You might also like

- Chapter Twelve: Arbitrage Pricing TheoryDocument15 pagesChapter Twelve: Arbitrage Pricing TheoryJeremiahOmwoyoNo ratings yet

- The Inefficient Stock Market: Estimating Expected Return With The Theories of Modern FinanceDocument14 pagesThe Inefficient Stock Market: Estimating Expected Return With The Theories of Modern FinanceAsma NousheenNo ratings yet

- Chapter Twelve: Arbitrage Pricing TheoryDocument15 pagesChapter Twelve: Arbitrage Pricing TheoryMego PlamoniaNo ratings yet

- The Capm: Dong Lou London School of Economics LSE Summer SchoolDocument39 pagesThe Capm: Dong Lou London School of Economics LSE Summer SchoolAryan PandeyNo ratings yet

- Return R Change in Asset Value + Income Initial Value: - R Is Ex Post - R Is Typically AnnualizedDocument41 pagesReturn R Change in Asset Value + Income Initial Value: - R Is Ex Post - R Is Typically AnnualizedrameshmbaNo ratings yet

- CAPMDocument51 pagesCAPMDisha BakshiNo ratings yet

- Lecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelDocument34 pagesLecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelL SNo ratings yet

- Chapter 9 - Multifactor Models of Risk & ReturnDocument10 pagesChapter 9 - Multifactor Models of Risk & ReturnImejah FaviNo ratings yet

- Risk ReturnDocument34 pagesRisk ReturnchandanNo ratings yet

- Lecture 8.1 (Beta and CAPM)Document17 pagesLecture 8.1 (Beta and CAPM)Devyansh GuptaNo ratings yet

- Capital Market Line (Rohit)Document33 pagesCapital Market Line (Rohit)agrawalrohit_228384No ratings yet

- Brandt 2004 Portfolio Choice ProblemsDocument75 pagesBrandt 2004 Portfolio Choice ProblemsThảo Như Trần NgọcNo ratings yet

- Portfolio Risk and Return Part 1Document34 pagesPortfolio Risk and Return Part 1Frédé AmouNo ratings yet

- L1 R50 HY NotesDocument7 pagesL1 R50 HY Notesayesha ansariNo ratings yet

- Risk and ReturnDocument31 pagesRisk and ReturnnidamahNo ratings yet

- Week 7 Week 8 - Intro To Portfolio TheoryDocument24 pagesWeek 7 Week 8 - Intro To Portfolio TheoryJoshua NemiNo ratings yet

- Capital Asset Pricing ModelDocument25 pagesCapital Asset Pricing ModelShiv Deep Sharma 20mmb087No ratings yet

- Chap7 - Risk and Return CAPM - PPimanDocument18 pagesChap7 - Risk and Return CAPM - PPimanBẢO NGUYỄN QUỐCNo ratings yet

- Arbitrage Pricing TheoryDocument21 pagesArbitrage Pricing TheoryVaidyanathan RavichandranNo ratings yet

- "We Are What We Repeatedly Do. Excellence, Then, Is Not An Act But A Habit." - AristotleDocument49 pages"We Are What We Repeatedly Do. Excellence, Then, Is Not An Act But A Habit." - AristotleErick OpiyoNo ratings yet

- Lezione 4Document42 pagesLezione 4gio040700No ratings yet

- Tutorial 4Document10 pagesTutorial 4Yaonik HimmatramkaNo ratings yet

- Risk and Return NewDocument34 pagesRisk and Return NewTushar AroraNo ratings yet

- ECN 3422 - Lecture 4 - 2021.09.30Document28 pagesECN 3422 - Lecture 4 - 2021.09.30Cornelius MasikiniNo ratings yet

- Capital Market LineDocument10 pagesCapital Market LineBishaka Singh DebNo ratings yet

- ECN 3422 - Lecture 3 - 2021.09.28Document17 pagesECN 3422 - Lecture 3 - 2021.09.28Cornelius MasikiniNo ratings yet

