You might also like

- Chapter 2 - Determinants of Interest RatesDocument3 pagesChapter 2 - Determinants of Interest RatesJean Stephany100% (1)

- ch#5 of CFDocument2 pagesch#5 of CFAzeem KhalidNo ratings yet

- DerivativesDocument53 pagesDerivativesnikitsharmaNo ratings yet

- Producer and Consumer SurplusDocument28 pagesProducer and Consumer SurplusSyedNo ratings yet

- FICM ObsaaDocument105 pagesFICM Obsaasamuel kebede100% (1)

- Caps Floors CollarsDocument3 pagesCaps Floors CollarsNaga Mani MeruguNo ratings yet

- How CAPM Helps Calculate Investment Risk and Expected ReturnsDocument7 pagesHow CAPM Helps Calculate Investment Risk and Expected ReturnsVaishali ShuklaNo ratings yet

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- PROJECT PLANNING WITH CPM/PERTDocument49 pagesPROJECT PLANNING WITH CPM/PERTRheanneNo ratings yet

- CH 1Document55 pagesCH 1kamkdgNo ratings yet

- CH 01Document12 pagesCH 01xyzNo ratings yet

- Topic 2 ExercisesDocument6 pagesTopic 2 ExercisesRaniel Pamatmat0% (1)

- Cash Coversion CYcleDocument29 pagesCash Coversion CYcleZohaib HassanNo ratings yet

- EBIT-EPS analysis for financing plan decisionsDocument6 pagesEBIT-EPS analysis for financing plan decisionsSthephany GranadosNo ratings yet

- Types of Dividends Overview of DividendsDocument5 pagesTypes of Dividends Overview of DividendsEllieNo ratings yet

- 8 Responsibility AccountingDocument8 pages8 Responsibility AccountingXyril MañagoNo ratings yet

- DerivativesDocument125 pagesDerivativesLouella Liparanon100% (1)

- Financial Accounting: Weygandt KimmelDocument47 pagesFinancial Accounting: Weygandt KimmelTham NguyenNo ratings yet

- Tutorial 1Document2 pagesTutorial 1musicslave96No ratings yet

- What Is Management Accounting?Document3 pagesWhat Is Management Accounting?Mia Casas100% (1)

- FIMA 40023 Security Analysis FinalsDocument14 pagesFIMA 40023 Security Analysis FinalsPrincess ErickaNo ratings yet

- EMGT102 - Online Activity No. 5inventory Control ModelDocument4 pagesEMGT102 - Online Activity No. 5inventory Control Modelmache dumadNo ratings yet

- ACCOUNTING FOR DERIVATIVES (Part 1Document40 pagesACCOUNTING FOR DERIVATIVES (Part 1Ericka AlimNo ratings yet

- Spotifire Ayala-Land Final-PaperDocument74 pagesSpotifire Ayala-Land Final-PaperTrace AsinasNo ratings yet

- Ifrs 3Document4 pagesIfrs 3Ken ZafraNo ratings yet

- Business Finance-Semi-Final ExamDocument3 pagesBusiness Finance-Semi-Final ExamHLeigh Nietes-Gabutan100% (1)

- Tutorial 1: 1. What Is The Basic Functions of Financial Markets?Document6 pagesTutorial 1: 1. What Is The Basic Functions of Financial Markets?Ramsha ShafeelNo ratings yet

- Callable Bonds ExplainedDocument33 pagesCallable Bonds ExplainedtwinklenoorNo ratings yet

- Introduction To Business Taxes: September 4, 2020Document20 pagesIntroduction To Business Taxes: September 4, 2020Bancas YvonNo ratings yet

- CASEDocument18 pagesCASEJay SabioNo ratings yet

- Powerpoint Slides Prepared by Robert F. Brooker, Ph.D. Opyright 2007 by Oxford University Press, IncDocument40 pagesPowerpoint Slides Prepared by Robert F. Brooker, Ph.D. Opyright 2007 by Oxford University Press, Incishikadhamija24No ratings yet

- Advance Chapter 1Document16 pagesAdvance Chapter 1abel habtamuNo ratings yet

- Corn Products Refining Company v. Commissioner of Internal Revenue, 215 F.2d 513, 2d Cir. (1954)Document7 pagesCorn Products Refining Company v. Commissioner of Internal Revenue, 215 F.2d 513, 2d Cir. (1954)Scribd Government DocsNo ratings yet

