You might also like

- Jay Abraham - Strategy Case StudiesDocument16 pagesJay Abraham - Strategy Case StudiesShashank KesarwaniNo ratings yet

- CPIM 2022 Part 1 Module 4Document112 pagesCPIM 2022 Part 1 Module 4Danilo Freitas100% (2)

- Chap.13 Guerrero Job Order CostingDocument40 pagesChap.13 Guerrero Job Order CostingGeoff MacarateNo ratings yet

- 2nd Evaluation Exam Key FINALDocument7 pages2nd Evaluation Exam Key FINALChristian GeronimoNo ratings yet

- Operations Management Karjewski RitzmanDocument1,516 pagesOperations Management Karjewski RitzmanAbdul Mateen100% (1)

- Economics of Plant Design (Report)Document10 pagesEconomics of Plant Design (Report)Hamizah Mieza100% (1)

- Activity Based CostingDocument30 pagesActivity Based Costinghardik1302No ratings yet

- The Importance of Ethics in BusinessDocument27 pagesThe Importance of Ethics in BusinessSederiku KabaruzaNo ratings yet

- AccountsDocument478 pagesAccountsAbhishek Ladha100% (1)

- Process Costing ModuleDocument6 pagesProcess Costing ModuleClaire BarbaNo ratings yet

- Standard CostingDocument65 pagesStandard CostingAmit KumarNo ratings yet

- Abstract Research ExampleDocument1 pageAbstract Research ExampleSederiku Kabaruza50% (2)

- Hybrid CostingDocument26 pagesHybrid CostingnadaNo ratings yet

- 610 Midterm 3 A PracticeDocument12 pages610 Midterm 3 A PracticeSummerNo ratings yet

- Cost Reduction in A Manufacturing Business - BEDocument3 pagesCost Reduction in A Manufacturing Business - BEsonali sonalNo ratings yet

- 1617 2ndS 3rde JonaldBDocument11 pages1617 2ndS 3rde JonaldBAlyssa Andrea SabinoNo ratings yet

- 2 Process Costing w2Document17 pages2 Process Costing w2Angel YungNo ratings yet

- Agenda: AF3112 Management Accounting 2Document17 pagesAgenda: AF3112 Management Accounting 2RoseNo ratings yet

- Chap18 - DNGNDocument58 pagesChap18 - DNGNĐàm Ngọc Giang NamNo ratings yet

- Desain Sistem: Perhitungan Biaya Berdasarkan Pesanan: (Job Order Costing)Document53 pagesDesain Sistem: Perhitungan Biaya Berdasarkan Pesanan: (Job Order Costing)AriniNo ratings yet

- Job CostDocument20 pagesJob CostPreetika AgarwalNo ratings yet

- Product Costing How To Calculate The Cost of A Product or A Service?Document13 pagesProduct Costing How To Calculate The Cost of A Product or A Service?FAEETNo ratings yet

- 4 Costing SystemsDocument38 pages4 Costing Systemsx6xhr6gk2mNo ratings yet

- Management Accounting Chapter 5&6Document84 pagesManagement Accounting Chapter 5&6yimerNo ratings yet

- Chapter 6 Process CostingDocument76 pagesChapter 6 Process Costingumar afzalNo ratings yet

- SCM L05 ProcessCostingDocument38 pagesSCM L05 ProcessCostinghorace000715No ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinNo ratings yet

- Systems Design: Process Costing: Chapter FourDocument53 pagesSystems Design: Process Costing: Chapter FoursanosyNo ratings yet

- ACCY918 T3 2023 Wk3 Process Costing Lecture NoteDocument82 pagesACCY918 T3 2023 Wk3 Process Costing Lecture NoteNIRAJ SharmaNo ratings yet

- Systems Design: Process Costing: Chapter FourDocument73 pagesSystems Design: Process Costing: Chapter FourBS StudioNo ratings yet

- Review Chapter 1-2-4-18Document55 pagesReview Chapter 1-2-4-18hoangmyduyennguyen2004No ratings yet

- Chap 004Document15 pagesChap 004Ahmad Restu FauziNo ratings yet

- Chap004 7e EditedDocument47 pagesChap004 7e EditedfarahNo ratings yet

- Job-Order Costing: Chapter ThreeDocument68 pagesJob-Order Costing: Chapter ThreeMd Hasibul Karim 1811766630No ratings yet

- ACT 202 Chapter 3 - UpdatedDocument53 pagesACT 202 Chapter 3 - UpdatedAminaMatinNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument17 pagesProcess Costing and Hybrid Product-Costing SystemsWailNo ratings yet

