You might also like

- B215 AC08 Mochi Kochi 6th Presentation 19 June 2009Document46 pagesB215 AC08 Mochi Kochi 6th Presentation 19 June 2009tohqinzhiNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- CHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)Document20 pagesCHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)VerrelyNo ratings yet

- Introduction To Financial Accounting: Long-Lived AssetsDocument58 pagesIntroduction To Financial Accounting: Long-Lived AssetsShubham Kaushik100% (1)

- Financial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsDocument55 pagesFinancial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsmukul3087_305865623No ratings yet

- ACC101 Chapter8newDocument19 pagesACC101 Chapter8newLaras Sukma Nurani TirtawidjajaNo ratings yet

- Bhawana Jain, ASB, EttimadaiDocument64 pagesBhawana Jain, ASB, EttimadaiDeepak PrabhakarNo ratings yet

- FINACC - Depreciation and Long-Lived Nonmonetary Assets - 031318Document8 pagesFINACC - Depreciation and Long-Lived Nonmonetary Assets - 031318ventus5thNo ratings yet

- depreciation 2023-2024 iisjed class for 12th standard CBSEDocument29 pagesdepreciation 2023-2024 iisjed class for 12th standard CBSETaLHa iNaM sameerNo ratings yet

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- Acct 100 Chapter 8 Notes S22Document60 pagesAcct 100 Chapter 8 Notes S22Cyntia ArellanoNo ratings yet

- INDE/EGRM 6617-02 Engineering Economy and Cost Estimating: Chapter 7: Depreciation and Income TaxesDocument40 pagesINDE/EGRM 6617-02 Engineering Economy and Cost Estimating: Chapter 7: Depreciation and Income Taxesfahad noumanNo ratings yet

- Plant Assets, Natural Resources, and Intangible AssetsDocument68 pagesPlant Assets, Natural Resources, and Intangible Assetsdwi studyNo ratings yet

- Accounting Adjustments ExplainedDocument45 pagesAccounting Adjustments ExplainednarmadaNo ratings yet

- Chap 5Document10 pagesChap 5khedira sami100% (1)

- Long - Lived AssetsDocument25 pagesLong - Lived AssetsJeff KinutsNo ratings yet

- Faculty Name - Sandeep Bhatiya: Financial Accounting FundamentalDocument34 pagesFaculty Name - Sandeep Bhatiya: Financial Accounting FundamentalNamrata PrasadNo ratings yet

- CHAPTER 8 - DepreciationDocument12 pagesCHAPTER 8 - DepreciationMuhammad AdibNo ratings yet

- Depreciation: Systematic Allocation of The Depreciable Amount of An Asset Over Its Useful LifeDocument24 pagesDepreciation: Systematic Allocation of The Depreciable Amount of An Asset Over Its Useful LifeKatrina PetracheNo ratings yet

- Depreciation AccountingDocument42 pagesDepreciation AccountingGaurav SharmaNo ratings yet

- Chapter 2 - Plant AssetDocument8 pagesChapter 2 - Plant AssetMelkamu Dessie TamiruNo ratings yet

- Lecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringDocument49 pagesLecture - 6 - Long - Term - Assets - NUS ACC1002 2020 SpringZenyui100% (1)

- Depriciation AccountingDocument42 pagesDepriciation Accountingezek1elNo ratings yet

- Prepare Financial Reports Edited HAND OUT1Document34 pagesPrepare Financial Reports Edited HAND OUT1getachewhabtamu361No ratings yet

- Depreciation Methods Guide For BusinessesDocument4 pagesDepreciation Methods Guide For BusinessesSantosh KakadNo ratings yet

- Ch#4 Accounting For Non Current AssetsDocument7 pagesCh#4 Accounting For Non Current Assetseaglerealestate31No ratings yet

- Prepare Financial Report 3rdDocument12 pagesPrepare Financial Report 3rdTegene Tesfaye100% (1)

- Accounting Standard 6 - DepreciationDocument34 pagesAccounting Standard 6 - DepreciationSarthak Gupta100% (2)

