You might also like

- The Little Blue Book On SchedulingDocument105 pagesThe Little Blue Book On Schedulingparagjain007No ratings yet

- BAB 2024 CH06 - Cost Volume Profit Analysis-Add - Issue.Document74 pagesBAB 2024 CH06 - Cost Volume Profit Analysis-Add - Issue.mini3110No ratings yet

- ch02 (4) 2Document61 pagesch02 (4) 2lanamr374No ratings yet

- CH 06Document62 pagesCH 06Abdallah AlfaqiehNo ratings yet

- CVP AnalysisDocument15 pagesCVP AnalysisAkhil JasrotiaNo ratings yet

- Cost Volume ProfitDocument24 pagesCost Volume ProfitRomuell BanaresNo ratings yet

- Chapter 3 - Cost-Volume-Profit RelationshipDocument9 pagesChapter 3 - Cost-Volume-Profit Relationshipjoseph planasNo ratings yet

- Managerial Accounting Ch06Document33 pagesManagerial Accounting Ch06Mohammed HassanNo ratings yet

- Cost and Managerial Accounting LL Chap 1Document60 pagesCost and Managerial Accounting LL Chap 1fekadegebretsadik478729No ratings yet

- Kinney 8e - CH 09Document17 pagesKinney 8e - CH 09Ashik Uz ZamanNo ratings yet

- Introduction To Cost Behavior and Cost-Volume Relationships: Learning ObjectivesDocument20 pagesIntroduction To Cost Behavior and Cost-Volume Relationships: Learning ObjectivesCarla GarciaNo ratings yet

- CVP AnalysisDocument26 pagesCVP AnalysisChandan JobanputraNo ratings yet

- 9003 CVP AnalysisDocument7 pages9003 CVP AnalysisSirNo ratings yet

- 03 CVP AnalysisDocument13 pages03 CVP AnalysisKenneth Marcial EgeNo ratings yet

- Chap 05 - Study GuideDocument14 pagesChap 05 - Study Guidedimitra triantosNo ratings yet

- CH 6 Cost Volume Profit Revised Mar 18Document84 pagesCH 6 Cost Volume Profit Revised Mar 18beccafabbriNo ratings yet

- Cost II Chapter1Document9 pagesCost II Chapter1Dureti NiguseNo ratings yet

- Analyzing Cost-Volume-Profit IssuesDocument55 pagesAnalyzing Cost-Volume-Profit IssuesVaisal AmirNo ratings yet

- 012 CAMIST CH10 Amndd 2 HS PP 247-276 Branded BW SecDocument31 pages012 CAMIST CH10 Amndd 2 HS PP 247-276 Branded BW Secsumaiazerin101No ratings yet

- MAS - CVP AnalysisDocument18 pagesMAS - CVP AnalysisDane Enterna50% (2)

- 8 - Operating and Financial LeverageDocument15 pages8 - Operating and Financial LeverageClariz VelasquezNo ratings yet

- "Variable Costing", "Differential Costing" or "Out-Of-Pocket" CostingDocument10 pages"Variable Costing", "Differential Costing" or "Out-Of-Pocket" CostingSANTHOSH KUMAR T MNo ratings yet

- Unit 4 - Marginal CostingDocument12 pagesUnit 4 - Marginal CostingHitesh VNo ratings yet

- CVP Sensitivity Analysis LmsDocument34 pagesCVP Sensitivity Analysis LmsnavalojiniravindranNo ratings yet

- Cost-Volume-Profit Analysis: Study ObjectiveDocument12 pagesCost-Volume-Profit Analysis: Study ObjectiveGracelle Mae OrallerNo ratings yet

- L5 - Cost - Volume - Profit AnalysisDocument47 pagesL5 - Cost - Volume - Profit AnalysisAbhishek TyagiNo ratings yet

- CH 19Document56 pagesCH 19Ahmed El KhateebNo ratings yet

- CVP AnalysisDocument37 pagesCVP Analysis20B81A1235cvr.ac.in G RUSHI BHARGAVNo ratings yet

- CVP Analysis (Theory Math)Document28 pagesCVP Analysis (Theory Math)Ariyan ShantoNo ratings yet

- Chapter 3 Marginal Costing and Break Even AnalysisDocument31 pagesChapter 3 Marginal Costing and Break Even AnalysisAjinkya NaikNo ratings yet

