You might also like

- Price Action (Strat's Stress Free Trading) - ActiverDocument11 pagesPrice Action (Strat's Stress Free Trading) - Activerrsousa1No ratings yet

- Accounting for Special Partnership TransactionsDocument15 pagesAccounting for Special Partnership TransactionsJessaNo ratings yet

- REGULATORY FRAMEWORK FOR BUSINESSDocument28 pagesREGULATORY FRAMEWORK FOR BUSINESSTrixie de LeonNo ratings yet

- University of Santo TomasDocument12 pagesUniversity of Santo TomasJEFFERSON CUTENo ratings yet

- Digital Exam Questions on Installment Sales AccountingDocument213 pagesDigital Exam Questions on Installment Sales AccountingAngelica RubiosNo ratings yet

- PAS 19 (Revised) Employee BenefitsDocument35 pagesPAS 19 (Revised) Employee BenefitsReynaldNo ratings yet

- METALLIC DENTURE BASE MATERIALSDocument57 pagesMETALLIC DENTURE BASE MATERIALSDRNIRBANMITRA100% (9)

- PFRS 7Document22 pagesPFRS 7Princess Jullyn ClaudioNo ratings yet

- ICICI Prudential Project ReportDocument54 pagesICICI Prudential Project Report-=[Yo9esh]=-81% (31)

- Segment and Interim Reporting QuestionsDocument2 pagesSegment and Interim Reporting QuestionsralphalonzoNo ratings yet

- Accounting For LaborDocument1 pageAccounting For LaborkwekwkNo ratings yet

- Problem 14-5: Kayla Cruz & Gabriel TekikoDocument7 pagesProblem 14-5: Kayla Cruz & Gabriel TekikoNURHAM SUMLAYNo ratings yet

- Separate and Consolidated Dayag Part 3Document4 pagesSeparate and Consolidated Dayag Part 3Edi wow WowNo ratings yet

- Chapter 3 Financial Statement Analysis ExercisesDocument6 pagesChapter 3 Financial Statement Analysis ExercisesCatherine VenturaNo ratings yet

- Assignment On SC and VADocument12 pagesAssignment On SC and VAVixen Aaron EnriquezNo ratings yet

- Revision Questions - Q&ADocument3 pagesRevision Questions - Q&Arosario correiaNo ratings yet

- EstimationDocument2 pagesEstimationJet jet Gonzales0% (1)

- IA2 CH15A PROBLEMS (Vhinson)Document5 pagesIA2 CH15A PROBLEMS (Vhinson)sophomorefilesNo ratings yet

- International Business 3Document45 pagesInternational Business 3Ken TuazonNo ratings yet

- Intermediate Accounting 3 Basic and Diluted Earnings Per Share: Quiz 11Document1 pageIntermediate Accounting 3 Basic and Diluted Earnings Per Share: Quiz 11Airon BendañaNo ratings yet

- Intermediate Accounting III ReviewerDocument3 pagesIntermediate Accounting III ReviewerRenalyn PascuaNo ratings yet

- SLU SAMCIS Course Guide on Financial MarketsDocument6 pagesSLU SAMCIS Course Guide on Financial MarketsFernando III PerezNo ratings yet

- Quiz 5 Problems Second Semester AY2223 With AnswersDocument4 pagesQuiz 5 Problems Second Semester AY2223 With AnswersManzano, Carl Clinton Neil D.No ratings yet

- ILLUSTRATIONS - Government AccountingDocument10 pagesILLUSTRATIONS - Government AccountingKathleenNo ratings yet

- Chapter 8 SolucionesDocument6 pagesChapter 8 SolucionesIvetteFabRuizNo ratings yet

- Commission On Audit:: Government Accounting Manual (Gam) Pointers CA51027Document4 pagesCommission On Audit:: Government Accounting Manual (Gam) Pointers CA51027Carl Dhaniel Garcia SalenNo ratings yet

- (Solution Answers) Advanced Accounting by Dayag, Version 2017 - Chapter 1 (Partnership) - Answers On Multiple Choice Computation #21 To 25Document1 page(Solution Answers) Advanced Accounting by Dayag, Version 2017 - Chapter 1 (Partnership) - Answers On Multiple Choice Computation #21 To 25John Carlos DoringoNo ratings yet

- Current Liabilities - QuizDocument4 pagesCurrent Liabilities - QuizArvin PaculanangNo ratings yet

- Module Part I Preface To UNIT I PDFDocument43 pagesModule Part I Preface To UNIT I PDFsvpsNo ratings yet

- Chap10 (Accounts Receivable and Inventory Management) VanHorne&Brigham, CabreaDocument3 pagesChap10 (Accounts Receivable and Inventory Management) VanHorne&Brigham, CabreaJollibee JollibeeeNo ratings yet