- Week 12 - Capex and DepreciationDocument55 pagesWeek 12 - Capex and DepreciationajenggNo ratings yet

- More ConceptsDocument47 pagesMore ConceptsGurkirat Singh100% (1)

- DepreciationDocument41 pagesDepreciationarun pratap singh bharatiNo ratings yet

- MAS 10 - Capital BudgetingDocument10 pagesMAS 10 - Capital BudgetingClint AbenojaNo ratings yet

- DepreciationDocument8 pagesDepreciationbhanu100% (1)

- Plant AssetsDocument41 pagesPlant AssetsShawon RahmanNo ratings yet

- ACCY901 Accounting Foundations For Professionals: Topic 7 Non-Current AssetsDocument33 pagesACCY901 Accounting Foundations For Professionals: Topic 7 Non-Current Assetsvenkatachalam radhakrishnan100% (1)

- Depreciation account-WPS OfficeDocument11 pagesDepreciation account-WPS Officegbengayusuf167No ratings yet

- Plant Assets Accounting and Depreciation MethodsDocument18 pagesPlant Assets Accounting and Depreciation MethodsYukino YukinoshitaNo ratings yet

- IENG 302 Lecture 16Document18 pagesIENG 302 Lecture 16Ganesh MandpeNo ratings yet

- Fixed Assets AccountingDocument24 pagesFixed Assets Accountingjayti desaiNo ratings yet

- Depreciation - Inventory Valuation MethodsDocument48 pagesDepreciation - Inventory Valuation MethodsArun Panwar100% (1)

- ACC 1100 Days 14&15 Long-Lived Assets PDFDocument25 pagesACC 1100 Days 14&15 Long-Lived Assets PDFYevhenii VdovenkoNo ratings yet

- Accounting o LevelsDocument6 pagesAccounting o LevelsHira KhanNo ratings yet

- PDF NotesDocument7 pagesPDF NotesBinoy TrevadiaNo ratings yet

- DepreciationDocument10 pagesDepreciationsoumibasuNo ratings yet

- Class 8Document48 pagesClass 8NkNo ratings yet

- Chapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Document18 pagesChapter 10 Plant Assets, Natural Resources, and Intangible Assets (13 E)Raa100% (1)

- CH9 Long-Lived AssetsDocument42 pagesCH9 Long-Lived AssetsStudent Sokha ChanchesdaNo ratings yet

- Financial Accounting IIDocument13 pagesFinancial Accounting IITimi DeleNo ratings yet

- Engineering and Project Management CostsDocument27 pagesEngineering and Project Management CostsMogogi PercyNo ratings yet

- Chapter 10 SummaryDocument14 pagesChapter 10 SummaryNhi Nguyễn Trần LiênNo ratings yet

- BBA II Chapter 3 Depreciation AccountingDocument28 pagesBBA II Chapter 3 Depreciation AccountingSiddharth Salgaonkar100% (1)

- Can you depreciate an asset in one yearDocument10 pagesCan you depreciate an asset in one yearbalucbe35No ratings yet

- Financial Reporting: Othm Level 5 Diploma in Accounting and BusinessDocument33 pagesFinancial Reporting: Othm Level 5 Diploma in Accounting and BusinessDime PierrowNo ratings yet

- Accounting For DepreciationDocument16 pagesAccounting For DepreciationKrishna100% (2)

- Baf 223 Accounting for Labilities - Depreciation NotesDocument5 pagesBaf 223 Accounting for Labilities - Depreciation Notesaroridouglas880No ratings yet

- Income TaxDocument71 pagesIncome TaxMahrukh MalikNo ratings yet

- Capital and Revenue ExpenditureDocument22 pagesCapital and Revenue ExpenditureTimi Dele100% (1)

- IAS 16 - Property Plant and EquipmentDocument35 pagesIAS 16 - Property Plant and EquipmentlaaybaNo ratings yet

- Chapter 2 PPEDocument16 pagesChapter 2 PPEcherunegashNo ratings yet

- Introduction To Finance Formula SheetDocument2 pagesIntroduction To Finance Formula SheetKhanh LinhNo ratings yet

