b12l29 Rev1Francis LNo ratings yet

- gm11 Businessmath Annuity Part1withpetaDocument38 pagesgm11 Businessmath Annuity Part1withpetaEmer John Dela CruzNo ratings yet

- Permanent Account Number (Pan)Document11 pagesPermanent Account Number (Pan)Presidency UniversityNo ratings yet

- Investment Portfolio Investment Abroad: 11-Mar-2022 (02:07 PM IST)Document3 pagesInvestment Portfolio Investment Abroad: 11-Mar-2022 (02:07 PM IST)parveen addsNo ratings yet

- SC EX 6-1 Bank Account ManagersDocument3 pagesSC EX 6-1 Bank Account ManagersJack WestNo ratings yet

- National Pension System (NPS) : NSDL E-Governance Infrastructure LimitedDocument31 pagesNational Pension System (NPS) : NSDL E-Governance Infrastructure LimitedBiswajit DasNo ratings yet

- Personal Loan AgreementDocument1 pagePersonal Loan AgreementLoraine Corpuz100% (2)

- Adobe Scan Dec 28, 2022Document6 pagesAdobe Scan Dec 28, 2022Vijay 0011No ratings yet

- 2.4 Ordinary Annuities: ExercisesDocument2 pages2.4 Ordinary Annuities: ExercisesRinesa SylaNo ratings yet

- Accounting 111E Quiz 5Document3 pagesAccounting 111E Quiz 5Khim NaulNo ratings yet

- Test Bank For Financial Markets and Institutions 10th EditionDocument14 pagesTest Bank For Financial Markets and Institutions 10th Editiongisellesamvb3100% (23)

- Upbly00258470000000082 2016Document1 pageUpbly00258470000000082 2016Chowkidar Dhirendra Pratap SinghNo ratings yet

- Anskey 1-1Document8 pagesAnskey 1-1De MarcusNo ratings yet

- NPA Recognition 12 Nov RBI CircularDocument30 pagesNPA Recognition 12 Nov RBI CircularNarayani TripathiNo ratings yet

- Comm Law II Combined 2023Document151 pagesComm Law II Combined 2023Kumah PrinceNo ratings yet

- BF ASN InvestmentDocument1 pageBF ASN InvestmentkeuliseutinNo ratings yet

- WhiskeySauer Budget 3.0 For RedditDocument23 pagesWhiskeySauer Budget 3.0 For RedditOmar ANo ratings yet

- Alrajhi-0 Compressed.5133686765536793Document1 pageAlrajhi-0 Compressed.5133686765536793Abdul-rheeim Q OwiNo ratings yet

- Income Tax Calculator 2023Document50 pagesIncome Tax Calculator 2023Pani NiNo ratings yet

- Financial Accounting Reporting Analysis and Decision Making 5Th Edition Carlon Solutions Manual Full Chapter PDFDocument61 pagesFinancial Accounting Reporting Analysis and Decision Making 5Th Edition Carlon Solutions Manual Full Chapter PDFthomasowens1asz100% (10)