You might also like

- Economic Development Chap. 3. Classic Theories of Economic Growth and DevelopmentDocument32 pagesEconomic Development Chap. 3. Classic Theories of Economic Growth and DevelopmentSoothing BlendNo ratings yet

- Chapter 4Document34 pagesChapter 4Hameed GulNo ratings yet

- Phasor Estimation and Modelling Techniques of PMU A Rev - 2017 - Energy Procedi PDFDocument14 pagesPhasor Estimation and Modelling Techniques of PMU A Rev - 2017 - Energy Procedi PDFAmar HodžicNo ratings yet

- The Benefits of Mobile Data How Can They Be Realised ?: Task Force 35.07Document70 pagesThe Benefits of Mobile Data How Can They Be Realised ?: Task Force 35.07John HarlandNo ratings yet

- BNEF Overview and Proposal For PT PLN - Revised Without SummitDocument28 pagesBNEF Overview and Proposal For PT PLN - Revised Without SummitlantangNo ratings yet

- Regulations in IndiaDocument8 pagesRegulations in IndiaHimanshu GuptaNo ratings yet

- A Framework For Mission-Oriented Policy Roadmapping For The Sdgs FinalDocument61 pagesA Framework For Mission-Oriented Policy Roadmapping For The Sdgs FinalaryNo ratings yet

- Foreign Investment Drives Nigeria's Economic GrowthDocument136 pagesForeign Investment Drives Nigeria's Economic GrowthFaith MoneyNo ratings yet

- Md. Sohel (11803022)Document13 pagesMd. Sohel (11803022)Sohel AhmedNo ratings yet

- Isp LicenseDocument36 pagesIsp LicenseVijay Dhokchoule PatilNo ratings yet

- Mesi 1.0Document8 pagesMesi 1.0Ida Suzana HussainNo ratings yet

- Indian Takeover CodeDocument10 pagesIndian Takeover CodeMoiz ZakirNo ratings yet

- Full-Paper 1 3Document44 pagesFull-Paper 1 3Kevin MagnoNo ratings yet

- IRENA Coalition Sector Coupling 2022Document40 pagesIRENA Coalition Sector Coupling 2022tudorNo ratings yet

- Public Debt and Economic Growth in India A ReassesDocument9 pagesPublic Debt and Economic Growth in India A ReassesGaran ParutaNo ratings yet

- QF ProjectDocument27 pagesQF Projectmhod omranNo ratings yet

- CAPE - Masterclass On VAT - Dr. Abdul Mannan Shikder Sir - Member (VAT Implementation & IT) NBRDocument115 pagesCAPE - Masterclass On VAT - Dr. Abdul Mannan Shikder Sir - Member (VAT Implementation & IT) NBRbanglauserNo ratings yet

- JISEA - US EnergyDocument92 pagesJISEA - US EnergyahmedNo ratings yet

- Trafficking in Persons ReportDocument382 pagesTrafficking in Persons ReportL'express MauriceNo ratings yet

- PEST Analysis The USADocument8 pagesPEST Analysis The USAMarian Valeria Callejas ÁngelesNo ratings yet

- Indian Tax System OverviewDocument17 pagesIndian Tax System OverviewSachin RanaNo ratings yet

- Foreign Policy ChangeDocument10 pagesForeign Policy ChangeHanny Mohd YunusNo ratings yet

- Eu Eom Kenya 2022 enDocument72 pagesEu Eom Kenya 2022 enThe Star KenyaNo ratings yet

- Copy of IO БилетыDocument73 pagesCopy of IO БилетыS ANo ratings yet

- U of Idaho Associated Students Senate Resolution No. f22-r03Document4 pagesU of Idaho Associated Students Senate Resolution No. f22-r03Valerie OsierNo ratings yet

- Notes - Unit 3Document26 pagesNotes - Unit 3ishita sabooNo ratings yet

- Zero Based Budgeting in IndiaDocument13 pagesZero Based Budgeting in IndiaBandita RoutNo ratings yet

- The Impact of Economic Development Programs and The Potential of Business Incubators in HaitiDocument54 pagesThe Impact of Economic Development Programs and The Potential of Business Incubators in HaitiDrew Mohoric100% (1)

- Libro de Memoerias ICITS 2018Document1,167 pagesLibro de Memoerias ICITS 2018paula andrea lopezNo ratings yet

- Consumer BehaviorDocument29 pagesConsumer Behaviorapi-384238511No ratings yet

- Trade Union Act ComparisonDocument2 pagesTrade Union Act ComparisonBernewsAdminNo ratings yet

- Manonmaniam Sundaranar University: Insurance and Risk ManagementDocument190 pagesManonmaniam Sundaranar University: Insurance and Risk ManagementDevanshu JulkaNo ratings yet

- 2022 CVE G10 UPDATED NOTES Latest-1Document49 pages2022 CVE G10 UPDATED NOTES Latest-1Epriam NgulubeNo ratings yet

