You might also like

- ALAC International - Working Capital FinancingDocument8 pagesALAC International - Working Capital FinancingAjith SudhakaranNo ratings yet

- ALAC InternationalDocument8 pagesALAC Internationalvarunjains100% (1)

- Private valuation of Bluntly Media for potential acquisitionDocument3 pagesPrivate valuation of Bluntly Media for potential acquisitionSrikant SharmaNo ratings yet

- Boston Chicken bond valuation challengesDocument7 pagesBoston Chicken bond valuation challengesARJUN M K100% (1)

- The Best Deal Gillette Could GetDocument1 pageThe Best Deal Gillette Could Get连文琪No ratings yet

- Case 16 Group 56 FinalDocument54 pagesCase 16 Group 56 FinalSayeedMdAzaharulIslamNo ratings yet

- WACC, Growth Rates, and DCF Valuation for Bluntly MediaDocument18 pagesWACC, Growth Rates, and DCF Valuation for Bluntly Mediahimanshu sagarNo ratings yet

- GR-II-Team 11-2018Document4 pagesGR-II-Team 11-2018Gautam PatilNo ratings yet

- Bluntly Media Valuatio1Document1 pageBluntly Media Valuatio1SrikantNo ratings yet

- FM-07 Valuations, Mergers Acquisitions Question PaperDocument4 pagesFM-07 Valuations, Mergers Acquisitions Question PaperSonu0% (1)

- Berkshire - IntroDocument2 pagesBerkshire - IntroRohith ThatchanNo ratings yet

- Instruction For Nantucket NectarsDocument4 pagesInstruction For Nantucket NectarsTanaporn SuwanchaiyongNo ratings yet

- Atlas Fin CaseDocument11 pagesAtlas Fin CaseAniruddhaNo ratings yet

- Case Summary Financial Management-II: "The Loewen Group, Inc. (Abridged) "Document4 pagesCase Summary Financial Management-II: "The Loewen Group, Inc. (Abridged) "Rishabh Kothari100% (1)

- The Verizon versus Qwest Battle for MCI TakeoverDocument17 pagesThe Verizon versus Qwest Battle for MCI TakeoverLucas Tai100% (1)

- Particulars MSFT 3 Year 5 Year 10 Year 30 YearDocument2 pagesParticulars MSFT 3 Year 5 Year 10 Year 30 YearAsad BilalNo ratings yet

- Session 10 Simulation Questions PDFDocument6 pagesSession 10 Simulation Questions PDFVAIBHAV WADHWA0% (1)

- Valuing a Cross-Border LBO of Yell GroupDocument5 pagesValuing a Cross-Border LBO of Yell GroupSameer Kumar0% (1)

- Individual AssignmentDocument10 pagesIndividual Assignmentparitosh nayakNo ratings yet

- Case Berkshire Hathaway Dividend Policy ParadigmDocument9 pagesCase Berkshire Hathaway Dividend Policy ParadigmHugoNo ratings yet

- STFC X15Document7 pagesSTFC X15Kajol Keshri100% (1)

- Blogging at Bzzagent Case AnalysisDocument6 pagesBlogging at Bzzagent Case AnalysisRavikanth VangalaNo ratings yet

- A2 - Group 1Document4 pagesA2 - Group 1Tanmay Tiwari100% (4)

- Dwo PHD01003 Harshad Savant Term2 EndtermDocument8 pagesDwo PHD01003 Harshad Savant Term2 EndtermHarshad SavantNo ratings yet

- Sure CutDocument1 pageSure Cutchch917No ratings yet

- Adelphia - V1Document6 pagesAdelphia - V1PratikkalantriNo ratings yet

- Turning A Product Into A Brand: Adeo Health ScienceDocument11 pagesTurning A Product Into A Brand: Adeo Health ScienceHarshit KumarNo ratings yet

- FM 475 Final ExamDocument7 pagesFM 475 Final Examabccd11No ratings yet

- Apple Cash Case StudyDocument2 pagesApple Cash Case StudyJanice JingNo ratings yet

- OM Scott Case AnalysisDocument20 pagesOM Scott Case AnalysissushilkhannaNo ratings yet