- Investment and Portfolio AnalysisDocument24 pagesInvestment and Portfolio Analysis‘Alya Qistina Mohd ZaimNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main ViewDocument47 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main ViewKazi FahimNo ratings yet

- RecitationDocument10 pagesRecitationAshish MalhotraNo ratings yet

- D - Tutorial 7 (Solutions)Document10 pagesD - Tutorial 7 (Solutions)AlfieNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsDocument36 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsAminul Islam AmuNo ratings yet

- Beta and CAPMDocument12 pagesBeta and CAPMSalia Tobias MwinenkumaNo ratings yet

- Portfolio OptimizationDocument27 pagesPortfolio OptimizationJeremiahOmwoyoNo ratings yet

- 11 - Modern Based Factor ModelsDocument23 pages11 - Modern Based Factor ModelsmuzammalNo ratings yet

- FM Session3 - 4Document29 pagesFM Session3 - 4Abhishek KashyapNo ratings yet

- Lecture 10Document40 pagesLecture 10Ronnie KurtzbardNo ratings yet

- Chapter 5Document14 pagesChapter 5Mohamad SyafiqNo ratings yet

- (CBCS) Commerce Paper - 4.4 (A) : Security Analysis and Portfolio ManagementDocument3 pages(CBCS) Commerce Paper - 4.4 (A) : Security Analysis and Portfolio ManagementSanaullah M SultanpurNo ratings yet

- Security Market Line and Capital Market Line (SML CML)Document18 pagesSecurity Market Line and Capital Market Line (SML CML)sagar2go89% (18)

- 6 & 7. Capm & AptDocument20 pages6 & 7. Capm & AptDicky IrawanNo ratings yet

- 4arisk and Return1Document58 pages4arisk and Return1Yunus Worn Out'sNo ratings yet

- Advanced Portfolio Mgt18-19Document8 pagesAdvanced Portfolio Mgt18-19CharlyNo ratings yet

- FINA340 8 Single Index Model - Full VersionDocument14 pagesFINA340 8 Single Index Model - Full VersionSteven ColeyNo ratings yet

- Presentation 1Document15 pagesPresentation 1Amita ShekhawatNo ratings yet

- Reading 50 Portfolio Risk and Return Part II AnswersDocument46 pagesReading 50 Portfolio Risk and Return Part II AnswersK59 Nguyen Thao LinhNo ratings yet

- CAPM Index ModelsDocument14 pagesCAPM Index ModelsSalia Tobias MwinenkumaNo ratings yet

- Topic 2.2 Portfolio Theory 2Document29 pagesTopic 2.2 Portfolio Theory 2caroNo ratings yet

- Chap 3 TCFDocument20 pagesChap 3 TCFMuhammad Umer SaigolNo ratings yet

- Portfolio ManagementDocument28 pagesPortfolio Managementagarwala4767% (3)

- Investment Analysis & Portfolio ManagementDocument27 pagesInvestment Analysis & Portfolio ManagementShubham AbrolNo ratings yet

- Capital Asset Pricing ModelDocument2 pagesCapital Asset Pricing ModelThomasaquinos Gerald Msigala Jr.No ratings yet

- Chapter 13. Risk & Return in Asset Pricing Models Chapter 13. Risk & Return in Asset Pricing ModelsDocument51 pagesChapter 13. Risk & Return in Asset Pricing Models Chapter 13. Risk & Return in Asset Pricing ModelsRaj Shekhar DasNo ratings yet

- Production AnalysisDocument36 pagesProduction AnalysisMr BhanushaliNo ratings yet

- Risiko Dan ReturnDocument27 pagesRisiko Dan ReturnThantNo ratings yet

- Chapter 8 Part 2Document7 pagesChapter 8 Part 2abdulraufdghaybeejNo ratings yet

- PR Emet 2 PDFDocument2 pagesPR Emet 2 PDFgleniaNo ratings yet

- CapmDocument26 pagesCapmNiravjain33No ratings yet

- Capmandaptmodels 2215Document37 pagesCapmandaptmodels 2215rohin gargNo ratings yet