- Critical Thoughts From A Government Mindset (New Print Book by DR Ali M. Al-Khouri)Document2 pagesCritical Thoughts From A Government Mindset (New Print Book by DR Ali M. Al-Khouri)Chartridge Books OxfordNo ratings yet

- Yamaha EMX212sDocument35 pagesYamaha EMX212sHaiAu2009No ratings yet

- Managerial Approaches and Organizational Performance of Multinational Enterprises in NigeriaDocument13 pagesManagerial Approaches and Organizational Performance of Multinational Enterprises in NigeriaCentral Asian StudiesNo ratings yet

- Comparing ICICI and IDBI BanksDocument27 pagesComparing ICICI and IDBI BanksGUDDUNo ratings yet

- Detailed AdvertisementDocument5 pagesDetailed AdvertisementKhatikNo ratings yet

- 1393-Quarterly Fiscal Bulletin 2Document41 pages1393-Quarterly Fiscal Bulletin 2Macro Fiscal PerformanceNo ratings yet

- The State of Local Government and Service DeliveryDocument15 pagesThe State of Local Government and Service DeliveryAkin DolapoNo ratings yet

- Critically Differentiate Government ConceptsDocument9 pagesCritically Differentiate Government ConceptsUsman Abubakar100% (1)

- Lecture 9 - Merger Control IIDocument68 pagesLecture 9 - Merger Control IIjoanaNo ratings yet

- Somalia Financial StatementsDocument40 pagesSomalia Financial StatementsNuur CaliNo ratings yet

- Chapter9 QuizDocument3 pagesChapter9 QuizJoey YUNo ratings yet

- RV 2021 Tech Trends ReportDocument35 pagesRV 2021 Tech Trends ReportAyi CkNo ratings yet

- Unfinished Business: Tanzania's Media Capture Challenge: Ryan PowellDocument14 pagesUnfinished Business: Tanzania's Media Capture Challenge: Ryan PowellMichael KaminyogeNo ratings yet

- G20 - WikipediaDocument24 pagesG20 - WikipediaTomy S WardhanaNo ratings yet

- Geels and Turnheim 2022 The Great ReconfigurationDocument394 pagesGeels and Turnheim 2022 The Great ReconfigurationHong Hai HaNo ratings yet

- GOVERNANCEDocument40 pagesGOVERNANCEKanhu ChslNo ratings yet

- Parco: Recruitment & Selection ProcessDocument16 pagesParco: Recruitment & Selection Processasif tajNo ratings yet

- CBN Rule Book Volume 1Document1,279 pagesCBN Rule Book Volume 1Justus Ohakanu100% (1)

- Islamic Bonds: Learning ObjectivesDocument20 pagesIslamic Bonds: Learning ObjectivesAbdelnasir HaiderNo ratings yet

- Chapter 7. RemediesDocument46 pagesChapter 7. RemediestejaswiniNo ratings yet

- Pakistan in Regional Affairs 30052022 104215amDocument19 pagesPakistan in Regional Affairs 30052022 104215amYusra Rehman KhanNo ratings yet

- Telecommunications November 2021Document42 pagesTelecommunications November 2021Tania ChakrabortyNo ratings yet

- India CW CAT 1Document88 pagesIndia CW CAT 1AAKASH GOPALNo ratings yet

- Empowering People Through Skilling Under CSR of TATA Power-DDLDocument26 pagesEmpowering People Through Skilling Under CSR of TATA Power-DDLGourab GogoiNo ratings yet

- Chapter 3 - Financial Reporting StandardsDocument9 pagesChapter 3 - Financial Reporting StandardsFardin Ahmed 2011823630No ratings yet

- Comparing Classic Theories of Economic DevelopmentDocument35 pagesComparing Classic Theories of Economic DevelopmentLaura Mîndra80% (5)

- Topic 3 - Todaro, Economic Development - Ch.3 (Wiscana AP)Document4 pagesTopic 3 - Todaro, Economic Development - Ch.3 (Wiscana AP)Wiscana Chacha100% (1)

- Chapter 1-3Document10 pagesChapter 1-3GWYNETH SYBIL BATACANNo ratings yet

- Batacan - MGT109 B5 - 01Document3 pagesBatacan - MGT109 B5 - 01GWYNETH SYBIL BATACANNo ratings yet

- Batacan - MGT109 B5 - Activity 3Document3 pagesBatacan - MGT109 B5 - Activity 3GWYNETH SYBIL BATACANNo ratings yet

- Batacan - MGT109 B5 - 02Document3 pagesBatacan - MGT109 B5 - 02GWYNETH SYBIL BATACANNo ratings yet

- Peace JournalDocument7 pagesPeace JournalGWYNETH SYBIL BATACANNo ratings yet

- My Own Definition of PEACE:: 4 Pics 1 ParagraphDocument2 pagesMy Own Definition of PEACE:: 4 Pics 1 ParagraphGWYNETH SYBIL BATACANNo ratings yet