- Finance Individual AssignmentDocument13 pagesFinance Individual AssignmentDylan Rabin PereiraNo ratings yet

- Accounting Group Assignment 1 (Updated)Document22 pagesAccounting Group Assignment 1 (Updated)Dylan Rabin PereiraNo ratings yet

- Coverpage For AssignmentDocument2 pagesCoverpage For AssignmentDylan Rabin PereiraNo ratings yet

- I2F Individual Assignment QA Aug 2020Document4 pagesI2F Individual Assignment QA Aug 2020Dylan Rabin PereiraNo ratings yet

- Section 5Document2 pagesSection 5Dylan Rabin PereiraNo ratings yet

- I2F Revision QuestionsDocument1 pageI2F Revision QuestionsDylan Rabin PereiraNo ratings yet

- Tutorial 11 QsDocument3 pagesTutorial 11 QsDylan Rabin PereiraNo ratings yet

- Revision Q&ADocument5 pagesRevision Q&ADylan Rabin PereiraNo ratings yet

- Accounting Group Assignment 1 (Updated)Document22 pagesAccounting Group Assignment 1 (Updated)Dylan Rabin PereiraNo ratings yet

- Accounting RevisionDocument3 pagesAccounting RevisionDylan Rabin PereiraNo ratings yet

- Tutorial 11 QsDocument3 pagesTutorial 11 QsDylan Rabin PereiraNo ratings yet

- Coverpage For Assignment Finance (Dylan Rabin)Document3 pagesCoverpage For Assignment Finance (Dylan Rabin)Dylan Rabin PereiraNo ratings yet

- Revision Q&ADocument5 pagesRevision Q&ADylan Rabin PereiraNo ratings yet

- Revision Q&ADocument5 pagesRevision Q&ADylan Rabin PereiraNo ratings yet

- Accounting Group Assignment 1 (Updated)Document22 pagesAccounting Group Assignment 1 (Updated)Dylan Rabin PereiraNo ratings yet

- Accounting RevisionDocument3 pagesAccounting RevisionDylan Rabin PereiraNo ratings yet

- Tutorial 11 QsDocument3 pagesTutorial 11 QsDylan Rabin PereiraNo ratings yet

- Tutorial 10 QsDocument4 pagesTutorial 10 QsDylan Rabin PereiraNo ratings yet

- Accounting RevisionDocument3 pagesAccounting RevisionDylan Rabin PereiraNo ratings yet

- Tutorial 12 QuestionsDocument8 pagesTutorial 12 QuestionsDylan Rabin PereiraNo ratings yet

- Tutorial 10 QsDocument4 pagesTutorial 10 QsDylan Rabin PereiraNo ratings yet

- Tutorial 7 QsDocument4 pagesTutorial 7 QsDylan Rabin PereiraNo ratings yet

- Tutorial 7Document74 pagesTutorial 7Dylan Rabin PereiraNo ratings yet

- Tutorial 6 QsDocument6 pagesTutorial 6 QsDylan Rabin PereiraNo ratings yet

- Tutorial 8 QsDocument9 pagesTutorial 8 QsDylan Rabin PereiraNo ratings yet

- Tutorial 9 QsDocument7 pagesTutorial 9 QsDylan Rabin PereiraNo ratings yet

- Tutorial 5 QsDocument7 pagesTutorial 5 QsDarren Khew0% (1)

- Tutorial 1 QuestionsDocument9 pagesTutorial 1 QuestionsDylan Rabin PereiraNo ratings yet

- Tutorial 4 QsDocument8 pagesTutorial 4 QsDylan Rabin PereiraNo ratings yet

- Ashenafi BeyeneDocument77 pagesAshenafi BeyeneYonas Begashaw Jr.No ratings yet

- The Manager and Management AccountingDocument24 pagesThe Manager and Management AccountingDr. Alla Talal YassinNo ratings yet

- Financial Accounting: Plant Assets, Natural Resources, and IntangiblesDocument85 pagesFinancial Accounting: Plant Assets, Natural Resources, and Intangiblesgizem akçaNo ratings yet

