You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Macroeconomics 6th Edition Williamson Solutions ManualDocument14 pagesMacroeconomics 6th Edition Williamson Solutions Manualregattabump0dt100% (30)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chapter 13-Investments in Noncurrent Operating Assets-Utilization & Re-TirementDocument26 pagesChapter 13-Investments in Noncurrent Operating Assets-Utilization & Re-Tirement수지No ratings yet

- Profit PlanningDocument86 pagesProfit PlanningSederiku KabaruzaNo ratings yet

- "How Well Am I Doing?" Financial Statement AnalysisDocument61 pages"How Well Am I Doing?" Financial Statement AnalysisSederiku KabaruzaNo ratings yet

- FIFO MethodDocument40 pagesFIFO MethodSederiku KabaruzaNo ratings yet

- Relevant Costs For Decision MakingDocument69 pagesRelevant Costs For Decision MakingSederiku KabaruzaNo ratings yet

- Decentralization and Segment ReportingDocument62 pagesDecentralization and Segment ReportingSederiku KabaruzaNo ratings yet

- Systems Design-Process CostingDocument58 pagesSystems Design-Process CostingSederiku KabaruzaNo ratings yet

- Activity Based Costing-A Tool To Aid Decision MakingDocument54 pagesActivity Based Costing-A Tool To Aid Decision MakingSederiku KabaruzaNo ratings yet

- MS MakulitDocument3 pagesMS MakulitSederiku KabaruzaNo ratings yet

- Variable Costing-A Tool For ManagementDocument32 pagesVariable Costing-A Tool For ManagementSederiku KabaruzaNo ratings yet

- Introduction To Entrepreneurship: Module - 1Document14 pagesIntroduction To Entrepreneurship: Module - 1Sederiku KabaruzaNo ratings yet

- Abstract Research ExampleDocument1 pageAbstract Research ExampleSederiku Kabaruza50% (2)

- History of The Meat IndustryDocument33 pagesHistory of The Meat IndustrySederiku KabaruzaNo ratings yet

- Research Tally SheetDocument85 pagesResearch Tally SheetSederiku KabaruzaNo ratings yet

- Answer KeyDocument8 pagesAnswer KeySederiku KabaruzaNo ratings yet

- The Importance of Ethics in BusinessDocument27 pagesThe Importance of Ethics in BusinessSederiku KabaruzaNo ratings yet

- Psychoanalysis (Sigmund Frued)Document3 pagesPsychoanalysis (Sigmund Frued)Sederiku KabaruzaNo ratings yet

- Law Society CONVEYANCING PRACTICE SOLICITORS UNDERTAKINGDocument1 pageLaw Society CONVEYANCING PRACTICE SOLICITORS UNDERTAKINGRian TamNo ratings yet

- Roles&Responsibilities of ULB Functionaries1Document130 pagesRoles&Responsibilities of ULB Functionaries1Raghu RamNo ratings yet

- MSL 19 0003Document1 pageMSL 19 0003Sovanna HangNo ratings yet

- A Proposed Mactan Amusement Park: Analee Borres QuiapoDocument1 pageA Proposed Mactan Amusement Park: Analee Borres Quiapofppalawan plansNo ratings yet

- An Experimental Investigation in Paver Blocks by Replacing Sand With Manufacturing Sand and Its Strength ComparisonDocument13 pagesAn Experimental Investigation in Paver Blocks by Replacing Sand With Manufacturing Sand and Its Strength ComparisonPratik WANKHEDENo ratings yet

- BillDocument1 pageBillLan NhiNo ratings yet

- Blinder-Is There A Core of Practical Macro We Should BelieveDocument7 pagesBlinder-Is There A Core of Practical Macro We Should BelieveSantiagoNo ratings yet

- Econ 122 Week 1-9 by DwexDocument19 pagesEcon 122 Week 1-9 by Dwexjohn100% (3)

- Association For Survey - v2Document4 pagesAssociation For Survey - v2sanjay chandwaniNo ratings yet

- Night AuditDocument16 pagesNight AuditKumarasamy Vijayarajan100% (1)

- Trade Name Reservation ReceiptDocument1 pageTrade Name Reservation ReceiptHORUS TYPING & P.R.O SERVICESNo ratings yet

- CrawfordQC 1 21 2020Document90 pagesCrawfordQC 1 21 2020dchester smithNo ratings yet

- Quality Control Management AssignmentDocument8 pagesQuality Control Management AssignmentKimmy LyonsNo ratings yet

- Corgi Queen PatternDocument4 pagesCorgi Queen PatternTasheenaNo ratings yet

- Acct Statement - XX6782 - 23012024Document5 pagesAcct Statement - XX6782 - 23012024Thejesh tejuNo ratings yet

- Tuesdi®: NO. June PriceDocument8 pagesTuesdi®: NO. June Pricefilip KOpeckyNo ratings yet

- Far Notes - Accounting Cycle of Merchandising BusinessDocument15 pagesFar Notes - Accounting Cycle of Merchandising BusinessVan MateoNo ratings yet

- Office Address Ro BangaloreDocument3 pagesOffice Address Ro Bangaloresandeep naikNo ratings yet

- Capital Budgeting Notes (MBA FA - 2023)Document10 pagesCapital Budgeting Notes (MBA FA - 2023)kavyaNo ratings yet

- FPB 22.03 - Steam Turbines and Axial Turbo Expanders Observation of Hexavalent Chromium On Equipment During OutagesDocument5 pagesFPB 22.03 - Steam Turbines and Axial Turbo Expanders Observation of Hexavalent Chromium On Equipment During Outageswaqar ahmadNo ratings yet

- 2001 Econ. Paper 1 (Original)Document7 pages2001 Econ. Paper 1 (Original)peter wongNo ratings yet

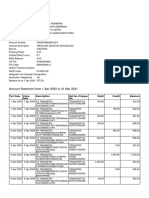

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNo ratings yet

- IFYEC002 Economics (Автосохраненный)Document11 pagesIFYEC002 Economics (Автосохраненный)bunyod radjabovNo ratings yet

- Final Corporate StrategyDocument1 pageFinal Corporate Strategyqikangdong7No ratings yet

- Attachment-F5 Transfer Line Refacroty Repir Rev2. U340-R75822 (MHI)Document27 pagesAttachment-F5 Transfer Line Refacroty Repir Rev2. U340-R75822 (MHI)JESUSNo ratings yet

- ENT300 BUSINESS PLAN Latest - Doc (Ref)Document61 pagesENT300 BUSINESS PLAN Latest - Doc (Ref)Nor HakimNo ratings yet

- DOC-20240405-WA0001.Document7 pagesDOC-20240405-WA0001.Swetha PvNo ratings yet

- Permanent Metal - Data - Sheet - AFP 1 209B New PDFDocument1 pagePermanent Metal - Data - Sheet - AFP 1 209B New PDFcham_900No ratings yet