- AF3112 Management Accounting 2: Process CostingDocument66 pagesAF3112 Management Accounting 2: Process Costing行歌No ratings yet

- Assignment of Process CostingDocument1 pageAssignment of Process CostingAliNo ratings yet

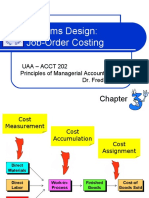

- Systems Design: Job-Order Costing: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeDocument22 pagesSystems Design: Job-Order Costing: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeOrnica BalesNo ratings yet

- Mind Map Process CostingDocument1 pageMind Map Process CostingAndhika Bella PrawitasariNo ratings yet

- Process Costing: A Cost Accumulation MethodDocument9 pagesProcess Costing: A Cost Accumulation MethodDahlia BloomsNo ratings yet

- Job CostingDocument26 pagesJob CostingpriyankaNo ratings yet

- Cost Concepts, Terms and ClassificationsDocument18 pagesCost Concepts, Terms and ClassificationsShennie BeldaNo ratings yet

- Job-Order Costing: Chapter ThreeDocument76 pagesJob-Order Costing: Chapter Threejaz hoodNo ratings yet

- Act 202 Chapter 3Document68 pagesAct 202 Chapter 3Shaon KhanNo ratings yet

- Chapters 2 & 3.: Job-Order CostingDocument83 pagesChapters 2 & 3.: Job-Order CostingsaraNo ratings yet

- Activity Based Costing:: A Tool To Aid Decision MakingDocument36 pagesActivity Based Costing:: A Tool To Aid Decision MakingParikshit SethiNo ratings yet

- Systems Design: Job-Order Costing: Chapter ThreeDocument66 pagesSystems Design: Job-Order Costing: Chapter ThreeSHAF KHANNo ratings yet

- Chapter No.04 - Process Costing and Hybrid Product-Costing SystemsDocument39 pagesChapter No.04 - Process Costing and Hybrid Product-Costing SystemsWali NoorzadNo ratings yet

- Topic 6 - Process CostingDocument7 pagesTopic 6 - Process CostingMuhammad Alif100% (1)

- Job Order Costing - Hand OutDocument6 pagesJob Order Costing - Hand OutKorinth BalaoNo ratings yet

- CH 04Document30 pagesCH 04Giang Nguyễn TràNo ratings yet

- تلخيص شابتر 8 محاسبةDocument1 pageتلخيص شابتر 8 محاسبةMariam SalahNo ratings yet

- Manac Knowledge Session - Mid TermDocument33 pagesManac Knowledge Session - Mid TermDebaloy DeyNo ratings yet

- CHPT 03 HODocument22 pagesCHPT 03 HOKerby Gail RulonaNo ratings yet

- Cost Accumulation For Job and Batch Production Chap003-3Document29 pagesCost Accumulation For Job and Batch Production Chap003-3Anirudh JoshiNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- 4 Cost Management System IMPROVED - by FSCDocument31 pages4 Cost Management System IMPROVED - by FSCAryan jhaNo ratings yet

- Module 6A Process Costing WeightedDocument3 pagesModule 6A Process Costing WeightedSky SoronoiNo ratings yet

- Hilton 11e Chap004 PPT-STUDocument42 pagesHilton 11e Chap004 PPT-STULạnh LùngNo ratings yet

- Chapter 5 - Job Order CostingDocument36 pagesChapter 5 - Job Order CostingviraNo ratings yet

- Topic 3 - Process CostingDocument30 pagesTopic 3 - Process CostingArvhenn BarcelonaNo ratings yet

- Managerial AccountingDocument16 pagesManagerial AccountingLinh ChiNo ratings yet

- Chapter 10 PPT Agm-1Document13 pagesChapter 10 PPT Agm-1Paulina DocenaNo ratings yet

- 25885110Document21 pages25885110Llyana paula SuyuNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Process Costing: ReadingsDocument52 pagesProcess Costing: Readingsمحمود احمدNo ratings yet

- Hilton Chapter 4 Prerecorded LectureDocument12 pagesHilton Chapter 4 Prerecorded Lecturesunq hccnNo ratings yet

- Process CostingDocument15 pagesProcess CostingyebegashetNo ratings yet

- Akb Bab4Document37 pagesAkb Bab4MulyaniNo ratings yet

- Chapter 2Document5 pagesChapter 2Hania M. CalandadaNo ratings yet

- Relevant Costs For Decision MakingDocument69 pagesRelevant Costs For Decision MakingSederiku KabaruzaNo ratings yet