- This Study Resource WasDocument9 pagesThis Study Resource WasVishalNo ratings yet

- Sealed AirDocument10 pagesSealed AirHimanshu KumarNo ratings yet

- BCE: INC Case AnalysisDocument6 pagesBCE: INC Case AnalysisShuja Ur RahmanNo ratings yet

- BerkshireDocument30 pagesBerkshireNimra Masood100% (3)

- Project ChariotDocument6 pagesProject ChariotRavina PuniaNo ratings yet

- Case Submission - Stone Container Corporation (A) ' Group VIIIDocument5 pagesCase Submission - Stone Container Corporation (A) ' Group VIIIGURNEET KAURNo ratings yet

- Financial Management - Case - Sealed AirDocument7 pagesFinancial Management - Case - Sealed AirAryan AnandNo ratings yet

- Polaroid Corporation Case Solution Final PDFDocument8 pagesPolaroid Corporation Case Solution Final PDFNovel ArianNo ratings yet

- Kmart, Sears and ESLDocument10 pagesKmart, Sears and ESLshreesti11290No ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- Sealed Air Corp Case Write Up PDFDocument3 pagesSealed Air Corp Case Write Up PDFRamjiNo ratings yet

- Sure CutDocument37 pagesSure Cutshmuup1100% (4)

- Burton SensorsDocument4 pagesBurton SensorsAbhishek BaratamNo ratings yet

- Stone Container Corporation's Financial Problems and SolutionsDocument7 pagesStone Container Corporation's Financial Problems and Solutionsanon_911384976No ratings yet

- JC Penney CaseDocument8 pagesJC Penney CaseSebastian MansillaNo ratings yet

- Yell Case Exhibits Growth RatesDocument12 pagesYell Case Exhibits Growth RatesJames MorinNo ratings yet

- Case Background: Kaustav Dey B18088Document9 pagesCase Background: Kaustav Dey B18088Kaustav DeyNo ratings yet

- Sealed Air Corporation's Leveraged Recapitalization (A)Document10 pagesSealed Air Corporation's Leveraged Recapitalization (A)Ramji100% (1)

- MGT431 - Apple, Einhorn, iPrefs Group ReportDocument13 pagesMGT431 - Apple, Einhorn, iPrefs Group ReportMokshNo ratings yet

- Sealed Air CorporationDocument4 pagesSealed Air CorporationValdemar Miguel SilvaNo ratings yet

- Uttam Kumar Sec-A Dividend Policy Linear TechnologyDocument11 pagesUttam Kumar Sec-A Dividend Policy Linear TechnologyUttam Kumar100% (1)

- Berkshire's Bid for Carter's - Industry Fit and Quantitative AnalysisDocument2 pagesBerkshire's Bid for Carter's - Industry Fit and Quantitative AnalysisAlex TovNo ratings yet

- Letter From PrisonDocument10 pagesLetter From PrisonNur Sakinah MustafaNo ratings yet

- Iron Gate - InputDocument1 pageIron Gate - InputShshank0% (1)

- Sealed Air CorporationDocument7 pagesSealed Air Corporationhadil_1No ratings yet

- Facebook, Inc: The Initial Public OfferingDocument5 pagesFacebook, Inc: The Initial Public OfferingHanako Taniguchi PoncianoNo ratings yet

- EFIN542 U12 T01 PowerPointDocument57 pagesEFIN542 U12 T01 PowerPointcustomsgyanNo ratings yet

- Effects of Working Capital Management On Sme ProfitabilityDocument14 pagesEffects of Working Capital Management On Sme ProfitabilityMilind WajeNo ratings yet

- Module IV - Working Capital ManagementDocument50 pagesModule IV - Working Capital ManagementAshwin DholeNo ratings yet

- Raffles Holdings Limited - Valuation of A Divestiture Teaching Note - NTU044-XLS-EnGDocument7 pagesRaffles Holdings Limited - Valuation of A Divestiture Teaching Note - NTU044-XLS-EnGjk kumarNo ratings yet

- The Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of GilletteDocument366 pagesThe Best Deal GiIlette Could Get - Procter & Gamble's Acquisition of Gillettejk kumarNo ratings yet