- Bm410-10 Theory 3 - Capm and Apt 29sep05Document41 pagesBm410-10 Theory 3 - Capm and Apt 29sep05Adam KhaleelNo ratings yet

- HRM Global PerspectiveDocument9 pagesHRM Global PerspectiveVenkateshNo ratings yet

- HRM 1Document24 pagesHRM 1VenkateshNo ratings yet

- Banking Awareness McqsDocument14 pagesBanking Awareness McqsSelva100% (1)

- Importance of Capital StructureDocument9 pagesImportance of Capital StructureVenkateshNo ratings yet

- Banking and Insurance: Question BankDocument11 pagesBanking and Insurance: Question BankAnjitha jayarajNo ratings yet

- HRM 40 QuestionsDocument3 pagesHRM 40 QuestionsVenkateshNo ratings yet

- HRM Bits 2Document53 pagesHRM Bits 2Venkatesh0% (1)

- HRM 10 Questions For AssignmentDocument1 pageHRM 10 Questions For AssignmentVenkateshNo ratings yet

- Chapter Twelve: Arbitrage Pricing TheoryDocument15 pagesChapter Twelve: Arbitrage Pricing TheoryVenkateshNo ratings yet

- Unit 1 Indian Contract Act 1872Document48 pagesUnit 1 Indian Contract Act 1872DeborahNo ratings yet

- Corporate Governance Initiatives in IndiaDocument6 pagesCorporate Governance Initiatives in IndiambadheerNo ratings yet

- Do You Think ThatDocument3 pagesDo You Think ThatVenkateshNo ratings yet

- Employment of Management AccountingDocument1 pageEmployment of Management AccountingVenkateshNo ratings yet

- New Resume Format For MBA Student by Chetan VibhandikDocument3 pagesNew Resume Format For MBA Student by Chetan Vibhandikvk_chetan76% (46)

- Management and EthicsDocument12 pagesManagement and EthicsVenkateshNo ratings yet

- MiniDocument36 pagesMiniVenkateshNo ratings yet

- Bharat Petroleum and Social ResponsibilityDocument3 pagesBharat Petroleum and Social ResponsibilityVenkateshNo ratings yet

- Afm Ass-3Document2 pagesAfm Ass-3VenkateshNo ratings yet

- Ii Sem Case Study - I PartDocument9 pagesIi Sem Case Study - I PartVenkatesh100% (1)

- OBDocument1 pageOBVenkateshNo ratings yet

- Do You Think ThatDocument3 pagesDo You Think ThatVenkateshNo ratings yet

- HRMDocument1 pageHRMVenkateshNo ratings yet

- Accounting For Managers-Unit-1Document21 pagesAccounting For Managers-Unit-1VenkateshNo ratings yet

- New Resume Format For MBA Student by Chetan VibhandikDocument3 pagesNew Resume Format For MBA Student by Chetan Vibhandikvk_chetan76% (46)

- How Long To Settle A DisputeDocument4 pagesHow Long To Settle A DisputeVenkateshNo ratings yet

- Mini Project Sample (Mouli)Document39 pagesMini Project Sample (Mouli)VenkateshNo ratings yet

- Accounting For Managers ASS-1Document3 pagesAccounting For Managers ASS-1VenkateshNo ratings yet

- Accounting For Managers ASS-2Document5 pagesAccounting For Managers ASS-2VenkateshNo ratings yet

- Case StudyDocument1 pageCase StudyVenkateshNo ratings yet

- Philippine Society of Mechanical Engineers: To: Ferdinand B. Sales, DirectorDocument2 pagesPhilippine Society of Mechanical Engineers: To: Ferdinand B. Sales, DirectorJImlan Sahipa IsmaelNo ratings yet

- Paper - 2: Management Accounting and Financial AnalysisDocument20 pagesPaper - 2: Management Accounting and Financial AnalysisChandana RajasriNo ratings yet