- Chapter 3 Valuation and Cost of CapitalDocument92 pagesChapter 3 Valuation and Cost of Capitalyemisrach fikiruNo ratings yet

- OLIGOPSONYDocument3 pagesOLIGOPSONYBernard Okpe100% (1)

- CfasDocument42 pagesCfasCleofe Mae Piñero AseñasNo ratings yet

- LEC 5.2 Standard Costing and Variance AnalysisDocument32 pagesLEC 5.2 Standard Costing and Variance AnalysisKelvin Culajará100% (1)

- Inventory MGMT ComprehensiveDocument4 pagesInventory MGMT ComprehensivebigbaekNo ratings yet

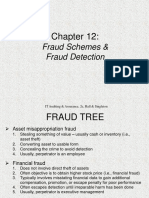

- Ch12 Fraud Scheme DetectionDocument18 pagesCh12 Fraud Scheme DetectionPanda BoarsNo ratings yet

- Exception To The Lower of Cost and Net Realizable Value Rule in IAS 2-InventoriesDocument3 pagesException To The Lower of Cost and Net Realizable Value Rule in IAS 2-InventoriesgdegirolamoNo ratings yet

- Tax SemisDocument50 pagesTax SemisTeam MindanaoNo ratings yet

- Chapter08 PDFDocument22 pagesChapter08 PDFBabuM ACC FIN ECONo ratings yet

- Anne in InvestmentDocument12 pagesAnne in InvestmentLigwina DNo ratings yet

- Intro To Cost Accounting ReviewerDocument2 pagesIntro To Cost Accounting ReviewerJosephine YenNo ratings yet

- ACCCOB3Document87 pagesACCCOB3Lexy SungaNo ratings yet

- Money Markets ReviewerDocument4 pagesMoney Markets ReviewerHazel Jane EsclamadaNo ratings yet

- 07 Multinational Financial ManagementDocument61 pages07 Multinational Financial Managementeunjijung100% (1)

- MiniscribeDocument14 pagesMiniscribeImadNo ratings yet

- Chapter 3-4 QuestionsDocument5 pagesChapter 3-4 QuestionsMya B. Walker0% (1)

- Bab Vii BalandcorcardDocument17 pagesBab Vii BalandcorcardCela Lutfiana100% (1)

- Valuation and Rate of ReturnsDocument42 pagesValuation and Rate of ReturnsMadCube gamingNo ratings yet

- Futures and ForwardsDocument39 pagesFutures and Forwardskamdica100% (1)

- BUSI 353 S18 Assignment 4 SOLUTIONDocument2 pagesBUSI 353 S18 Assignment 4 SOLUTIONTanNo ratings yet

- Asset Recognition and Operating Assets: Fourth EditionDocument55 pagesAsset Recognition and Operating Assets: Fourth EditionAyush JainNo ratings yet

- Unit III TOPIC: - Forward and Futures Contracts: Meaning, Difference Between Forward and FuturesDocument12 pagesUnit III TOPIC: - Forward and Futures Contracts: Meaning, Difference Between Forward and FuturescammyNo ratings yet

- Chapter 15Document20 pagesChapter 15sdfklmjsdlklskfjdNo ratings yet

- BUSI 353 S18 Assignment 5 SOLUTIONDocument5 pagesBUSI 353 S18 Assignment 5 SOLUTIONTan100% (2)

- Prequalifying Exam Level 2 3 Set B FSUU AccountingDocument9 pagesPrequalifying Exam Level 2 3 Set B FSUU AccountingRobert CastilloNo ratings yet

- Asian Economic Integration Report 2021: Making Digital Platforms Work for Asia and the PacificFrom EverandAsian Economic Integration Report 2021: Making Digital Platforms Work for Asia and the PacificNo ratings yet

- Perancangan Model Data Warehouse Dan Perangkat Analitik Untuk Memaksimalkan Proses Pemasaran Hotel: Studi Kasus Pada Hotel AbcDocument10 pagesPerancangan Model Data Warehouse Dan Perangkat Analitik Untuk Memaksimalkan Proses Pemasaran Hotel: Studi Kasus Pada Hotel Abcfaisal zafryNo ratings yet

