You might also like

- Activity Based CostingDocument30 pagesActivity Based Costinghardik1302No ratings yet

- The Relevance of Porter's Five Forces in Today's Innovative and Changing Business EnvironmentDocument23 pagesThe Relevance of Porter's Five Forces in Today's Innovative and Changing Business EnvironmentKarim IsmailNo ratings yet

- 03 - FoAM Form-02 - Fraud Risk Assessment TemplateDocument3 pages03 - FoAM Form-02 - Fraud Risk Assessment Templatenonavi lazoNo ratings yet

- Unilever in India: Hindustan Lever S Project Shakti - Marketing FMCG To The Ruralconsumer Case AnalysisDocument5 pagesUnilever in India: Hindustan Lever S Project Shakti - Marketing FMCG To The Ruralconsumer Case Analysismahtaabk100% (4)

- Session 7 - Process Selection and AnalysisDocument66 pagesSession 7 - Process Selection and AnalysisPranit padhiNo ratings yet

- Dessler Ch3Document5 pagesDessler Ch3Bobleagă Perişan Nicoleta RoxanaNo ratings yet

- Functionalities Sap Business Sap Business: One All - in - OneDocument9 pagesFunctionalities Sap Business Sap Business: One All - in - OneSelvakumar RmNo ratings yet

- Chapter 3Document76 pagesChapter 3wowipev155No ratings yet

- ch3 Student FB2101 1011BDocument66 pagesch3 Student FB2101 1011BJavier TsangNo ratings yet

- Job Order Costing 1Document50 pagesJob Order Costing 1Adrian ContilloNo ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument61 pagesSystems Design: Job-Order Costing: Chapter ThreeBS StudioNo ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument86 pagesSystems Design: Job-Order Costing: Chapter ThreeSabeeh FarooqNo ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument86 pagesSystems Design: Job-Order Costing: Chapter ThreeFaisal KhoriNo ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument61 pagesSystems Design: Job-Order Costing: Chapter ThreesanosyNo ratings yet

- Job-Order Costing: Chapter ThreeDocument76 pagesJob-Order Costing: Chapter Threejaz hoodNo ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument66 pagesSystems Design: Job-Order Costing: Chapter ThreeSHAF KHANNo ratings yet

- Job-Order Costing: Chapter ThreeDocument68 pagesJob-Order Costing: Chapter ThreeMd Hasibul Karim 1811766630No ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument66 pagesSystems Design: Job-Order Costing: Chapter ThreeKerby Gail RulonaNo ratings yet

- ACT 202 Chapter 3 - UpdatedDocument53 pagesACT 202 Chapter 3 - UpdatedAminaMatinNo ratings yet

- Chapters 2 & 3.: Job-Order CostingDocument83 pagesChapters 2 & 3.: Job-Order CostingsaraNo ratings yet

- Chap18 - DNGNDocument58 pagesChap18 - DNGNĐàm Ngọc Giang NamNo ratings yet

- Hms 03Document52 pagesHms 03JavierNo ratings yet

- Production Methods: Batch Production Job Production Mass Production Flow Production Cellular ManufacturingDocument2 pagesProduction Methods: Batch Production Job Production Mass Production Flow Production Cellular Manufacturingjuan pablo rodriguez romeroNo ratings yet

- Systems Design-Process CostingDocument58 pagesSystems Design-Process CostingSederiku KabaruzaNo ratings yet

- Job CostingDocument26 pagesJob CostingpriyankaNo ratings yet

- CH 04Document30 pagesCH 04Giang Nguyễn TràNo ratings yet

- Job CostDocument20 pagesJob CostPreetika AgarwalNo ratings yet

- Accounting For Joint ProductsDocument16 pagesAccounting For Joint ProductsVince Christian PadernalNo ratings yet

- Product Costing How To Calculate The Cost of A Product or A Service?Document13 pagesProduct Costing How To Calculate The Cost of A Product or A Service?FAEETNo ratings yet

- 4to IB - Cycle 26 - Production MethodsDocument26 pages4to IB - Cycle 26 - Production MethodsDaniela SánchezNo ratings yet

- Variable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncDocument30 pagesVariable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncInga ApseNo ratings yet