- Cost-Volume-Profit (CVP) Analysis: Cmu SPDocument3 pagesCost-Volume-Profit (CVP) Analysis: Cmu SPKuya ANo ratings yet

- CVP Analysis: Shiri PaduriDocument9 pagesCVP Analysis: Shiri Padurivardha rajuNo ratings yet

- M5 Cost-Volume Profit Analysis As Managerial Planing ToolDocument6 pagesM5 Cost-Volume Profit Analysis As Managerial Planing Toolwingsenigma 00No ratings yet

- Chapter 6:part Two Cost-Volume-ProfitDocument44 pagesChapter 6:part Two Cost-Volume-ProfitFidelina CastroNo ratings yet

- CH 005Document24 pagesCH 005melodie03100% (2)

- Chapter 7Document55 pagesChapter 7bhagyeshparekh.caNo ratings yet

- Lecture 4 - Cost Volume Profit AnalysisDocument19 pagesLecture 4 - Cost Volume Profit AnalysisRODOLFO AUSTRIA JR.No ratings yet

- CVP Analysis 1Document20 pagesCVP Analysis 1RoyalNo ratings yet

- Cost-Volume-Profit Analysis: A Managerial Planning Tool Break-Even Point in UnitsDocument3 pagesCost-Volume-Profit Analysis: A Managerial Planning Tool Break-Even Point in UnitsHafizh GalihNo ratings yet

- CVP AnalysisDocument18 pagesCVP AnalysisKashvi MakadiaNo ratings yet

- Break Even PointDocument4 pagesBreak Even PointabhinaymarupakulaNo ratings yet

- AE11 Man Econ Module 3-4Document51 pagesAE11 Man Econ Module 3-4Jynilou PinoteNo ratings yet

- Marginal Costing For Decision Making & CVP Analysis: 5BA - Business Accounting For Non-SpecialistsDocument11 pagesMarginal Costing For Decision Making & CVP Analysis: 5BA - Business Accounting For Non-SpecialistsSravya MagantiNo ratings yet

- Chapter 5 - CVP Analysis Part 2 - UpdatedDocument17 pagesChapter 5 - CVP Analysis Part 2 - UpdatedrasmimoqbelNo ratings yet

- Chapter 6Document57 pagesChapter 6Léo Audibert75% (4)

- Breakeven Analysis UnderstandingDocument12 pagesBreakeven Analysis UnderstandingSamreen LodhiNo ratings yet

- Cost Volume Profit Analysis: Meaning Purpose Assumptions TechniquesDocument36 pagesCost Volume Profit Analysis: Meaning Purpose Assumptions TechniquesreaderNo ratings yet

- Break-Even AnalysisDocument37 pagesBreak-Even Analysismablekos13No ratings yet

- 12 - Breakeven AnalysisDocument4 pages12 - Breakeven AnalysisMohammad ImaduddinNo ratings yet

- Lecture 4 - Cost Volume Profit AnalysisDocument19 pagesLecture 4 - Cost Volume Profit AnalysisHiyakishu SanNo ratings yet

- Topic 3 - CVP AnalysisDocument31 pagesTopic 3 - CVP AnalysiskajaleNo ratings yet

- Unit2 ModuleDocument29 pagesUnit2 ModuleJasper John NacuaNo ratings yet

- Lecture Notes: Learning Objective 1: Explain How Changes in Activity Affect Contribution Margin and Net Operating IncomeDocument16 pagesLecture Notes: Learning Objective 1: Explain How Changes in Activity Affect Contribution Margin and Net Operating IncomeĐức LộcNo ratings yet

- Chapter 4 Cost Accounting HorngrenDocument23 pagesChapter 4 Cost Accounting HorngrenNHNo ratings yet

- CVP AnalysisDocument31 pagesCVP AnalysisSudhanshu SharmaNo ratings yet

- 04 Mas - CVPDocument8 pages04 Mas - CVPKarlo D. ReclaNo ratings yet

- ACCT 1162 Contabilidad PowerpointDocument20 pagesACCT 1162 Contabilidad PowerpointMariane Sales-LunaNo ratings yet

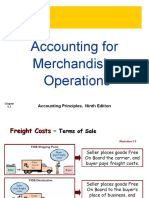

- Accounting For Merchandising Operations: Accounting Principles, Ninth EditionDocument17 pagesAccounting For Merchandising Operations: Accounting Principles, Ninth EditionMehedi HasanNo ratings yet