- Charles R. Wood Theater Capital Campaign PlanDocument25 pagesCharles R. Wood Theater Capital Campaign PlanErin CoonNo ratings yet

- A Annual Consumption 0 Cost of Placing Order C Carrying Cost Per UnitDocument8 pagesA Annual Consumption 0 Cost of Placing Order C Carrying Cost Per UnitJaimin PatelNo ratings yet

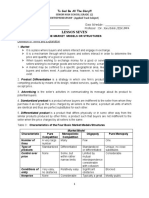

- SHS LESSON 7 Market Models or StructuresDocument12 pagesSHS LESSON 7 Market Models or StructuresPaul AnteNo ratings yet

- Vision and MissionDocument3 pagesVision and MissionPaulo Arwin BaduriaNo ratings yet

- Bus 2101 - Chapter 2Document24 pagesBus 2101 - Chapter 2HarshaBorresAlamoNo ratings yet

- HP Supply Chain ManagmentDocument25 pagesHP Supply Chain ManagmentEr Pradip Patel100% (1)

- Manufacturing Process Audit: Example ReportDocument25 pagesManufacturing Process Audit: Example ReportJawad rahmanaccaNo ratings yet

- Principle of ValuationDocument76 pagesPrinciple of Valuationnavneet PatilNo ratings yet

- Citi BankDocument40 pagesCiti BankZeeshan Mobeen100% (1)

- Syllabus KM & MonpoDocument2 pagesSyllabus KM & MonpoGaneshNo ratings yet

- Atlantic Computer A Bundle of Pricing OptionsDocument2 pagesAtlantic Computer A Bundle of Pricing OptionsShipra100% (1)

- Quality Control ProcessDocument1 pageQuality Control ProcessHuseyinNo ratings yet

- Atb Cell ManualDocument63 pagesAtb Cell Manualramyarayee100% (1)

- Evaluation of Investor Awareness On Techniques UseDocument12 pagesEvaluation of Investor Awareness On Techniques UseRonat JainNo ratings yet

- 1 D 1 DF 41 D 6 F 8 C 8 G 5Document5 pages1 D 1 DF 41 D 6 F 8 C 8 G 5Kia PottsNo ratings yet

- Ebook Cornerstones of Financial Accounting 4Th Edition Rich Test Bank Full Chapter PDFDocument55 pagesEbook Cornerstones of Financial Accounting 4Th Edition Rich Test Bank Full Chapter PDFfreyahypatias7j100% (9)

- Bartronics 2013 OCDocument189 pagesBartronics 2013 OCNaz BuntingNo ratings yet

- Corporate GovernanceDocument30 pagesCorporate GovernanceMehdi BouaniaNo ratings yet

- Price Water House Coopers (PWC) ProfileDocument13 pagesPrice Water House Coopers (PWC) ProfilebharatNo ratings yet

- BodyDocument83 pagesBodyarunantony100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument7 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceGagan DhingraNo ratings yet

- Shopper Marketing StrategyDocument22 pagesShopper Marketing StrategyMuhammad Faiq SiddiquiNo ratings yet

- Duties of Directors to Ensure Good GovernanceDocument26 pagesDuties of Directors to Ensure Good GovernanceBishop PantaNo ratings yet

- An Assessment of Customer Response To El PDFDocument17 pagesAn Assessment of Customer Response To El PDFaleneNo ratings yet

- Manage savings and track transactionsDocument1 pageManage savings and track transactionsbc180204979 ALI FAROOQ100% (3)

- Unit - 3: Service MarketingDocument19 pagesUnit - 3: Service MarketingcharangowdaNo ratings yet

- Currency ConversionDocument6 pagesCurrency Conversiontatyanna weaverNo ratings yet

- Department of Agrarian Reform: "Gil" de Los ReyesDocument10 pagesDepartment of Agrarian Reform: "Gil" de Los ReyesGNCDWNo ratings yet

- 11 Master Data Management Roadmap TemplateDocument20 pages11 Master Data Management Roadmap TemplateMARIA SELES TELES SOUSANo ratings yet