- Ma2 Project Screening Projec Ranking and Capital RationingDocument11 pagesMa2 Project Screening Projec Ranking and Capital RationingMangoStarr Aibelle Vegas100% (1)

- Exam in Accounting-FinalsDocument5 pagesExam in Accounting-FinalsIyarna YasraNo ratings yet

- M2u Classification Individual Taxation P1Document30 pagesM2u Classification Individual Taxation P1Xehdrickke FernandezNo ratings yet

- Solution Manual-Module 1: Acc 311 - Acctg For Special Transactions and Business CombinationsDocument11 pagesSolution Manual-Module 1: Acc 311 - Acctg For Special Transactions and Business CombinationsJoy SantosNo ratings yet

- ADDITIONAL PROBLEMS Variable and Absorption and ABCDocument2 pagesADDITIONAL PROBLEMS Variable and Absorption and ABCkaizen shinichiNo ratings yet

- Chapter 15 Miscellaneous TopicsDocument6 pagesChapter 15 Miscellaneous TopicsAngelica Joy ManaoisNo ratings yet

- Repealed PD 692 Known As Revised Accountancy LawDocument8 pagesRepealed PD 692 Known As Revised Accountancy LawLian RamirezNo ratings yet

- Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument7 pagesIas 8 Accounting Policies, Changes in Accounting Estimates and Errorsmusic niNo ratings yet

- 4a Standard Costs and Analysis of VariancesDocument3 pages4a Standard Costs and Analysis of VariancesGina TingdayNo ratings yet

- Midterm Exam Parcor 2020Document1 pageMidterm Exam Parcor 2020John Alfred CastinoNo ratings yet

- Comprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFDocument9 pagesComprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFamie honnagNo ratings yet

- Final Proj Sy2022-23 Agrigulay Corp.Document4 pagesFinal Proj Sy2022-23 Agrigulay Corp.Jan Elaine CalderonNo ratings yet

- Total Assets 402,000 96,000 430,800Document2 pagesTotal Assets 402,000 96,000 430,800Melwin CalubayanNo ratings yet

- RFBT Answer Key Chapter 1 To 4Document4 pagesRFBT Answer Key Chapter 1 To 4Feelingerang MAYoraNo ratings yet

- Chapter 4 - Seat Work - Assignment #4 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDocument3 pagesChapter 4 - Seat Work - Assignment #4 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDonise Ronadel SantosNo ratings yet

- Quiz Assignment 4 Costing ProblemsDocument2 pagesQuiz Assignment 4 Costing ProblemsRocel Domingo0% (1)

- Effect of Working Capital Management and Financial Leverage On Financial Performance of Philippine FirmsDocument9 pagesEffect of Working Capital Management and Financial Leverage On Financial Performance of Philippine FirmsGeorgina De LiañoNo ratings yet

- Prelim Exam: Name: Date: Professor: Section: ScoreDocument13 pagesPrelim Exam: Name: Date: Professor: Section: ScoreJoyce LunaNo ratings yet

- Chapter 10 - AnswerDocument15 pagesChapter 10 - AnswerAgentSkySkyNo ratings yet

- 4 2 Endless Company PDFDocument3 pages4 2 Endless Company PDFJulius Mark Carinhay TolitolNo ratings yet

- Chapter 15 PDFDocument12 pagesChapter 15 PDFDarijun SaldañaNo ratings yet

- Chapter 17 BBDocument48 pagesChapter 17 BBTaVuKieuNhiNo ratings yet

- Chapter 6 - Income Tax For PartnershipDocument40 pagesChapter 6 - Income Tax For PartnershipNineteen AùgùstNo ratings yet

- Far Ii Finals ProblemDocument17 pagesFar Ii Finals ProblemSaeym SegoviaNo ratings yet

- Accounting for Investment in AssociatesDocument2 pagesAccounting for Investment in AssociatesRanee DeeNo ratings yet

- Qa PartnershipDocument9 pagesQa PartnershipFaker MejiaNo ratings yet

- AssesmentDocument12 pagesAssesmentMaya Keizel A.No ratings yet

- Capital Budgeting Discounted Method - Discussion Problems - Part 1Document11 pagesCapital Budgeting Discounted Method - Discussion Problems - Part 1Deryl GalveNo ratings yet

- Labor Variance: By: Group 2Document24 pagesLabor Variance: By: Group 2Kris BayronNo ratings yet