- Karate I. History/Origin of Karate A. Development B. Olympics/Sea Games C. BranchesDocument14 pagesKarate I. History/Origin of Karate A. Development B. Olympics/Sea Games C. BranchesGWYNETH SYBIL BATACANNo ratings yet

- Compare & Contrast Arguments (BATACAN)Document2 pagesCompare & Contrast Arguments (BATACAN)GWYNETH SYBIL BATACANNo ratings yet

- REFLECTIONDocument1 pageREFLECTIONGWYNETH SYBIL BATACANNo ratings yet

- Ditta Shierlly Novierra - Minicase Conch Republic Electronics, Part 2Document36 pagesDitta Shierlly Novierra - Minicase Conch Republic Electronics, Part 2Ummaya MalikNo ratings yet

- Legal Statement of Ownership FormDocument4 pagesLegal Statement of Ownership FormMy BusinessNo ratings yet

- ICICI Bank Limited CPC-Demat Account Closure FormDocument1 pageICICI Bank Limited CPC-Demat Account Closure FormAkash MishraNo ratings yet

- Datasheet - Burndy - YA4CDocument2 pagesDatasheet - Burndy - YA4CAriel MendozaNo ratings yet

- Https Uucms - Karnataka.gov - in ExamGeneral PrintExamApplicationDocument1 pageHttps Uucms - Karnataka.gov - in ExamGeneral PrintExamApplicationSagar SagarNo ratings yet

- The Effect of Geo Cultural Product Attractiveness On Marketing Performance A Conceptual FrameworkDocument6 pagesThe Effect of Geo Cultural Product Attractiveness On Marketing Performance A Conceptual FrameworkVidya HerawatiNo ratings yet

- SoftGel Capsule Part 2Document109 pagesSoftGel Capsule Part 2pharmashri53990% (1)

- Ifrs Chart of AccountDocument22 pagesIfrs Chart of AccountZidan Zee100% (1)

- Common Statistical Tests Are Linear ModelsDocument1 pageCommon Statistical Tests Are Linear ModelsLourrany BorgesNo ratings yet

- Contract Management in ProcurementDocument18 pagesContract Management in ProcurementSiampol FeepakphorNo ratings yet

- Identity Theft, Credit Reports, and You - Kalzumeus SoftwareDocument14 pagesIdentity Theft, Credit Reports, and You - Kalzumeus Softwarebjrfedor100% (1)

- 41 - 21-001 - AVK026 - Eng - v1-0 (1) - Check Valve Swing TypeDocument2 pages41 - 21-001 - AVK026 - Eng - v1-0 (1) - Check Valve Swing TypeBernard Bonnin CervantesNo ratings yet

- Nota k3 LodgingDocument55 pagesNota k3 LodgingsyafawatisamanNo ratings yet

- SAILDocument17 pagesSAILnareshNo ratings yet

- Plant for Pakistan PT-10 FormDocument2 pagesPlant for Pakistan PT-10 FormAqeel AhmedNo ratings yet

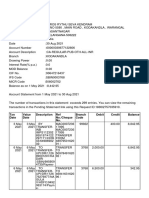

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument40 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balance184H0 Yellu Anusha VCENo ratings yet

- Simple Interest and Compound Interest Basic LevelDocument10 pagesSimple Interest and Compound Interest Basic LevelSubhash HandaNo ratings yet

- Approved Supplier ListDocument12 pagesApproved Supplier ListgfqatrNo ratings yet

- Animal Census Rajasthan 2019 DataDocument2 pagesAnimal Census Rajasthan 2019 DataPAHAL PYARENo ratings yet

- Salaar FlourDocument71 pagesSalaar FlourZubair TradersNo ratings yet

- Confirmation 2 PDFDocument2 pagesConfirmation 2 PDFENAD TBISHATNo ratings yet

- Case Study 1Document5 pagesCase Study 1Katherine Barreto0% (1)

- 28x VenmoDocument1 page28x Venmorckmvp6c8qNo ratings yet

- Alpha Engineers, AlwarDocument36 pagesAlpha Engineers, AlwarHarsh KachhawaNo ratings yet

- 30-April-2021 Weekly UpdateDocument11 pages30-April-2021 Weekly UpdateShamraiz KhanNo ratings yet

- 02 Traffic Data Collection and AADT ReviewDocument38 pages02 Traffic Data Collection and AADT ReviewNic Pangan VinuyaNo ratings yet

- 382 1458 1 PBDocument11 pages382 1458 1 PBDaniela DanaNo ratings yet

- Up1029 A0 Copyshop - CompressedDocument1 pageUp1029 A0 Copyshop - CompressedPaula MoraNo ratings yet

- Gantrex Pad Mk6Document4 pagesGantrex Pad Mk6reza nasiriNo ratings yet

- Economic Resources and Basic QuestionsDocument2 pagesEconomic Resources and Basic QuestionsGine Bert Fariñas PalabricaNo ratings yet