- Profit PlanningDocument86 pagesProfit PlanningSederiku KabaruzaNo ratings yet

- FIFO MethodDocument40 pagesFIFO MethodSederiku KabaruzaNo ratings yet

- Decentralization and Segment ReportingDocument62 pagesDecentralization and Segment ReportingSederiku KabaruzaNo ratings yet

- "How Well Am I Doing?" Financial Statement AnalysisDocument61 pages"How Well Am I Doing?" Financial Statement AnalysisSederiku KabaruzaNo ratings yet

- Introduction To Entrepreneurship: Module - 1Document14 pagesIntroduction To Entrepreneurship: Module - 1Sederiku KabaruzaNo ratings yet

- Variable Costing-A Tool For ManagementDocument32 pagesVariable Costing-A Tool For ManagementSederiku KabaruzaNo ratings yet

- Activity Based Costing-A Tool To Aid Decision MakingDocument54 pagesActivity Based Costing-A Tool To Aid Decision MakingSederiku KabaruzaNo ratings yet

- MS MakulitDocument3 pagesMS MakulitSederiku KabaruzaNo ratings yet

- History of The Meat IndustryDocument33 pagesHistory of The Meat IndustrySederiku KabaruzaNo ratings yet

- Answer KeyDocument8 pagesAnswer KeySederiku KabaruzaNo ratings yet

- Research Tally SheetDocument85 pagesResearch Tally SheetSederiku KabaruzaNo ratings yet

- Psychoanalysis (Sigmund Frued)Document3 pagesPsychoanalysis (Sigmund Frued)Sederiku KabaruzaNo ratings yet

- Cost Revenue and Profit Functions (English)Document75 pagesCost Revenue and Profit Functions (English)Germy02No ratings yet

- April 2012Document3 pagesApril 2012Derick cheruyotNo ratings yet

- Jawaban MGT BiayaDocument9 pagesJawaban MGT BiayaRessa LiniNo ratings yet

- Mid Term Assignment On: The Superior University LahoreDocument9 pagesMid Term Assignment On: The Superior University LahoreFaizan ChNo ratings yet

- PROBLEM in RELEVANT COSTING 2 OCT 11 2019Document3 pagesPROBLEM in RELEVANT COSTING 2 OCT 11 2019Ellyza SerranoNo ratings yet

- File 0801Document27 pagesFile 0801Kimberly VicenteNo ratings yet

- Intro To Cost AccountingDocument4 pagesIntro To Cost AccountingdollymbaikaNo ratings yet

- Contract Costing 2 PDFDocument30 pagesContract Costing 2 PDFSrinath BabuNo ratings yet

- FUUAST Cost and Mangement Accounting BBA 5 A & B, MBA-2 Eve Spring 2020Document2 pagesFUUAST Cost and Mangement Accounting BBA 5 A & B, MBA-2 Eve Spring 2020Shahroz ShahidNo ratings yet

- Notes by Homeraashraf Standard Costing and Variance AnalysisDocument10 pagesNotes by Homeraashraf Standard Costing and Variance AnalysisZic ZacNo ratings yet

- Team 8a, 8BDocument2 pagesTeam 8a, 8BAravind MadhusudhananNo ratings yet

- Full Download Managerial Accounting The Cornerstone of Business Decision Making 7th Edition Mowen Solutions ManualDocument36 pagesFull Download Managerial Accounting The Cornerstone of Business Decision Making 7th Edition Mowen Solutions Manualaideneba100% (40)

- RESEARCH PROPOSAL For Establishing Pinapple Syrup Processing PlantDocument23 pagesRESEARCH PROPOSAL For Establishing Pinapple Syrup Processing Planttrina_bhagat100% (1)

- Cost AnalysisDocument36 pagesCost AnalysisHarisagar ThulasiramanNo ratings yet

- Ch. 1 Managers and Management AccountingDocument45 pagesCh. 1 Managers and Management AccountingABDI ADDENo ratings yet

- Topic 2 - Basic ConceptsDocument28 pagesTopic 2 - Basic ConceptsjosgarudaeagleNo ratings yet

- Lembar Jawaban Kosong Untuk BelajarDocument55 pagesLembar Jawaban Kosong Untuk BelajarDwiki RamadhonNo ratings yet

- Harp - Ba234 - Flexcon Course ProjectaDocument13 pagesHarp - Ba234 - Flexcon Course Projectaapi-34062055260% (5)

- 74749bos60489 cp6Document34 pages74749bos60489 cp6tempNo ratings yet

- PART I: True or False: Management Accounting Quiz 1 BsmaDocument4 pagesPART I: True or False: Management Accounting Quiz 1 BsmaAngelyn SamandeNo ratings yet