- Chap007 27102021 110417amDocument30 pagesChap007 27102021 110417amAzaz IftikharNo ratings yet

- Chapter 03 Systems Design Job-Order CostingDocument38 pagesChapter 03 Systems Design Job-Order CostingFarihaNo ratings yet

- Job Cost AccDocument50 pagesJob Cost AccJason CNo ratings yet

- Inventory Costing: Chapter NineDocument39 pagesInventory Costing: Chapter NineDio VinosaNo ratings yet

- Review Chapter 1-2-4-18Document55 pagesReview Chapter 1-2-4-18hoangmyduyennguyen2004No ratings yet

- FET 9 Types of ProductionDocument18 pagesFET 9 Types of ProductionRoshanRSVNo ratings yet

- Topic 3 - Process CostingDocument30 pagesTopic 3 - Process CostingArvhenn BarcelonaNo ratings yet

- Job Order CostingDocument63 pagesJob Order CostingGhillian Mae GuiangNo ratings yet

- Cost Acc Chapter 12Document8 pagesCost Acc Chapter 12ElleNo ratings yet

- Variable Costing: A Tool For Management: Mcgraw-Hill/IrwinDocument40 pagesVariable Costing: A Tool For Management: Mcgraw-Hill/IrwinAbed Al-Rahman SalehNo ratings yet

- Chapter 2 - Overview of ManufacturingDocument56 pagesChapter 2 - Overview of ManufacturingOlward TôNo ratings yet

- Chap03notes PDFDocument79 pagesChap03notes PDFElla maeNo ratings yet

- Joint Product and by ProductDocument8 pagesJoint Product and by ProductMihir ThakurNo ratings yet

- Variable Costing: A Tool For Management: Chapter SevenDocument37 pagesVariable Costing: A Tool For Management: Chapter SevenJavier TsangNo ratings yet

- Chapter 6 Process CostingDocument76 pagesChapter 6 Process Costingumar afzalNo ratings yet

- Management Accounting Chapter 5&6Document84 pagesManagement Accounting Chapter 5&6yimerNo ratings yet

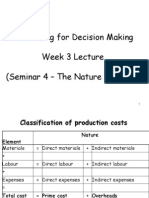

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- AF3112 Lec 5 Joint and By-Product CostingDocument12 pagesAF3112 Lec 5 Joint and By-Product CostingRoseNo ratings yet

- Cost Calculation Models. An OverviewDocument12 pagesCost Calculation Models. An OverviewRoksoliana PankovskaNo ratings yet

- Chapter 2 Cost ClassificationsDocument18 pagesChapter 2 Cost Classificationsmarizemeyer2No ratings yet

- Chap004 7e EditedDocument47 pagesChap004 7e EditedfarahNo ratings yet

- 2AB3 Final Cribsheet 1Document2 pages2AB3 Final Cribsheet 1aymangbaNo ratings yet

- Jordan Managment Accounting 61Document41 pagesJordan Managment Accounting 61Ace RividiNo ratings yet

- Job OrderDocument69 pagesJob OrderSweet EmmeNo ratings yet

- Cost Accounting SystemsDocument4 pagesCost Accounting SystemsEDELYN PoblacionNo ratings yet

- Hms 02Document64 pagesHms 02JavierNo ratings yet

- CH 4Document16 pagesCH 4Euis Muliawaty NNo ratings yet

- Job-Order Costing: An Overview: Job-Order Costing Systems Are Used When: Job-Order Costing Systems Are Used WhenDocument72 pagesJob-Order Costing: An Overview: Job-Order Costing Systems Are Used When: Job-Order Costing Systems Are Used WhenRifat Tasfia OtriNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinNo ratings yet

- Price ReviewerDocument3 pagesPrice ReviewerTheresse BalmoridaNo ratings yet

- Desain Sistem: Perhitungan Biaya Berdasarkan Pesanan: (Job Order Costing)Document53 pagesDesain Sistem: Perhitungan Biaya Berdasarkan Pesanan: (Job Order Costing)AriniNo ratings yet

