You might also like

- White Hills Children's MuseumDocument23 pagesWhite Hills Children's Museumjk kumarNo ratings yet

- Estimation of Cost of Capital: Case: The Boeing 7E7Document125 pagesEstimation of Cost of Capital: Case: The Boeing 7E7jk kumarNo ratings yet

- Case: The Boeing 7E7Document183 pagesCase: The Boeing 7E7jk kumarNo ratings yet

- Siemens Electric Motor Works (A) Process-Oriented CostingDocument12 pagesSiemens Electric Motor Works (A) Process-Oriented Costingjk kumar100% (1)

- ABC - Ashokleyland MDP 2017Document41 pagesABC - Ashokleyland MDP 2017jk kumarNo ratings yet

- EVA Analysis: Case: Vyaderm PharmaceuticalsDocument56 pagesEVA Analysis: Case: Vyaderm Pharmaceuticalsjk kumarNo ratings yet

- CVP Analysis: Case: Aussie Pies (A)Document35 pagesCVP Analysis: Case: Aussie Pies (A)jk kumarNo ratings yet

- Terrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705Document6 pagesTerrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705jk kumarNo ratings yet

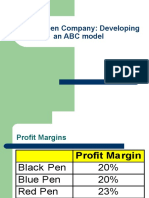

- Classic Pen Company: Developing An ABC ModelDocument22 pagesClassic Pen Company: Developing An ABC Modeljk kumarNo ratings yet

- BEA Associates - Enhanced Equity Index FundDocument16 pagesBEA Associates - Enhanced Equity Index Fundjk kumarNo ratings yet

- European Option: Basic (No Dividend) ModelDocument8 pagesEuropean Option: Basic (No Dividend) Modeljk kumarNo ratings yet

- Boeing 7E7 - UV6426-XLS-ENGDocument85 pagesBoeing 7E7 - UV6426-XLS-ENGjk kumarNo ratings yet

- 6 Polaroid Corporation 1996Document64 pages6 Polaroid Corporation 1996jk kumarNo ratings yet

- Convertible Securities: Case: Mogen IncDocument93 pagesConvertible Securities: Case: Mogen Incjk kumarNo ratings yet

- 2012 Fuel Hedging at JetBlue Airways U - V6685-XLS-ENG-3Document123 pages2012 Fuel Hedging at JetBlue Airways U - V6685-XLS-ENG-3jk kumar100% (1)

- 2012 Fuel Hedging at JetBlue AirwaysDocument181 pages2012 Fuel Hedging at JetBlue Airwaysjk kumar100% (3)

- Working Capital Management: Case: ALAC InternationalDocument55 pagesWorking Capital Management: Case: ALAC Internationaljk kumarNo ratings yet

- British Petroleum LimitedDocument593 pagesBritish Petroleum Limitedjk kumarNo ratings yet

- Bond Valuation: Case: Atlas InvestmentsDocument853 pagesBond Valuation: Case: Atlas Investmentsjk kumarNo ratings yet

- Arvind's Net Worth: Exhibit 1: Before Tax Salary and Other Benefit Details of Mr. Arvind As On 30 May 2018Document2 pagesArvind's Net Worth: Exhibit 1: Before Tax Salary and Other Benefit Details of Mr. Arvind As On 30 May 2018jk kumarNo ratings yet

- Delta Beverage Group, Inc. - FINALDocument23 pagesDelta Beverage Group, Inc. - FINALjk kumarNo ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- The Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of GilletteDocument366 pagesThe Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of Gillettejk kumarNo ratings yet

- Joint Venture: Case: Hero Honda Motors (India) LTD.: Is It Honda That Made It A Hero?Document37 pagesJoint Venture: Case: Hero Honda Motors (India) LTD.: Is It Honda That Made It A Hero?jk kumarNo ratings yet

- 3 Ribbons AnDocument2 pages3 Ribbons Anjk kumarNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Value InvestingDocument10 pagesValue InvestingAtul Divya SodhiNo ratings yet

- Li Lu Lecture 2010 CBSDocument3 pagesLi Lu Lecture 2010 CBStatsrus1100% (2)

