You might also like

- Social Security SchemesDocument26 pagesSocial Security SchemesharishNo ratings yet

- GSISDocument11 pagesGSISClauds GadzzNo ratings yet

- The Government Service Insurance System Act of 1997 (REPORT)Document15 pagesThe Government Service Insurance System Act of 1997 (REPORT)Johnson LimNo ratings yet

- GSISDocument56 pagesGSISJonna Maye Loras Canindo100% (6)

- Principles of Insurance PDFDocument72 pagesPrinciples of Insurance PDFshahzebNo ratings yet

- Social Security System 2017Document35 pagesSocial Security System 2017NJ Geerts100% (1)

- Provident Fund ActDocument14 pagesProvident Fund ActAkanksha Dubey0% (1)

- GSISDocument56 pagesGSISsantasantita100% (1)

- GSIS ReportDocument177 pagesGSIS ReportAbigail PasionNo ratings yet

- Case Brief InsuDocument3 pagesCase Brief InsuMikes Flores100% (1)

- The GSIS and RA 8291Document6 pagesThe GSIS and RA 8291Efeiluj CuencaNo ratings yet

- R.A. 8291Document4 pagesR.A. 8291Nenita OcarizaNo ratings yet

- Irr Gsis LawDocument46 pagesIrr Gsis LawMa Geobelyn LopezNo ratings yet

- Social Security LawDocument11 pagesSocial Security LawmarkNo ratings yet

- Presentation For GSISDocument12 pagesPresentation For GSISDkNarcisoNo ratings yet

- Government Service Insurance System (GSIS)Document11 pagesGovernment Service Insurance System (GSIS)BethylGo0% (1)

- Gsis LawDocument26 pagesGsis LawMaia DelimaNo ratings yet

- Aditya Birla CapitalDocument42 pagesAditya Birla CapitalKush100% (4)

- Ra 8282 - SSSDocument112 pagesRa 8282 - SSSNelia Mae S. Villena100% (1)

- Comparative Matrix of Social Legislation in The PhilippinesDocument14 pagesComparative Matrix of Social Legislation in The PhilippinesHowie Malik100% (2)

- Coop Laws and Social Legislation: Government Service Insurance SystemDocument24 pagesCoop Laws and Social Legislation: Government Service Insurance Systemyannie11No ratings yet

- An Orientation of Gsis Membership, Benefits, Programs and LoansDocument31 pagesAn Orientation of Gsis Membership, Benefits, Programs and LoansFrancis Ysabella BalagtasNo ratings yet

- Gsis - Ra 8291Document33 pagesGsis - Ra 8291RoySantosMoralesNo ratings yet

- Irr Gsis LawDocument45 pagesIrr Gsis LawManila LoststudentNo ratings yet

- Topic 6.1 Government Service Insurance System: CoverageDocument3 pagesTopic 6.1 Government Service Insurance System: CoverageJohn Lesther PabiloniaNo ratings yet

- Retirement BrochureDocument40 pagesRetirement BrochureSweetHiezel SaplanNo ratings yet

- NLM ReportDocument58 pagesNLM ReportBon QuiapoNo ratings yet

- GSISDocument56 pagesGSISGilbert Gabrillo JoyosaNo ratings yet

- GSIS AccomplishmentDocument16 pagesGSIS AccomplishmentGerrysaudi Dzme-epNo ratings yet

- Employee Benefits and Social Insurance: Ariel M. LorenzoDocument45 pagesEmployee Benefits and Social Insurance: Ariel M. LorenzoJaime DaliuagNo ratings yet

- University of Santo Tomas Faculty of Civil Law: Academic Year 2020-2021, Term 1Document46 pagesUniversity of Santo Tomas Faculty of Civil Law: Academic Year 2020-2021, Term 1Miguel Joshua Gange AguirreNo ratings yet

- LoansDocument18 pagesLoansKristel Jane Donaire BihagNo ratings yet

- University of Santo Tomas Faculty of Civil Law: Academic Year 2020-2021, Term 1Document42 pagesUniversity of Santo Tomas Faculty of Civil Law: Academic Year 2020-2021, Term 1Miguel Joshua Gange AguirreNo ratings yet

- Lecture 3 - The Employee's State Insurance Act, 1948Document8 pagesLecture 3 - The Employee's State Insurance Act, 1948rishapNo ratings yet

- Who Are Subject To Compulsory Coverage Under The Government Service Insurance System?Document12 pagesWho Are Subject To Compulsory Coverage Under The Government Service Insurance System?nimfasfontaineNo ratings yet

- Contributions/ Fees 1. EE's Contribution: Members Who Can AffordDocument2 pagesContributions/ Fees 1. EE's Contribution: Members Who Can AffordblimjucoNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument17 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledRen MagallonNo ratings yet

- GSISDocument61 pagesGSISJelly BeanNo ratings yet

- Social Legislation PrinciplesDocument4 pagesSocial Legislation PrinciplesAppleSamsonNo ratings yet

- Chapters 11 13Document68 pagesChapters 11 13Shanley Duenn UdtohanNo ratings yet

- Definition of Terms IRR Gsis Board Employer: CD Technologies Asia, Inc. © 2019Document42 pagesDefinition of Terms IRR Gsis Board Employer: CD Technologies Asia, Inc. © 2019shhhgNo ratings yet

- Employees' State Insurance Act, 1948Document6 pagesEmployees' State Insurance Act, 1948Ronan GomezNo ratings yet

- Sss CoverageDocument2 pagesSss CoverageKirt CatindigNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument23 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledJayMichaelAquinoMarquezNo ratings yet

