You might also like

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- PRINT 216396833 Con Law Attack SheetDocument24 pagesPRINT 216396833 Con Law Attack SheetAnnsley Oakley89% (37)

- Bernas - The 1987 Constitution (1) - 675-819Document145 pagesBernas - The 1987 Constitution (1) - 675-819Ava Stark100% (1)

- The Budget: Roberto A. Biato, Mpa Jail Chief Inspector Deputy Chief, FSO-NHQDocument58 pagesThe Budget: Roberto A. Biato, Mpa Jail Chief Inspector Deputy Chief, FSO-NHQEnrico ReyesNo ratings yet

- Doctrines Araullo Vs AquinoDocument3 pagesDoctrines Araullo Vs AquinoDelsie FalculanNo ratings yet

- Topic 2.1 Budget Process Budget Prepartion Budget LegislationDocument24 pagesTopic 2.1 Budget Process Budget Prepartion Budget LegislationLeila Ouano100% (1)

- Constitutional Provisions On BudgetingDocument6 pagesConstitutional Provisions On BudgetingJohn Dx LapidNo ratings yet

- The Federal Budget Process, 2E: A Description of the Federal and Congressional Budget Processes, Including TimelinesFrom EverandThe Federal Budget Process, 2E: A Description of the Federal and Congressional Budget Processes, Including TimelinesNo ratings yet

- Insiders Talk: Glossary of Legislative Concepts and Representative TermsFrom EverandInsiders Talk: Glossary of Legislative Concepts and Representative TermsNo ratings yet

- Araullo Vs Aquino III: A Case DigestDocument12 pagesAraullo Vs Aquino III: A Case DigestMarlouis U. Planas94% (35)

- Midterm Exam Constitutional LawDocument91 pagesMidterm Exam Constitutional LawMogsy Pernez0% (1)

- Belgica V Executive SecretaryDocument10 pagesBelgica V Executive SecretaryFG FGNo ratings yet

- Government BudgetingDocument6 pagesGovernment BudgetingMariaCarlaMañago100% (1)

- Budget Legislation: Alternatively Called The "Budget Authorization Phase,"Document13 pagesBudget Legislation: Alternatively Called The "Budget Authorization Phase,"Nikki Ever JuanNo ratings yet

- Absorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualDocument20 pagesAbsorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualPatrick LanceNo ratings yet

- Budget Cycle (Budget Accountability) TEAM 1Document43 pagesBudget Cycle (Budget Accountability) TEAM 1Patrick LanceNo ratings yet

- The Budget ProcessDocument8 pagesThe Budget ProcessGeminah BellenNo ratings yet

- Tolentino Vs Secretary of FinanceDocument22 pagesTolentino Vs Secretary of FinancePatrick RamosNo ratings yet

- The Killing of Osama Bin LadenDocument25 pagesThe Killing of Osama Bin LadenSheni OgunmolaNo ratings yet

- Public Budgeting: Introductory Concepts: Gilbert R. HufanaDocument23 pagesPublic Budgeting: Introductory Concepts: Gilbert R. Hufanagilberthufana446877No ratings yet

- Budget Cycle Both LGU and National Government AgenciesDocument41 pagesBudget Cycle Both LGU and National Government AgenciesKrizzel Sandoval100% (1)

- Incentive Wage Plan: Alonzo, Camille Joyce P. Group 5Document56 pagesIncentive Wage Plan: Alonzo, Camille Joyce P. Group 5Patrick Lance100% (1)

- Bye Laws, 1974 - Under WBAO Act, 1972Document16 pagesBye Laws, 1974 - Under WBAO Act, 1972Basudev GanguliNo ratings yet

- Araullo v. Benigno Simeon Aquino IIIDocument2 pagesAraullo v. Benigno Simeon Aquino IIIJulius Robert JuicoNo ratings yet

- Alumni Association Bye LawDocument6 pagesAlumni Association Bye LawArunNo ratings yet

- Job Order Costing: Illustrative ProblemsDocument30 pagesJob Order Costing: Illustrative ProblemsPatrick LanceNo ratings yet

- Power of AppropriationDocument3 pagesPower of AppropriationMelDominiLicardoEboNo ratings yet

- The Budget ProcessDocument16 pagesThe Budget ProcessBesha SoriganoNo ratings yet

- J.L. Mashaw (2012) Creating The Administrative ConstitutionDocument430 pagesJ.L. Mashaw (2012) Creating The Administrative ConstitutionRENATO JUN HIGA GRIFFIN100% (1)

- Constitutional Law Reviewer For FinalsDocument55 pagesConstitutional Law Reviewer For FinalsGodofredo De Leon Sabado100% (1)

- 2.3. Budget Cycle - Budget LegislationDocument7 pages2.3. Budget Cycle - Budget LegislationJudy Ann TusiNo ratings yet

- Budget CycleDocument26 pagesBudget CycleAleah TyNo ratings yet

- Notes For Re-Enacted Budget Article Vi The Legislative DepartmentDocument9 pagesNotes For Re-Enacted Budget Article Vi The Legislative DepartmentKitem Kadatuan Jr.No ratings yet