- Raffles Holdings Limited - Valuation of A DivestitureDocument37 pagesRaffles Holdings Limited - Valuation of A Divestiturejk kumarNo ratings yet

- ANNUAL REPORT 2017-18 HIGHLIGHTSDocument220 pagesANNUAL REPORT 2017-18 HIGHLIGHTSramsinntNo ratings yet

- Boeing 7e7 Uv6426 Xls EngDocument82 pagesBoeing 7e7 Uv6426 Xls Engjk kumarNo ratings yet

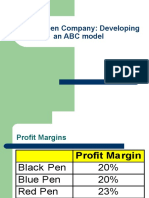

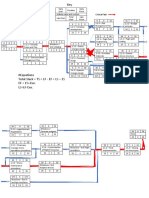

- Classic Pen Company: Developing An ABC ModelDocument22 pagesClassic Pen Company: Developing An ABC Modeljk kumarNo ratings yet

- CVP Analysis: Case: Aussie Pies (A)Document35 pagesCVP Analysis: Case: Aussie Pies (A)jk kumarNo ratings yet

- Case: The Boeing 7E7Document183 pagesCase: The Boeing 7E7jk kumarNo ratings yet

- Boeing 7e7 Uv6426 Xls EngDocument82 pagesBoeing 7e7 Uv6426 Xls Engjk kumarNo ratings yet

- Estimation of Cost of Capital: Case: The Boeing 7E7Document125 pagesEstimation of Cost of Capital: Case: The Boeing 7E7jk kumarNo ratings yet

- EVA Analysis: Case: Vyaderm PharmaceuticalsDocument56 pagesEVA Analysis: Case: Vyaderm Pharmaceuticalsjk kumarNo ratings yet

- Market Timing Case Study Evaluating Investment RiskDocument31 pagesMarket Timing Case Study Evaluating Investment Riskjk kumarNo ratings yet

- ABC - Ashokleyland MDP 2017Document41 pagesABC - Ashokleyland MDP 2017jk kumarNo ratings yet

- White Hills Children's MuseumDocument23 pagesWhite Hills Children's Museumjk kumarNo ratings yet

- Siemens Electric Motor Works (A) Process-Oriented CostingDocument12 pagesSiemens Electric Motor Works (A) Process-Oriented Costingjk kumar100% (1)

- Project No 1 DCF 2 DCF 3 DCF 4 DCF 5 Initial Investment: Exhibit 1 Project Free Cash Flows (Dollars in Thousands)Document5 pagesProject No 1 DCF 2 DCF 3 DCF 4 DCF 5 Initial Investment: Exhibit 1 Project Free Cash Flows (Dollars in Thousands)jk kumarNo ratings yet

- Marriott - Spread SheetDocument13 pagesMarriott - Spread Sheetjk kumarNo ratings yet

- 12 Marriott Corporation - The Cost of Capital (Abridged)Document9 pages12 Marriott Corporation - The Cost of Capital (Abridged)jk kumarNo ratings yet

- 3 Divisional Cost of CapitalDocument41 pages3 Divisional Cost of Capitaljk kumarNo ratings yet

- Case: The Boeing 7E7Document183 pagesCase: The Boeing 7E7jk kumarNo ratings yet

- Mercury Case ExhibitsDocument10 pagesMercury Case ExhibitsjujuNo ratings yet

- Value Investing - Used in Private Banking ProgrameDocument57 pagesValue Investing - Used in Private Banking Programejk kumarNo ratings yet

- Boeing 7E7 - UV6426-XLS-ENGDocument85 pagesBoeing 7E7 - UV6426-XLS-ENGjk kumarNo ratings yet

- 6 Polaroid Corporation 1996Document64 pages6 Polaroid Corporation 1996jk kumarNo ratings yet

- BEA Associates - Enhanced Equity Index FundDocument16 pagesBEA Associates - Enhanced Equity Index Fundjk kumarNo ratings yet

- Mercury Athletic Footwear - Valuing The OpportunityDocument55 pagesMercury Athletic Footwear - Valuing The OpportunityKunal Mehta100% (2)

- Bond ValuationDocument52 pagesBond Valuationjk kumarNo ratings yet

- European Option: Basic (No Dividend) ModelDocument8 pagesEuropean Option: Basic (No Dividend) Modeljk kumarNo ratings yet

- Terrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705Document6 pagesTerrapower Harvard Business School Teaching Note: 5-815-050 Courseware 5-816-705jk kumarNo ratings yet

- Convertible Securities: Case: Mogen IncDocument93 pagesConvertible Securities: Case: Mogen Incjk kumarNo ratings yet

- Service Request - Id 000000003862891Document3 pagesService Request - Id 000000003862891Mohamed HamdyNo ratings yet

- Anthony ProctorDocument2 pagesAnthony ProctorsanjuNo ratings yet

- CPM Method Wilmont's Drone Case PDFDocument2 pagesCPM Method Wilmont's Drone Case PDFRwa Gihuta100% (3)

- Customer Satisfaction For ISO 9001 - 2015 With ExamplesDocument5 pagesCustomer Satisfaction For ISO 9001 - 2015 With ExamplesSudheer23984No ratings yet

- HBL Internship ReportDocument36 pagesHBL Internship ReportKhurram Jehanzeb75% (4)

- Sustainability Reporting FrameworksDocument20 pagesSustainability Reporting Frameworksapi-286745978No ratings yet

- Human Relations Approach TheoriesDocument17 pagesHuman Relations Approach TheoriesSayam RoyNo ratings yet

- Resume - 01.03.2016Document5 pagesResume - 01.03.2016muthuswamy77No ratings yet

- Dipankar RoyDocument3 pagesDipankar RoysandeephwrNo ratings yet

- External Auditing and QualityDocument351 pagesExternal Auditing and QualityKristof MC100% (1)

- Warehouse Automation and Integration Improves Operations Codex3812Document3 pagesWarehouse Automation and Integration Improves Operations Codex3812James ThoNo ratings yet

- A Project Report Onoperations Management in Shoppers' StopDocument18 pagesA Project Report Onoperations Management in Shoppers' Stopnaruto_u91% (11)

- 2.2.4.acceptance TestingDocument3 pages2.2.4.acceptance TestingThành CôngNo ratings yet

- Cost Engineers Notebook!!!!!Document5 pagesCost Engineers Notebook!!!!!Anonymous 19hUyem0% (2)

- Ficep Logistics ImprovementPITrealDocument28 pagesFicep Logistics ImprovementPITrealSandeep MishraNo ratings yet

- Obermeyer Solution 1Document38 pagesObermeyer Solution 1razvanpravat895No ratings yet

- Penner PDFDocument2 pagesPenner PDFpalak0% (1)

- Auditing II Midterm TestDocument7 pagesAuditing II Midterm TestpartnerinChrist100% (3)

- Organizational DesignDocument11 pagesOrganizational DesignPeter John SabasNo ratings yet

- Unit 5 CoacconDocument7 pagesUnit 5 CoacconSofia Mae AlbercaNo ratings yet

- Amr Mohamed Zen El Abdeen: Career ObjectivesDocument2 pagesAmr Mohamed Zen El Abdeen: Career ObjectivessalemNo ratings yet

- Chaotics The Business of Managing and Marketing in The Age of Turbulence 1Document2 pagesChaotics The Business of Managing and Marketing in The Age of Turbulence 1Mustafa Al AliNo ratings yet

- CHAPTER 2 MSDM DowlingDocument4 pagesCHAPTER 2 MSDM DowlingDhery January HidayatNo ratings yet

- Collaborative Product CommerceDocument5 pagesCollaborative Product CommerceNavin Vijey RajNo ratings yet

- Operations Management SlidesDocument87 pagesOperations Management SlidesrockstarchandreshNo ratings yet

- MBA Spring 2010 ProspectusDocument20 pagesMBA Spring 2010 ProspectusziabuttNo ratings yet

- DelegationDocument4 pagesDelegationalwil144548No ratings yet

- Taco Bell: The Breakfast OpportunitiesDocument14 pagesTaco Bell: The Breakfast OpportunitiesQudsia NourasNo ratings yet

- Networking and EntrepreneurshipDocument14 pagesNetworking and EntrepreneurshipKshitishNo ratings yet

- Ipcr SampleDocument11 pagesIpcr SampleJayzel Laureano100% (2)