- R.A. No. 1161 (The Social Security Act of 1997)Document7 pagesR.A. No. 1161 (The Social Security Act of 1997)nicole coNo ratings yet

- LIC Group Insurance SchemeDocument4 pagesLIC Group Insurance SchemeSavi SharmaNo ratings yet

- Explanation BfiDocument7 pagesExplanation BfidespianyayahanNo ratings yet

- Law 2Document23 pagesLaw 2Kamlesh TripathiNo ratings yet

- GSIS BenefitsDocument17 pagesGSIS BenefitsRandy MusaNo ratings yet

- Social Welfare LegislationDocument12 pagesSocial Welfare LegislationMarianita CenizaNo ratings yet

- Group Saving Linked Insurance SchemeDocument14 pagesGroup Saving Linked Insurance SchemeSam DavidNo ratings yet

- Brochure GFAL ActiveDocument40 pagesBrochure GFAL ActiveJudson PastranoNo ratings yet

- Employees Compensation ProgramDocument13 pagesEmployees Compensation Programnorma bayoneta100% (1)

- Social Welfare Legislation LectureDocument16 pagesSocial Welfare Legislation LectureAllyza RamirezNo ratings yet

- Declaration of Policy.: Power and DutiesDocument4 pagesDeclaration of Policy.: Power and DutiesMidzmar KulaniNo ratings yet

- Social Security in IndiaDocument49 pagesSocial Security in IndiaKaran Gupta100% (1)

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument21 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledRhenfacel ManlegroNo ratings yet

- Laurie Carr L. LandichoDocument11 pagesLaurie Carr L. LandichoLaurie Carr LandichoNo ratings yet

- 4.1 Revised IRR of (GSIS) R.A. 8291Document43 pages4.1 Revised IRR of (GSIS) R.A. 8291Leonel DomingoNo ratings yet

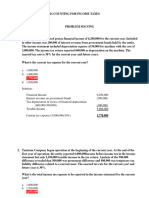

- Solution Tax467 - Jul 2017Document7 pagesSolution Tax467 - Jul 2017Putri Nurin Hasnida HassanNo ratings yet

- AR Educare Advantage Insurance Plan 5 May 2014Document6 pagesAR Educare Advantage Insurance Plan 5 May 2014ÌmřańNo ratings yet

- ReportDocument7 pagesReporttanjim_47No ratings yet

- GROSS INCOME and DEDUCTIONSDocument10 pagesGROSS INCOME and DEDUCTIONSMHERITZ LYN LIM MAYOLANo ratings yet

- Unit 4 InsuranceDocument4 pagesUnit 4 InsuranceKanishkaNo ratings yet

- Learner Guide 242597Document28 pagesLearner Guide 242597palmalynchwatersNo ratings yet

- Online Insurance Claim Management System: AbstractDocument6 pagesOnline Insurance Claim Management System: AbstractPradeep VishwakarmaNo ratings yet

- Mii Pceia Ceilli ExaminationDocument8 pagesMii Pceia Ceilli Examinationgopalathevar sammuhomNo ratings yet

- Shriram Life Insurance Company (Wiki)Document2 pagesShriram Life Insurance Company (Wiki)KaranPatil50% (2)

- Biagtan CaseDocument40 pagesBiagtan CaseNikclausse MarquezNo ratings yet

- Insunews: Weekly E-NewsletterDocument30 pagesInsunews: Weekly E-NewsletterHimanshu PantNo ratings yet

- TG1628 Kotak Life InsuranceDocument2 pagesTG1628 Kotak Life InsuranceAnandKumarPNo ratings yet

- Gross EstateDocument11 pagesGross EstatejungoosNo ratings yet

- Predetermination of Benefits-30122023Document2 pagesPredetermination of Benefits-30122023jgodlontonNo ratings yet

- Solution - Accounting For Income TaxesDocument12 pagesSolution - Accounting For Income TaxesKlarissemay MontallanaNo ratings yet

- Dr. Usha N. Patil MRP SummaryDocument4 pagesDr. Usha N. Patil MRP SummaryShree GuruNo ratings yet

- American Continental Insurance CompanyDocument8 pagesAmerican Continental Insurance CompanyMathias MartinezNo ratings yet

- BIR Form 2551M Monthly Percentage TaxDocument3 pagesBIR Form 2551M Monthly Percentage TaxBaby BoyNo ratings yet

- Nyaradzo Group - Our TeamDocument2 pagesNyaradzo Group - Our TeamTony Peterz Kurewa100% (1)

- 4 - GSIS V City Treasurer of The City of Manila, G.R. No. 186242Document8 pages4 - GSIS V City Treasurer of The City of Manila, G.R. No. 186242KhiarraNo ratings yet

- NO. Chapter Name Page No.: Content of TableDocument58 pagesNO. Chapter Name Page No.: Content of TableSuraj JadhavNo ratings yet

- Ranjan Kumar Jaiswal Kotak Mahindra BankDocument6 pagesRanjan Kumar Jaiswal Kotak Mahindra BankpradeepkumarsinghkhoNo ratings yet

- Unit 2Document21 pagesUnit 2nikita2802No ratings yet

- Calanoc vs. Court of AppealsDocument4 pagesCalanoc vs. Court of AppealsAaron CarinoNo ratings yet

- Curriculum Vitae: Career ObjectivesDocument5 pagesCurriculum Vitae: Career ObjectivesAlfie Group of InvestmentNo ratings yet

- Non Bank Financial Institutions (Fis)Document25 pagesNon Bank Financial Institutions (Fis)Md. Saiful IslamNo ratings yet

- INCOME TAXATION ExclusionsDocument2 pagesINCOME TAXATION ExclusionsPepe FrogNo ratings yet