- ACCY918 T3 2023 Wk3 Process Costing Lecture NoteDocument82 pagesACCY918 T3 2023 Wk3 Process Costing Lecture NoteNIRAJ SharmaNo ratings yet

- Chapter-8 Unit - Batch CostingDocument8 pagesChapter-8 Unit - Batch CostingAdi PrajapatiNo ratings yet

- Samiksha Gupta - Asst - Manager - CompressedDocument2 pagesSamiksha Gupta - Asst - Manager - CompressedsamikshaguptagsmrNo ratings yet

- Part 1-15 Points Ais: Role and Purpose Answer: A Structured Procedure For Collecting Data, Processing The Data Into Information, and DeliveringDocument2 pagesPart 1-15 Points Ais: Role and Purpose Answer: A Structured Procedure For Collecting Data, Processing The Data Into Information, and DeliveringPrimeNo ratings yet

- CH 5Document134 pagesCH 5Shanelle SilmaroNo ratings yet

- Quiz - CPM and PertDocument1 pageQuiz - CPM and PertAngel RavenNo ratings yet

- TB Raiborn - Activity-Based Management and Activity-Based CostingDocument31 pagesTB Raiborn - Activity-Based Management and Activity-Based Costingjayrjoshuavillapando100% (1)

- Sap Material Management Configuration Manual: Prepared byDocument60 pagesSap Material Management Configuration Manual: Prepared bydudhmogre23No ratings yet

- Lean and Continuous Improvement - XDocument3 pagesLean and Continuous Improvement - XjozsefczNo ratings yet

- (STANDARD) NATO ProcurementDocument44 pages(STANDARD) NATO ProcurementSekwah HawkesNo ratings yet

- Foundations of Planning Lec 5Document27 pagesFoundations of Planning Lec 5Rajja RashadNo ratings yet

- Sales Manager Beverage Hospitality in San Diego CA Resume Joel HerzerDocument1 pageSales Manager Beverage Hospitality in San Diego CA Resume Joel HerzerJoelHerzerNo ratings yet

- Auditing I (Acct 411) : Unit 1: Overview of AuditingDocument30 pagesAuditing I (Acct 411) : Unit 1: Overview of Auditingsamuel debebeNo ratings yet

- Manage Suppliers With Teamcenter Vendor ManagementDocument2 pagesManage Suppliers With Teamcenter Vendor ManagementAkkshhey JadhavNo ratings yet

- RESUME - Linda Allonge-BybeeDocument2 pagesRESUME - Linda Allonge-BybeeRuthie TrentNo ratings yet

- MogadishuDocument3 pagesMogadishumohee1315No ratings yet

- Certified ETL Testing ProfessionalDocument6 pagesCertified ETL Testing ProfessionalAnamika VermaNo ratings yet

- Green and White Corporate Technology Business Plan PresentationDocument19 pagesGreen and White Corporate Technology Business Plan PresentationA4K74 HUPNo ratings yet

- Corporate Brochure ESCP EuropeDocument48 pagesCorporate Brochure ESCP EuropeJohn KusakNo ratings yet

- An Investment Perspective of Human Resources 03Document14 pagesAn Investment Perspective of Human Resources 03kutubiNo ratings yet

- Business AnalystDocument27 pagesBusiness AnalystSaurabh DalviNo ratings yet

- Managerial Accounting Concepts and Principles: Mcgraw-Hill/Irwin © The Mcgraw-Hill Companies, Inc., 2005Document40 pagesManagerial Accounting Concepts and Principles: Mcgraw-Hill/Irwin © The Mcgraw-Hill Companies, Inc., 2005Fear Part 2No ratings yet

- Chapter 2 SlidesDocument95 pagesChapter 2 SlidesMukesh KumarNo ratings yet

- Drabek - Quarantelli Theory Award Lecture - Social ProblemsDocument117 pagesDrabek - Quarantelli Theory Award Lecture - Social ProblemszylfielNo ratings yet

- ShubhamDocument34 pagesShubhamshubham kumarNo ratings yet

- Icici CRMDocument13 pagesIcici CRMSachin ChaudhryNo ratings yet

- Review of Related Literautre and StudiesDocument16 pagesReview of Related Literautre and StudiesJT SaguinNo ratings yet