- Journalizing Transactions & Analyzing Business Entries in 40 CharactersDocument5 pagesJournalizing Transactions & Analyzing Business Entries in 40 CharactersSatvik Bisht100% (1)

- Job-Order Costing: Cost Flows and External Reporting: QuestionsDocument62 pagesJob-Order Costing: Cost Flows and External Reporting: QuestionsDona Kris GumbanNo ratings yet

- Review of Financial Statements PreparationDocument23 pagesReview of Financial Statements PreparationRhea QuibolNo ratings yet

- Guide To Public Financial ManagementDocument124 pagesGuide To Public Financial Managementmorisrav23No ratings yet

- Managerial Accounting Module 1-6Document18 pagesManagerial Accounting Module 1-6Migz Jose Garcia CalicdanNo ratings yet

- Testing Ingine KaliDocument30 pagesTesting Ingine KaliIngiaNo ratings yet

- HW On Equity SecuritiesDocument3 pagesHW On Equity Securitiesjjk firstloveNo ratings yet

- 8.cash Flow StatementDocument16 pages8.cash Flow Statementnarangdiya602No ratings yet

- Acca Paper 1.2Document25 pagesAcca Paper 1.2anon-280248No ratings yet

- Marginal Costing Concepts ExplainedDocument21 pagesMarginal Costing Concepts ExplainedGauravsNo ratings yet

- Accounting Standard (AS) 9 Revenue RecognitionDocument12 pagesAccounting Standard (AS) 9 Revenue RecognitionKhushi KumariNo ratings yet

- Solutions CH 6 PDFDocument62 pagesSolutions CH 6 PDF21aberckmuellerNo ratings yet

- Barton Co. Balance Sheet For Branch December 31, 20x4Document27 pagesBarton Co. Balance Sheet For Branch December 31, 20x4Love FreddyNo ratings yet

- F3 ACCA Financial Accounting - Inventory by MOCDocument10 pagesF3 ACCA Financial Accounting - Inventory by MOCMunyaradzi Onismas Chinyukwi100% (1)

- CH 11 Question Book - Not ReconciliationDocument5 pagesCH 11 Question Book - Not Reconciliationahmed0% (1)

- AT Welcome Pack 2021 Reduced VersionDocument16 pagesAT Welcome Pack 2021 Reduced VersionHenry Sicelo NabelaNo ratings yet

- Financial Accounting Information For Decisions 8th Edition John Wild Test BankDocument24 pagesFinancial Accounting Information For Decisions 8th Edition John Wild Test BankDerrickCastanedamjpzo100% (28)

- Intercompany Transactions ConsolidationDocument1 pageIntercompany Transactions ConsolidationErjohn Papa0% (1)

- Makalah Tentang Asset (Bahasa Inggris)Document5 pagesMakalah Tentang Asset (Bahasa Inggris)Ilham Sukron100% (1)

- Ch1 - ExercisesDocument2 pagesCh1 - ExercisesAfon 03No ratings yet

- Exercises On Accounting CycleDocument7 pagesExercises On Accounting CycleXyriene RocoNo ratings yet

- Umme Zainab Accounting AssighnmentDocument2 pagesUmme Zainab Accounting Assighnmentzm65012No ratings yet

- The Audit of Assertions - ACCA GlobalDocument8 pagesThe Audit of Assertions - ACCA Globaldesk.back.recovNo ratings yet

- Accounting For Public Sector and Civil Society 2022 LatestDocument170 pagesAccounting For Public Sector and Civil Society 2022 LatestZerai Hagos HailemariamNo ratings yet

- The Advantages of Manual VsDocument12 pagesThe Advantages of Manual Vsxxx101xxxNo ratings yet

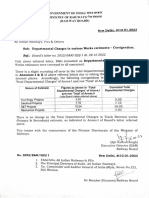

- Corrigendum of Departmental ChargesDocument1 pageCorrigendum of Departmental ChargesADEE G GRCNo ratings yet

- CPA REVIEW SCHOOL OF THE PHILIPPINESDocument11 pagesCPA REVIEW SCHOOL OF THE PHILIPPINESNhel AlvaroNo ratings yet