- Philippine Fiscal FrameworkDocument18 pagesPhilippine Fiscal FrameworkCamille HofilenaNo ratings yet

- Gpo Hpractice 104 5Document85 pagesGpo Hpractice 104 5BEHAIFAH BOTONESNo ratings yet

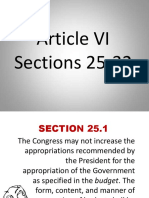

- Article VI Sections 25-32Document66 pagesArticle VI Sections 25-32Rhison AsiaNo ratings yet

- MOd 8 ScriptDocument6 pagesMOd 8 ScriptJennifer GepanayaoNo ratings yet

- C2 The Budget ProcessDocument4 pagesC2 The Budget ProcessCyril Grace DedumoNo ratings yet

- CONSTI 1 - Article VI Sections 25-27 10272022Document13 pagesCONSTI 1 - Article VI Sections 25-27 10272022Docefjord EncarnacionNo ratings yet

- 5powers of CongressDocument46 pages5powers of CongressCidg Nueva VizcayaNo ratings yet

- Public Finance Management Act (Chapter 22-19)Document54 pagesPublic Finance Management Act (Chapter 22-19)Justice MurapaNo ratings yet

- Lesson 3 - Public FinanceDocument18 pagesLesson 3 - Public FinanceSharon Rose Tesoro TugadeNo ratings yet

- Arraullo VS AquinoDocument3 pagesArraullo VS AquinoQuijano ReevesNo ratings yet

- Casals Guingona Jr. v. CaragueDocument11 pagesCasals Guingona Jr. v. CaraguejanmartinmgonzalesNo ratings yet

- Public Finance Act 22 19Document62 pagesPublic Finance Act 22 19stellaNo ratings yet

- Govacc M2Document2 pagesGovacc M2ErosNo ratings yet

- Unit-18 Legislative Control PDFDocument12 pagesUnit-18 Legislative Control PDFSatish DasNo ratings yet

- Reconciliation (United States Congress)Document9 pagesReconciliation (United States Congress)Mujahidul HasanNo ratings yet

- Legal AwarenessDocument12 pagesLegal AwarenessNajeeb AlamNo ratings yet

- Gpo Riddick 1992 34Document141 pagesGpo Riddick 1992 34Jake Dan-AzumiNo ratings yet

- Act, 1993:-The Procedure For Recovery of Debts To The Banks and FinancialDocument7 pagesAct, 1993:-The Procedure For Recovery of Debts To The Banks and FinancialK KOTHAND RAMI REDDYNo ratings yet

- How A Bill Becomes A LawDocument11 pagesHow A Bill Becomes A Law1222No ratings yet

- Budget Rules Matter May 2008Document20 pagesBudget Rules Matter May 2008Manuel L. Quezon IIINo ratings yet

- NMHB2020rev Ch16Document10 pagesNMHB2020rev Ch16jdhartNo ratings yet

- Senate Bill 3121, by Senator Benigno S. Aquino IIIDocument5 pagesSenate Bill 3121, by Senator Benigno S. Aquino IIITonyo CruzNo ratings yet

- Araullo v. Aquino DAP CaseDocument6 pagesAraullo v. Aquino DAP CasefclalarilaNo ratings yet

- Public Finance Management Act As Amended at 31 October 2016Document45 pagesPublic Finance Management Act As Amended at 31 October 2016NARSHON KOHLONo ratings yet

- Gbmaa UpdatedDocument35 pagesGbmaa UpdatedMr DamphaNo ratings yet

- IBC Part V Miscellaneous F2Document43 pagesIBC Part V Miscellaneous F2a.p.singh associatesNo ratings yet

- Budget Legislation: 1. House DeliberationsDocument3 pagesBudget Legislation: 1. House DeliberationspatNo ratings yet

- The National Budget and The Budget ProcessDocument1 pageThe National Budget and The Budget ProcessErica EgidaNo ratings yet

- The Budget Process & The CongressDocument7 pagesThe Budget Process & The CongressNovah Mae Begaso SamarNo ratings yet

- The Budget Process & The Philippine CongressDocument5 pagesThe Budget Process & The Philippine CongressSimon WolfNo ratings yet

- Araullo v. Aquino G.R. 209287 July 1, 2014 Bersamin JDocument5 pagesAraullo v. Aquino G.R. 209287 July 1, 2014 Bersamin JMarkee Nepomuceno AngelesNo ratings yet

- Budget LegislationDocument7 pagesBudget LegislationJohn Lloyd EspinosaNo ratings yet

- IF10514Document3 pagesIF10514chichponkli24No ratings yet

- Public Sector Accounting APS 20103 Financial Accounting Systems and ProceduresDocument26 pagesPublic Sector Accounting APS 20103 Financial Accounting Systems and ProceduresAsheequin ZainolNo ratings yet

- 2ND321 - Foundation of EducationDocument26 pages2ND321 - Foundation of EducationMary Rose GonzalesNo ratings yet

- LAWSDocument5 pagesLAWSZenez B. LabradorNo ratings yet

- PH Goverment Accounting Budget ProcessDocument9 pagesPH Goverment Accounting Budget ProcessNabelah OdalNo ratings yet