- Costing ModuleDocument7 pagesCosting ModuleJoneric RamosNo ratings yet

- Problems: Problem 4 - 1Document4 pagesProblems: Problem 4 - 1KioNo ratings yet

- Shutting Down or Continuing To Operate A Plant - Hallas CompanyDocument3 pagesShutting Down or Continuing To Operate A Plant - Hallas CompanyFernando III PerezNo ratings yet

- Forming a Partnership and Calculating Capital AccountsDocument5 pagesForming a Partnership and Calculating Capital AccountsCarl Dhaniel Garcia SalenNo ratings yet

- Quiz 1 Afar 1Document13 pagesQuiz 1 Afar 1Rujean Salar AltejarNo ratings yet

- Chapter 13 Capital Investment DecisionsDocument28 pagesChapter 13 Capital Investment Decisionsmuhammad alfariziNo ratings yet

- 178.200 06-5Document34 pages178.200 06-5api-3860979100% (1)

- Portfolio Risk and Return: Part I: Presenter Venue DateDocument35 pagesPortfolio Risk and Return: Part I: Presenter Venue DateahmedNo ratings yet

- 2010 Form 990 For President and Fellows of Harvard CollegeDocument254 pages2010 Form 990 For President and Fellows of Harvard CollegeresponsibleharvardNo ratings yet

- Costs of An Initial Public Offering-Grant ThorntonDocument7 pagesCosts of An Initial Public Offering-Grant ThorntonSS CORPORATE SERVICESNo ratings yet

- SIP Presentation On AU Small Finance BankDocument13 pagesSIP Presentation On AU Small Finance BankMadhurNo ratings yet

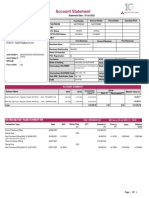

- Account StatementDocument3 pagesAccount Statementsia kamathNo ratings yet

- Classic Theories of Economic Growth and DevelopmentDocument16 pagesClassic Theories of Economic Growth and DevelopmentGWYNETH SYBIL BATACANNo ratings yet

- Akshay's ResumeDocument1 pageAkshay's ResumeakshayNo ratings yet

- MIT Economics Notes OCWDocument192 pagesMIT Economics Notes OCWfindingfelicityNo ratings yet

- Accounting For Shares NewDocument24 pagesAccounting For Shares NewSteve NtefulNo ratings yet

- Personal Income Tax AllowancesDocument2 pagesPersonal Income Tax AllowancesShivam ThaliaNo ratings yet

- Woven SacksDocument27 pagesWoven Sacksbig johnNo ratings yet

- Passive Income EbookDocument7 pagesPassive Income EbookColombia Exótica ToursNo ratings yet

- Index Page - SAP Transaction Codes - Character ADocument689 pagesIndex Page - SAP Transaction Codes - Character AAurino DjamarisNo ratings yet

- IAS 2 - InventoriesDocument17 pagesIAS 2 - InventoriesraopraniNo ratings yet

- THEJASWINI ProjectDocument112 pagesTHEJASWINI Projectswamy yashuNo ratings yet

- "How Well Am I Doing?" Financial Statement AnalysisDocument61 pages"How Well Am I Doing?" Financial Statement AnalysisSederiku KabaruzaNo ratings yet

- Full Download Test Bank For Portfolio Construction Management and Protection 5th Edition Strong PDF Full ChapterDocument35 pagesFull Download Test Bank For Portfolio Construction Management and Protection 5th Edition Strong PDF Full Chaptershaps.tortillayf3th100% (20)

- Valuation HandbookDocument1 pageValuation HandbookbaronfgfNo ratings yet

- Financial Performance Analysis of TeslaDocument20 pagesFinancial Performance Analysis of TeslaDaniel WambuaNo ratings yet

- Market Making and Mean Reversion: Tanmoy Chakraborty Tanmoy@seas - Upenn.edu Michael Kearns Mkearns@cis - Upenn.eduDocument7 pagesMarket Making and Mean Reversion: Tanmoy Chakraborty Tanmoy@seas - Upenn.edu Michael Kearns Mkearns@cis - Upenn.eduIrfan SihabNo ratings yet

- The History of Jollibee Dates Back To 1975Document4 pagesThe History of Jollibee Dates Back To 1975Jayson MendozaNo ratings yet

- Ch08-Ppt-Risk and Rates of Return-1Document46 pagesCh08-Ppt-Risk and Rates of Return-1muhammadosama100% (1)

- Pertemuan 3 - IAS 1 - Paper For Discussion PDFDocument23 pagesPertemuan 3 - IAS 1 - Paper For Discussion PDFSlamet RaharjoNo ratings yet

- LEM IR FY 2018 19 WebDocument52 pagesLEM IR FY 2018 19 WebAbhishekAdhikaryNo ratings yet