- HolidayDocument4 pagesHolidayjessridgeukNo ratings yet

- Hotel IndustryDocument9 pagesHotel IndustryRaghu Citech N SjecNo ratings yet

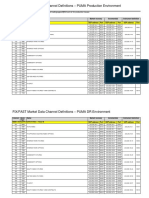

- FIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentDocument3 pagesFIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentVaibhav PoddarNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Invoice 1139421221 I0136P2000267596Document1 pageInvoice 1139421221 I0136P2000267596Thanish GattuNo ratings yet

- Top Trading TipsDocument55 pagesTop Trading TipsRadhika TrisyahdanaNo ratings yet

- HK Weekly Summary 20230718Document2 pagesHK Weekly Summary 20230718Nabil JazliNo ratings yet

- INDEMNITYDocument8 pagesINDEMNITYGaurav JindalNo ratings yet

- HSBCDocument9 pagesHSBCMohammad Mehdi JourabchiNo ratings yet

- Millward Brown ModelDocument14 pagesMillward Brown ModeljbaksiNo ratings yet

- Rent Vs Buy Calculator - AssetyogiDocument16 pagesRent Vs Buy Calculator - AssetyogiAkhlaqur RahmanNo ratings yet

- Risk Warnings and Investment Disclaimers PDFDocument8 pagesRisk Warnings and Investment Disclaimers PDFselozok1No ratings yet

- Dwnload Full Accounting For Corporate Combinations and Associations Australian 7th Edition Arthur Test Bank PDFDocument36 pagesDwnload Full Accounting For Corporate Combinations and Associations Australian 7th Edition Arthur Test Bank PDFdietzbysshevip813100% (16)

- Knowledge Is Power, So Be As Powerful As You Can!Document27 pagesKnowledge Is Power, So Be As Powerful As You Can!Ahemad ShamimNo ratings yet

- House Bill 1406: Washington State Wealth TaxDocument11 pagesHouse Bill 1406: Washington State Wealth TaxGeekWireNo ratings yet

- AFM-Module 4 Part-B Ratio Analysis ProblemsDocument5 pagesAFM-Module 4 Part-B Ratio Analysis ProblemskanikaNo ratings yet

- Module 1 - Canvas SlidesDocument40 pagesModule 1 - Canvas SlidesAniKelbakianiNo ratings yet

- An Introduction To Equity ValuationDocument37 pagesAn Introduction To Equity ValuationAamir Hamza MehediNo ratings yet

- Avanse App Form PDFDocument4 pagesAvanse App Form PDFSuresh DhanasekarNo ratings yet

- Balance Sheet Quarterly RestatedDocument12 pagesBalance Sheet Quarterly RestatedKhurram Sadiq (Father Name:Muhammad Sadiq)No ratings yet

- Atlas Copco (India) LTD Balance Sheet: Sources of FundsDocument19 pagesAtlas Copco (India) LTD Balance Sheet: Sources of FundsnehaNo ratings yet

- Direction For StudentsDocument6 pagesDirection For StudentsRitik SinghalNo ratings yet

- Bhanu Chaitanya Kumar (11) : Presented byDocument16 pagesBhanu Chaitanya Kumar (11) : Presented bySriramya PediredlaNo ratings yet

- Corp Fin Test 2 PDFDocument9 pagesCorp Fin Test 2 PDFT Surya Kandhaswamy100% (2)

- Brokerage Business PlanDocument19 pagesBrokerage Business PlanMuhammad Ahmed50% (4)

- Hotel AccountsDocument52 pagesHotel AccountsAbinavam Subramanian Mohan95% (22)

- FAR 4.3MC Investments in Debt Equity InstrumentsDocument4 pagesFAR 4.3MC Investments in Debt Equity InstrumentsEunice FulgencioNo ratings yet

- Appointment - LetterDocument3 pagesAppointment - LetteraarifNo ratings yet