- Basic Concepts in BudgetingDocument4 pagesBasic Concepts in BudgetingniqdelrosarioNo ratings yet

- Budget Cycle - Budget Preparation - Team 2Document11 pagesBudget Cycle - Budget Preparation - Team 2Patrick LanceNo ratings yet

- 1 Barangay Budget and Process TEAM3Document13 pages1 Barangay Budget and Process TEAM3Patrick LanceNo ratings yet

- Job Order Costing: Group 3 Santiago, Erica DDocument17 pagesJob Order Costing: Group 3 Santiago, Erica DPatrick LanceNo ratings yet

- Time Standards and Learning Curve TheoryDocument33 pagesTime Standards and Learning Curve TheoryPatrick LanceNo ratings yet

- Leigh Ann S. RamosDocument28 pagesLeigh Ann S. RamosPatrick LanceNo ratings yet

- Accounting For Personnel Related CostsDocument59 pagesAccounting For Personnel Related CostsPatrick LanceNo ratings yet

- Organization For Labor Cost Accounting and ControlDocument22 pagesOrganization For Labor Cost Accounting and ControlPatrick LanceNo ratings yet

- Maniego, Chantelle Kyle TDocument15 pagesManiego, Chantelle Kyle TPatrick LanceNo ratings yet

- Casicas, Andrea Nicole ADocument22 pagesCasicas, Andrea Nicole APatrick LanceNo ratings yet

- PATTTTDocument1 pagePATTTTPatrick LanceNo ratings yet

- Activity-Based, Absorption and Variable CostingDocument83 pagesActivity-Based, Absorption and Variable CostingPatrick LanceNo ratings yet

- NAT Mock Social Sciences FinalDocument5 pagesNAT Mock Social Sciences FinalRafael PresadoNo ratings yet

- The President's Job DescriptionDocument5 pagesThe President's Job DescriptionMayeth MacedaNo ratings yet

- Final Censure ResolutionDocument2 pagesFinal Censure ResolutionPennLiveNo ratings yet

- Robotics Club Constitution Final Copy UpdatedDocument4 pagesRobotics Club Constitution Final Copy Updatedomit senNo ratings yet

- UNITY Mauritius Overview V0.1.7 Last Updated 28 Jun20.07Document7 pagesUNITY Mauritius Overview V0.1.7 Last Updated 28 Jun20.07dhaylan cuneapenNo ratings yet

- US Presidents ListDocument2 pagesUS Presidents ListkenechidukorNo ratings yet

- BBI Final VersionDocument156 pagesBBI Final Version243695% (43)

- GFJ 01-22-2023 LTR To ArchivesDocument2 pagesGFJ 01-22-2023 LTR To ArchivesCNBC.comNo ratings yet

- MCQs RST All About History by Jawed Ali SamoDocument104 pagesMCQs RST All About History by Jawed Ali SamoUzair SoomroNo ratings yet

- 1973 Constitution of The Republic of The PhilippinesDocument33 pages1973 Constitution of The Republic of The PhilippinesArnulfo Yu LanibaNo ratings yet

- Constitutional Law Pemberton Alenhart Spring 2020 OutlineDocument39 pagesConstitutional Law Pemberton Alenhart Spring 2020 Outlinesantito1203No ratings yet

- 2013SOFIACTRefManual FinalDocument162 pages2013SOFIACTRefManual Finalcondorblack2001No ratings yet

- Astroga v. VillegasDocument8 pagesAstroga v. VillegasAmicah Frances AntonioNo ratings yet

- CFR Annual Report 2002 0 PDFDocument128 pagesCFR Annual Report 2002 0 PDFBoris MarkovićNo ratings yet

- Power Sector Assets v. CIR GR 198146 8 Aug 2017Document19 pagesPower Sector Assets v. CIR GR 198146 8 Aug 2017John Ludwig Bardoquillo PormentoNo ratings yet

- CBL 2019-2020 CSGDocument21 pagesCBL 2019-2020 CSGFavor Christian BustilloNo ratings yet

- The American Empire - Garet Garrett PDFDocument18 pagesThe American Empire - Garet Garrett PDFVZZNo ratings yet

- A Critical Analysis On Sixteen Amendment of Bangladesh Constitution A Legal StudyDocument51 pagesA Critical Analysis On Sixteen Amendment of Bangladesh Constitution A Legal StudyMohammad Safirul HasanNo ratings yet

- Datu Michael Abas Kida v. Senate 659 Scra 270 (2011)Document16 pagesDatu Michael Abas Kida v. Senate 659 Scra 270 (2011)John OrdanezaNo ratings yet

- Political Law Bar Questions 2010-2019Document100 pagesPolitical Law Bar Questions 2010-2019Jose Antonio BarrosoNo ratings yet

- Nuesa Biu Draft Constitution - 1Document16 pagesNuesa Biu Draft Constitution - 1Kadiri DonaldNo ratings yet

- General Supervision Over FederalDocument20 pagesGeneral Supervision Over FederalAVNISH PRAKASHNo ratings yet