- II. COST-VOLUME-PROFIT-ANALYSIS (Chapter 5)Document6 pagesII. COST-VOLUME-PROFIT-ANALYSIS (Chapter 5)Karl BasaNo ratings yet

- Profit Planning and Cost-Volume-Profit AnalysisDocument24 pagesProfit Planning and Cost-Volume-Profit AnalysisFallen Hieronymus50% (2)

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- African Language PoliciesDocument121 pagesAfrican Language PoliciesBradNo ratings yet

- Gsic Lexus Is350300 250 200d Gse 202122 Ale20 2010 2012Document22 pagesGsic Lexus Is350300 250 200d Gse 202122 Ale20 2010 2012joelsimpson171001toy100% (137)

- Ice-Carb High Performance Internal Coolant Drills For Drilling Depths Up To 7XdDocument4 pagesIce-Carb High Performance Internal Coolant Drills For Drilling Depths Up To 7XdalphatoolsNo ratings yet

- V1 Exam 1 AfternoonDocument31 pagesV1 Exam 1 AfternoonajnigelNo ratings yet

- Muhammad Arham CVDocument2 pagesMuhammad Arham CVHaseeb AhmedNo ratings yet

- Kunal RawatDocument4 pagesKunal RawatGuar GumNo ratings yet

- DEVICE Exp 4 StudentDocument4 pagesDEVICE Exp 4 StudentTouhid AlamNo ratings yet

- Sf2460i Line 163Document123 pagesSf2460i Line 163Santiago SilvaNo ratings yet

- WHLP Q2 W7Document7 pagesWHLP Q2 W7Sharlyn JunioNo ratings yet

- In Uence of Fatigue Loading in Shear Failures of Reinforced Concrete Members Without Transverse ReinforcementDocument14 pagesIn Uence of Fatigue Loading in Shear Failures of Reinforced Concrete Members Without Transverse ReinforcementSai CharanNo ratings yet

- Class 6 Social PaperDocument5 pagesClass 6 Social PaperManav RachchhNo ratings yet

- Math4 q2 Mod6 FindingtheLCM v3 - For MergeDocument21 pagesMath4 q2 Mod6 FindingtheLCM v3 - For MergeJoanna GarciaNo ratings yet

- Group 2I - Herman Miller Case AnalysisDocument7 pagesGroup 2I - Herman Miller Case AnalysisRishabh Kothari100% (1)

- Introducing and Exchanging Personal Information: Practice 1Document11 pagesIntroducing and Exchanging Personal Information: Practice 1Riyan RiyanuartzNo ratings yet

- Understanding The Dairy Cow Third Edition John Webster All ChapterDocument77 pagesUnderstanding The Dairy Cow Third Edition John Webster All Chaptereric.ward851100% (8)

- DFT Notes PDFDocument4 pagesDFT Notes PDFkrishna prasad ghantaNo ratings yet

- Workshop As Social Setting For Paul's Missionary PreachingDocument14 pagesWorkshop As Social Setting For Paul's Missionary Preaching31songofjoyNo ratings yet

- Geol 105LDocument6 pagesGeol 105LDeron ZiererNo ratings yet

- Hovadik & Larue 2007 Connectivity ReviewDocument17 pagesHovadik & Larue 2007 Connectivity ReviewASKY PNo ratings yet

- MFG Technical Design Guide FRP Composite 0Document25 pagesMFG Technical Design Guide FRP Composite 0thiyakiNo ratings yet

- Eligible Students - SoCDocument39 pagesEligible Students - SoCaaqilumri20No ratings yet

- Valley Metro System MapDocument1 pageValley Metro System MapLục Ẩn ĐạtNo ratings yet

- Resume Template & Cover Letter Bu YoDocument28 pagesResume Template & Cover Letter Bu YoatinnajahkamalasariNo ratings yet

- Workshop 3 - MathsDocument5 pagesWorkshop 3 - MathsJuan David Bernal QuinteroNo ratings yet

- Unit 2Document7 pagesUnit 2Hind HindouNo ratings yet

- Mazda3 Takuya Brochure July 10Document3 pagesMazda3 Takuya Brochure July 10Rujisak MuangsongNo ratings yet

- Agricultural Revolution - Industrial RevolutionDocument2 pagesAgricultural Revolution - Industrial RevolutionJenni SilvaNo ratings yet

- Lesson 1Document35 pagesLesson 1Irish GandolaNo ratings yet

- 2Document1 page2Dedes SahpitraNo ratings yet