- Important LessonDocument129 pagesImportant LessonsalihuNo ratings yet

- Ebook How I Made 5k Per Month Using Properties Faizul Ridzuan PDFDocument21 pagesEbook How I Made 5k Per Month Using Properties Faizul Ridzuan PDFAisyah Humaira50% (2)

- Geico Case Study PDFDocument22 pagesGeico Case Study PDFMichael Cano LombardoNo ratings yet

- Business Finance Investment Article DatabaseDocument13 pagesBusiness Finance Investment Article DatabaseMoney HackerNo ratings yet

- The Man Who Beats The SP Investing With Bill Miller by Janet LoweDocument274 pagesThe Man Who Beats The SP Investing With Bill Miller by Janet LoweFelipeGarciaSony100% (1)

- GMO 2009 1st Quarter Investor LetterDocument14 pagesGMO 2009 1st Quarter Investor LetterBrian McMorris100% (2)

- The - Inside - Game - To - Real - Estate - Value - Investing - Inside Look VersionDocument47 pagesThe - Inside - Game - To - Real - Estate - Value - Investing - Inside Look VersionEla DabrowskaNo ratings yet

- All Trading BooksDocument96 pagesAll Trading BooksNACHIKETH8957% (7)

- Thesis: The Influence of Hedge Funds On Share PricesDocument63 pagesThesis: The Influence of Hedge Funds On Share Pricesbenkedav100% (7)

- Creighton Value Investing PanelDocument9 pagesCreighton Value Investing PanelbenclaremonNo ratings yet

- Value Investing Syllabus - Summer 2023Document2 pagesValue Investing Syllabus - Summer 2023Timothy PruittNo ratings yet

- The Intelligent InvestorDocument7 pagesThe Intelligent InvestorRajivShahNo ratings yet

- Graham's ChecklistDocument8 pagesGraham's ChecklistNicolasPioNo ratings yet

- Ae 18 Financial MarketsDocument6 pagesAe 18 Financial Marketsnglc srzNo ratings yet

- Financial Statement AnalysisDocument10 pagesFinancial Statement AnalysisBeth Diaz LaurenteNo ratings yet

- Safal Niveshak Mastermind Free ChaptersDocument31 pagesSafal Niveshak Mastermind Free Chaptersthisispraveen100% (2)

- Bruce Greenwald InterviewDocument9 pagesBruce Greenwald Interviewkirit0No ratings yet

- The Ultimate Guide To Stock Valuation - Sample ChaptersDocument11 pagesThe Ultimate Guide To Stock Valuation - Sample ChaptersOld School ValueNo ratings yet

- Prof Sanjay Bakshi's Fav Stock Falls From Grace Even As ValuePickr Forum's Ominous Warning Rings TrueDocument7 pagesProf Sanjay Bakshi's Fav Stock Falls From Grace Even As ValuePickr Forum's Ominous Warning Rings Truebhaskar.jain20021814No ratings yet

- What Is An Investment PhilosophyDocument10 pagesWhat Is An Investment PhilosophyArafat DreamtheterNo ratings yet

- Secrets of SovereignDocument13 pagesSecrets of SovereignredcovetNo ratings yet

- Greenwald Earnings Power Value EPV Lecture SlidesDocument43 pagesGreenwald Earnings Power Value EPV Lecture SlidesOld School Value100% (12)

- Sumit Todi The Piotroski F ScoreDocument9 pagesSumit Todi The Piotroski F ScoreSumit TodiNo ratings yet

- NYU Stern Evaluation NewsletterDocument25 pagesNYU Stern Evaluation NewsletterCanadianValueNo ratings yet

- The 10 Best Investors in The WorldDocument14 pagesThe 10 Best Investors in The WorldAditya BhideNo ratings yet

- 2011 Value Investing Congress NotesDocument71 pages2011 Value Investing Congress NotesbenclaremonNo ratings yet

- Warren Buffet Letters To ShareholdersDocument44 pagesWarren Buffet Letters To Shareholdersvr211480% (5)

- CMT Curriculum 2021 LEVEL 1 Wiley FINALDocument19 pagesCMT Curriculum 2021 LEVEL 1 Wiley FINALJamesMc114467% (12)